Dear Investor,

The Altrinsic Emerging Markets Opportunities portfolio gained 13.0% (12.7% net of fees) during the second quarter, compared to the 12.0% gain of the MSCI Emerging Markets (Net) Index, as measured in US dollars.i Positive attribution was derived from stock-specific performance in select countries (Brazil, Vietnam, Peru) and key sectors (consumer discretionary, financials, real estate). Our holdings in South Korea, our underweight positioning in Taiwan, and our underweight exposure and foreign exchange effects in the IT sector were sources of negative attribution.

Perspectives

The first half of 2025 – and the second quarter, in particular – challenged the market’s expectations. Emerging markets outperformed developed markets despite tariff headwinds and heightened global volatility, reminding us to stay grounded in fundamentals with a long-term perspective, rather than getting caught up in short-term headlines. Broadening performance across EM, and historically low cross-market correlations, suggest fertile ground for bottom-up stock selection. Equity valuations remain broadly attractive, and a declining US dollar has served as a tailwind for many EM companies and countries. Ongoing trade discussions, geopolitical unrest, and other economic factors could drive USD volatility, however, presenting new risks. Beneath the surface, deeper structural shifts are underway. From supply chain realignments to intensifying resource constraints – particularly growing concerns over water scarcity – the emerging markets landscape is evolving due to a series of influential undercurrents.

EM Strength in Choppy Waters

Year-to-date global market returns may paint a picture of smooth sailing, but there have been turbulent waters along the way. The S&P 500 hit new highs, Mag 7 stocks led gains, and developed markets, as measured by the MSCI World Index, rose almost 10%. Simultaneously, US markets recorded their highest volatility in 25 years (excluding the COVID-19 and GFC outliers), global trade faced fresh disruptions, and fears grew as headlines highlighted the potential strain on emerging markets.

Emerging markets have quietly and broadly outperformed developed markets, rising 15.3% year-to-date. A few drivers are at play – most notably, a weakening US dollar, renewed enthusiasm around AI and China, and broad resilience of EM countries.

The US dollar declined nearly 11% year-to-date1 on a trade-weighted basis. Additionally, the MSCI EM Index’s heavy weighting – over 21%2 – in AI/tech leaders and dominant Chinese LLM stocks boosted returns as consumers and investors flocked back to the ‘hot dots’ following the DeepSeek episode and heightened AI enthusiasm.

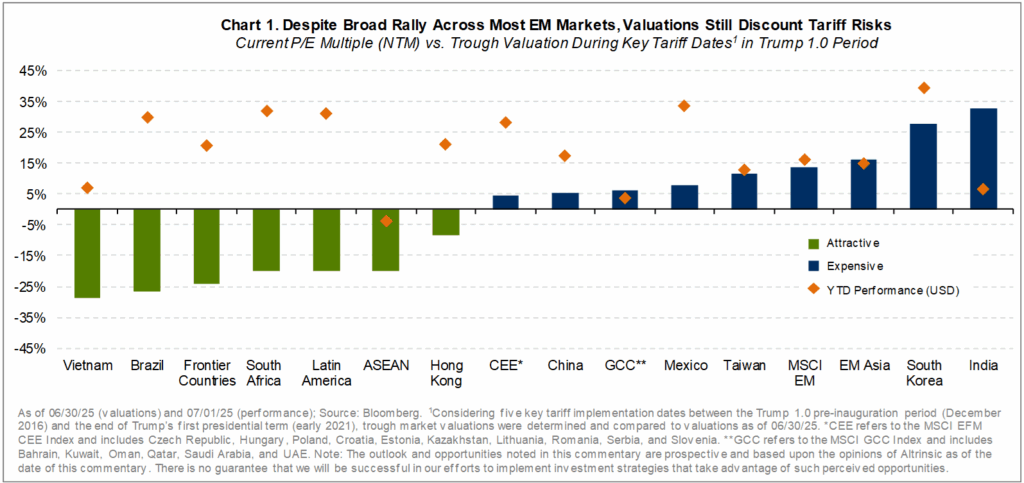

Importantly, however, a wide variety of emerging markets proved resilient amid economic and market headwinds. Most countries, especially outside ASEAN, posted strong USD gains (Chart 1); median returns hit 17.5%, surpassing the impact of the US dollar depreciation. Taiwan, despite its tech-heavy market, actually lagged broad EM results, and China, despite steep tariffs, outperformed India by nearly 11%. Other markets, including Brazil, Peru, Hungary, and South Africa, also delivered strong gains.

Valuations remain appealing across most markets; Taiwan and India are the exceptions. Our portfolio stands out for its differentiation and diversification, featuring lower exposure to the largest countries and market constituents and higher weights in smaller markets (Table 1).

Redrawing the Trade Routes

Many assumed that the implementation of Trump’s tariffs would cause significant pain for emerging markets.3 The reality is that many EM companies continue to expand their businesses within emerging and frontier markets, a longer-term trend that now also creates a pathway to neutralize some of the potential tariff disruptions.

In the current environment, our emerging markets decoupling thesis is gaining momentum. Growth now stems from rising local consumption, shifting supply chains, and new intra-EM trade links. Reduced reliance on developed economies and business strategies that capitalize on strong demographic and economic trends fuel faster growth, improved profitability, and more sustainable financial productivity.

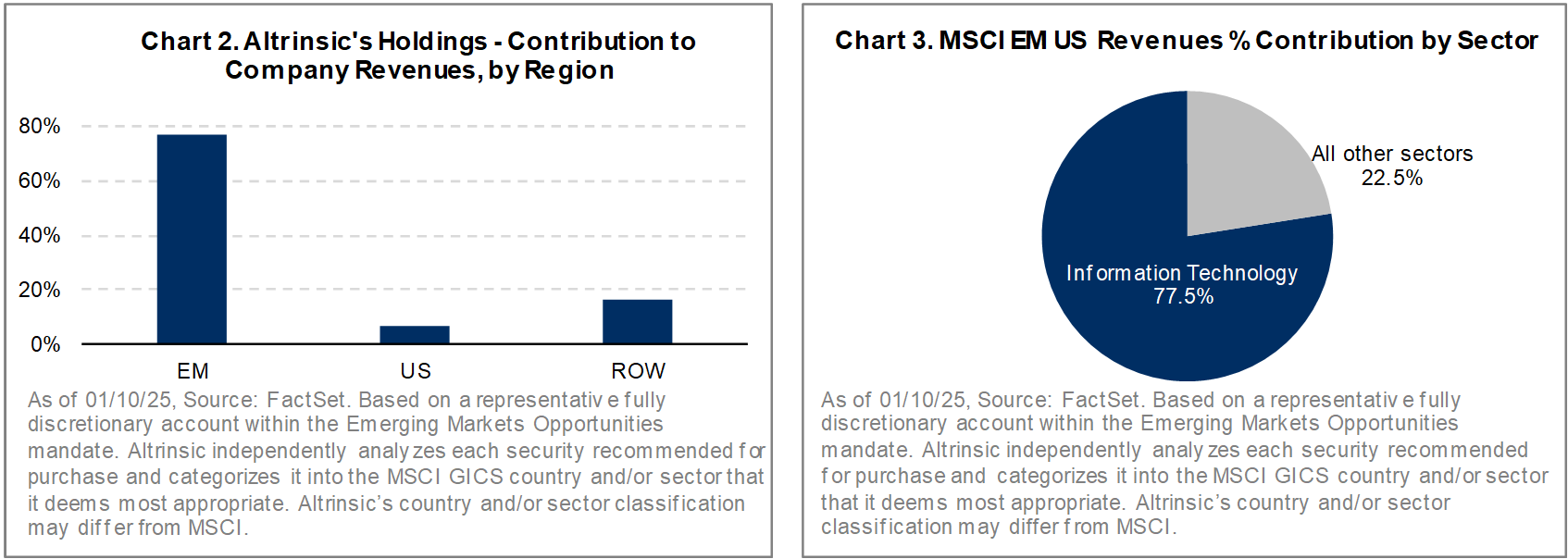

As shown in Chart 2, our portfolio companies offer direct and differentiated EM exposure, with nearly 80% of revenues generated from emerging market countries.

The MSCI EM Index’s US-based revenues are concentrated in the expensive information technology sector (Chart 3), with 63%4 of that generated by Taiwanese companies. By contrast, our portfolio offers more balanced and diversified sector and country weightings.

Currency Crosscurrents

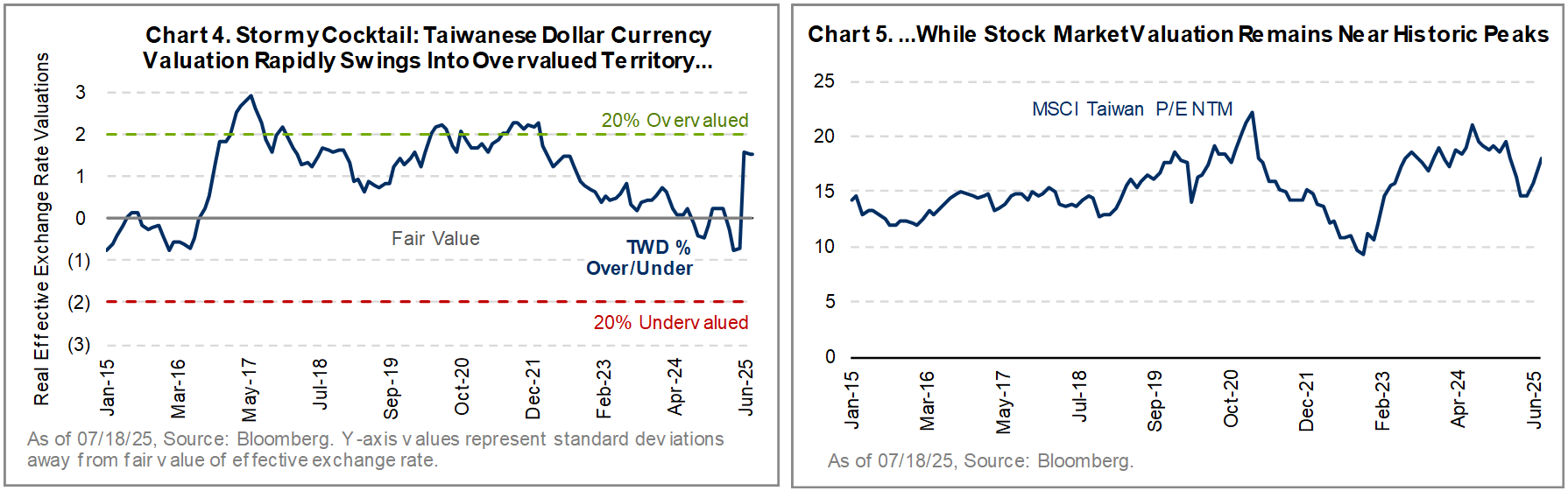

The 10.7% year-to-date decline of the US dollar on a trade-weighted basis provided a tailwind to emerging markets returns, but currency dynamics have shifted meaningfully across regions. Six major markets – India, Indonesia, Saudi Arabia, UAE, Taiwan, and Hungary – experienced the most pronounced moves in real exchange rate valuations. The first four saw currency depreciation, enhancing their relative attractiveness, while the Hungarian forint and Taiwanese dollar appreciated sharply.

The most notable shift came from Taiwan, where the currency appreciated 11.6%, nearing historic highs (Chart 4). Taiwan’s currency outpaced gains in the Japanese yen, Korean won, or Chinese renminbi in 1H25, eroding competitiveness. This poses earnings risks for Taiwanese companies, particularly given their significant US-based revenue exposure. For Taiwan’s tech companies, nearly 90% of sales are in USD, while most costs are incurred locally. Foundries like TSMC, for example, have roughly 50% of their cost of goods sold in USD, amplifying FX sensitivity. Despite robust AI demand, dollar strength compresses translated revenues and inflates local costs, pressuring margins. TSMC noted recently that a 1% currency move translates into a 0.4% operating margin headwind.5 With Taiwanese stock valuations near historic highs (Chart 5), the margin for error is narrowing.

Against this backdrop, sustaining high top-line growth will be critical to offset currency-related margin compression. We do not believe that peak multiples are widely justified, and we continue to favor companies across geographies and industries with more diversified revenue streams. Our portfolio’s limited US revenue exposure and underweight position in Taiwan should help navigate current trade and FX headwinds with more resilience.

H2-Uh-Oh

An important but under-the-radar structural concern in EM is water scarcity. No longer just a humanitarian concern, water availability is becoming a material constraint on economic activity and corporate profitability. As water scarcity increasingly affects industrial output, agricultural yields, and geopolitical stability, we believe it will become a more pronounced risk and prominent factor in asset pricing.

Industry, agriculture, and households are all competing for a finite resource; agriculture accounts for 72% of global freshwater use, industry 16%, and domestic consumption 12%. Our recent travels underscored the severity of this challenge, from depleted aquifers in Monterrey, Mexico, to intensifying water disputes between India and Pakistan.

But beyond the obvious, observable shortages, a still-relevant 2023 Euronews headline6 offers a striking example of a growing – and rapidly accelerating – issue:

“ChatGPT ‘drinks’ a bottle of fresh water for every 20 to 50 questions we ask”

This headline points to a broader issue in the technology and industrial ecosystems: beyond surging user demand for AI tools, the real constraint lies in the immense water (and energy) resources required to manufacture the chips powering AI. Despite growing awareness, we believe market valuations rarely reflect the economic implications.

In Taiwan – the global epicenter of semiconductor manufacturing, responsible for 20% of worldwide output and 90% of advanced chips – key reservoir levels currently average 92%7 capacity, but memories of the 2021 drought, which halted chip production, loom large. Even minor shifts in typhoon patterns could quickly turn water from an asset to a vulnerability, introducing noteworthy operational risks.

The impacts of water shortage concerns are not limited to EM countries. In response to geopolitical pressures and soaring demand, TSMC committed in 2023 to invest $165 billion in new fabs in Arizona. But according to a July 2024 World Economic Forum report, a single chip facility can consume up to 10 million gallons of ultrapure water per day – enough to supply 33,000 US households. With half of Arizona classified as desert, persistent water shortages in the Colorado River Basin have contributed to delayed project timelines.

As chipmakers scale capacity8 amid tightening global water supplies, their valuations may be due for a splash of cold water. We continue to monitor water-related risks as part of our broader sustainability framework, both from the standpoint of macro considerations and, of course, bottom-up stock selection. We expect this theme to grow in importance and impact over the next several years, and we look forward to having more occasions to discuss its investment implications (both risks and opportunities) as the environment continues to evolve.

Concluding Remarks

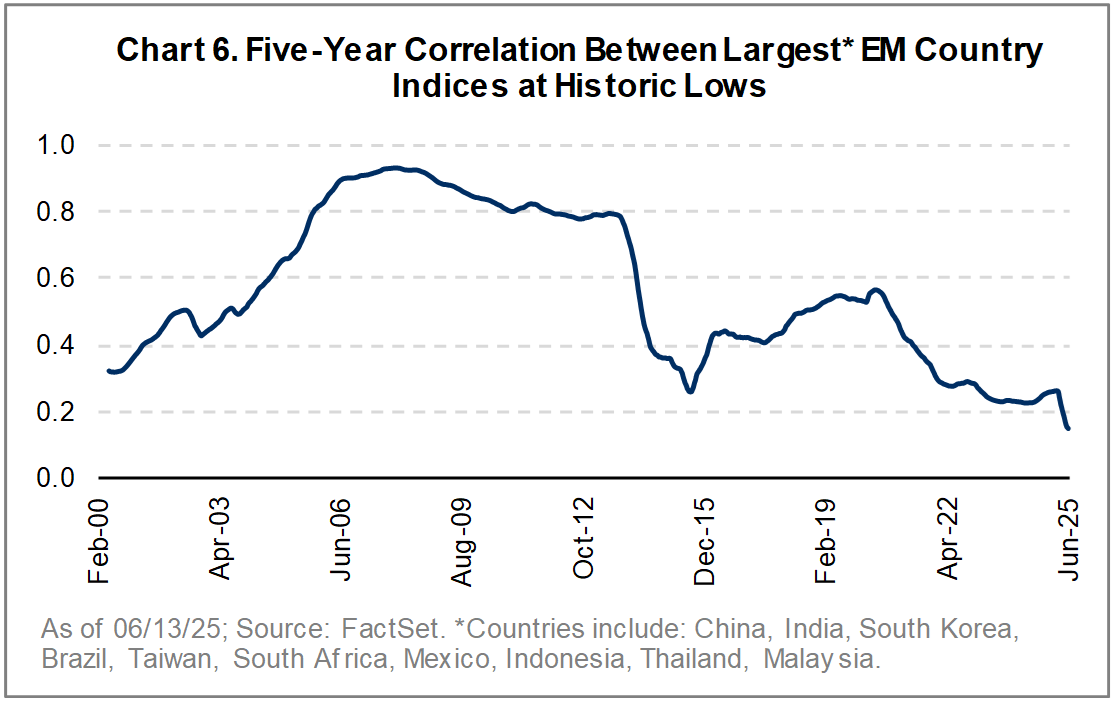

The first half of 2025 reminded us that emerging markets are not a monolith – instead, they are a mosaic of diverse economies, each responding differently to shifting global tides. Correlations across EM country indices have broken down in a post-pandemic period of unsynchronized economic and earnings cycles as well as a fragmented world of exclusive trade agreements. Five-year correlations among the largest EM markets have reached historic lows (Chart 6). Further, country correlations have been below 50%, on average, for over a decade – this is not a new phenomenon, despite prevailing rhetoric about the asset class being seen as a bloc.

While headlines often amplify risks and play to common fears, the underlying data usually tells a more nuanced story. EM equities broadly outperformed, correlations fell, and new growth drivers emerged beneath the surface. Yet, challenges remain. Currency volatility, trade uncertainty, and resource constraints – particularly water – are reshaping the investment landscape in subtle but significant ways.

In this environment, we believe thoughtful differentiation matters more than ever. Our portfolio is built to navigate complexity: diversified across countries and sectors, underweight in crowded areas, and focused on companies with resilient business models and authentic EM exposure. Alpha will increasingly be generated by company-specific drivers, as opposed to sentiment toward the asset class as a whole. For active managers, this presents a tremendous opportunity to find compelling, underappreciated businesses. Traveling frequently and engaging in our deep networks of local contacts is critical in getting to know the companies, their management teams, and the environment in which they are operating. As we look ahead to the second half of the year and beyond, we remain grounded in fundamentals, alert to structural shifts, and committed to uncovering opportunities where others may not be looking.

Sincerely,

Alice Popescu

2Q25 Performance Review and Investment Activityi,ii

The Altrinsic Emerging Markets Opportunities portfolio gained 13.0% (12.7% net of fees) during the second quarter, compared to the 12.0% gain of the MSCI Emerging Markets (Net) Index, as measured in US dollars.

From a sectoral perspective, stock-specific gains in consumer discretionary (Lojas Renner, Coway), financials (Porto Seguro, KB Financial Group, Banorte), and real estate (Vinhomes) were only partially offset by performance in industrials (Center Testing International, Yutong Bus) and utilities (China Resources Gas), as well as our underweight positioning and FX effects in information technology.

From a geographic perspective, gains due to stocks in Brazil (Porto Seguro, Lojas Renner, GPS Participacoes, Motiva), Vietnam (Vinhomes), and Peru (Credicorp) were partially offset by the performance of holdings in South Korea, our underweight positioning in Taiwan, as well as stock-specific issues in South Africa (Aspen Pharmacare Holdings).

The quarter started with significant volatility linked to the ‘Liberation Day’ announcement and its ensuing ripple effects across global markets. We took advantage of the unrest in the market to build positions in recently initiated stocks (International Container Terminal) and replenish deeply undervalued stocks in Indonesia (PT Bank Mandiri, Sumber Alfaria Trijaya, PT Telkom Indonesia), Egypt (Commercial International Bank of Egypt), South Africa (Standard Bank), and China (China Resources Beer Holdings).

Portfolio activity was limited in the quarter with two sales (Aspen Pharmacare Holdings, Parade Technologies) and one purchase (Sinbon Electronics), reflecting our investment process and sell discipline.

We exited our position in Aspen Pharmacare Holdings, a South African pharmaceutical company, after the company lost a major client that would have been crucial to its anticipated manufacturing ramp-up and margin recovery. With limited management disclosure and declining conviction in execution, the stock’s risk-reward profile became less attractive relative to new opportunities in the portfolio.

We also exited Parade Technologies, a fabless semiconductor company in Taiwan. Parade’s key drivers included constant upgrades to higher resolution displays and ever-increasing demand for higher data transfer rates within devices and peripherals. While the company’s underlying performance was impacted by an industry inventory correction, we noted challenges in its recent execution. We have seen a delay in margin improvements from better product mix, which has diminished earnings growth visibility. A partially broken thesis and less favorable risk-return profile led us to sell the stock.

We added Sinbon Electronics, a leading Taiwanese maker of specialty cables and connectors for sectors including medical, auto, green energy, and industrial. Its strength in customized products for demanding uses has fueled growth into new, expanding markets. We believe Sinbon is undervalued compared to global peers given its expanding global presence, scale gains, and strong financial productivity.