Dear Investor,

Global equities delivered strong gains during the first quarter as investors shrugged off two of the three largest bank failures in US history and the collapse of once venerable Credit Suisse. The proximate cause for the rally is a belief that inflation risk is vanquished, interest rates have peaked, years of extraordinary financial stimulus can be normalized painlessly, and the global economy will not experience a downturn. This implies a tremendous amount of confidence in policymakers.

The Altrinsic Global Equity portfolio gained 4.3% (4.1% net), lagging the MSCI World Index’s 7.7% gain, as measured in US dollars.i Headline index gains masked significant underlying volatility in sector and style performance (Chart 1), as market leadership came from an unlikely combination of the longest duration growth stocks (a proxy for lower rates) and nonfinancial cyclicals (a proxy for economic growth – or at least a soft economic landing). Traditionally defensive sectors including utilities, health care, and consumer staples lagged. Growth indices far outpaced value indices, and high beta was the best performing factor.

The primary source of our relative underperformance was our lack of growth stocks, an underweight exposure to high beta non-financial cyclicals, and poor performance by our financials investments. Probing deeper into growth stocks’ role in performance this quarter, the three best performing sectors were information technology (led by Apple, NVIDIA, Microsoft), communication services (Meta, Alphabet), and consumer discretionary (Tesla, Amazon). In fact, those seven stocks contributed to over half the MSCI World Index’s gain and almost all of our relative underperformance (~300bps).

Some of our investments in these industries lagged as well – notably Gen Digital (IT) and Advance Auto Parts (consumer discretionary). Gen Digital declined on fears of a revenue slowdown despite improving profitability and cash flow generation following its acquisition of cybersecurity firm Avast. The temporary revenue slowdown is an unhelpful consequence of the merger that will improve over time. Until then, expenses remain in check and cash flow is increasing. Advance Auto Parts declined as company initiatives to improve customer service will lead to temporarily heightened inventory levels and lower cash flow. We look favorably on the inventory investments, as improved availability should drive sales growth closer to peer levels in the structurally sound auto parts aftermarket.

The greatest sources of positive attribution came from investments in the consumer staples (Heineken, Danone) and materials (CRH, Akzo Nobel) sectors. Heineken announced results showing continued growth in volume, sales, and profits through their ongoing premiumization strategy. Additionally, FEMSA (an economic owner of 15% of Heineken) announced their intention to sell 40% of their position, with Heineken buying back a quarter of that stake. This decision removes an overhang and highlights management’s (and investors’) confidence in the company. Danone results were better than feared, demonstrating that the new management team has regained investor trust to embark on their growth and efficiency efforts. Akzo and CRH benefitted from declining input costs while maintaining pricing power and improved return potential. CRH was further aided by the announcement about moving their listing from the UK to the US, which will highlight the valuation disconnect from its closest peers.

Perspectives

Decisions have consequences. The extraordinary stimulus measures and recurring bailouts that characterized the years since the global financial crisis (GFC) have contributed to a moral hazard and inflation in risky assets. While markets shrugged off major bank failures during the first quarter, the consequences of a long overdue reversal of easy monetary policy and supercharged global stimulus are unlikely to be short-lived. New opportunities are emerging but significant excesses still need to deflate.

Early casualties have been among the more speculative beneficiaries of zero interest rates and a world awash with liquidity: profitless tech companies, SPACs, crypto-tokens and exchanges, and Robinhood, to name a few. Sudden spikes in bond yields exposed flaws in Liability Driven Investment (LDI) strategies of UK pension plans and ultimately contributed to the collapse of Silicon Valley Bank, Signature Bank, and Credit Suisse. Even China’s once vaunted infrastructure improvement Belt and Road initiative has seen bailouts balloon. Illiquid private companies and venture capital portfolios have drawn attention but have yet to take the full write-downs that public markets suggest they should. While public markets are not offering the fire sale values that one might expect given current macroeconomic and geopolitical factors, there is a lot of pessimism priced into a growing number of companies.

Commercial real estate (CRE) is a casualty in the early innings of a struggle that warrants close attention. A dangerous cycle may be underway with profound consequences for developers, banks, and the economy. CRE prices have been under pressure due to rising interest rates, rising vacancy rates, and stressed borrowers, to name a few. In Europe, many CRE owners are adjusting their bloated debt structure (often 2-3x the leverage of US counterparts) by slashing dividends and selling assets. In the US, CRE’s primary lenders (regional banks) are under tremendous pressure from deposit outflows, increased regulatory scrutiny, rising non-performing loans, and the need to reevaluate their entire business models. This set of factors has the hallmarks of a troubling cycle in the making given regional banks’ vital role in providing credit to local communities and households. In a post-GFC world, one could reasonably assume that the increased regulation, supervision, capital requirements, and “stress tests” would make the risk of developed market bank failures unimaginable. Yet, here we are again.

At a minimum, banking regulation will certainly increase and weigh on banks’ profitability. Financial conditions are already tightening and will dampen economic growth in the months ahead. Markets are taking an optimistic view of this, implying that reduced lending will slow inflation more effectively – and with fewer side effects – than Fed actions. Policymakers are balancing inflationary pressures, financial system stability, and politics at a time of unprecedented global leverage, near peak corporate profit margins, and elevated valuations.

Our exposure to banks has varied greatly over the years given their inherent leverage, reliance on the interest rate curve, underlying cyclicality, and a tendency for valuations to overshoot in both directions. During recent years, our exposure was limited to Japan, but more recently we have added emerging market banks to the portfolio. None of our bank holdings experienced the combination of sharp growth in uninsured deposits, asset/liability duration mismatches that hindered liquidity, large unrealized losses on government securities, and weak capital that contributed to the collapse of SVB and Signature in the US. The turmoil during the quarter has increased the valuation appeal, but regulation, increased capital requirements, and increased funding and insurance costs will weigh on ROEs. We keep an open eye to banks with quality franchises, strong management teams, and healthy balance sheets.

Despite the seemingly slow motion roll of casualties, corporate earnings and expectations for their growth have been surprisingly resilient – particularly in the US (Charts 2 & 3). This is largely due to extraordinary pricing actions taken by corporations, in many cases well in excess of input costs. Consumers have been accepting of the increases due to an unstable combination of pent-up COVID demand, savings, and stimulus. Pricing power and earnings will be important drivers of performance in coming quarters, particularlyin the sectors where valuations and expectations are the highest like tech and consumer discretionary.

We believe it is fruitless to try to forecast central bank policies, market-determined interest rates, or inflation in the short or long term. We do believe it is important to recognize structural change, consider new frameworks, and ponder risks that could carry greater probabilities than markets reflect. A return to the past goldilocks environment of modest growth, steadily declining interest rates, and low stable inflation in major developed economies is just a remote possibility. We must be mindful that unpleasant conditions, including stagflation, are realistic possibilities. Well-capitalized and noncommoditized business models in which talented, nimble, and aligned management teams can adapt to changing environments and grow shareholder value should be increasingly rewarded in the market. Price paid (valuation) matters – as it always does over the long term. Table 1 provides a global perspective on how different markets are reflecting these macroeconomic uncertainties, as captured in primary valuation measures.

Portfolio Exposures and Investment Activity

Table 2 depicts our industry exposures compared to those of the MSCI World Index. Our portfolios are constructed using a bottom-up approach, company by company, with a prudent regard for risk throughout the process. The result is a portfolio positioned very differently from benchmarks with below market risk, and a concentration of attractively valued companies that we believe will deliver sustainable and/or improving returns.

Our three largest overweight exposures are non-bank financials, food and beverage franchises, and pharma biotech and life sciences companies.

Our Non-Bank Financials exposure is primarily in property and casualty insurance-focused businesses (Chubb, Everest Re, Willis Tower Watson) and exchanges (ICE, Euronext, JPX). Our insurance-related holdings have multi-year ROE tailwinds due to improved competitive discipline, rising demand in a risky world, better capital allocation, and rising investment income in the current interest rate environment. These companies have a fraction of the leverage of a typical bank with very little funding risks, and many trade at deeply discounted valuations on normalized earnings power. Our exchange holdings have solid competitive moats, attractive free cash flow margins, and new avenues to monetize their strong data and clearing platforms, particularly in a more volatile world.

Many Food & Beverage franchises operate in structurally sound categories and/or with scope for operational improvement undertaken by newly installed, experienced management teams. The ongoing trend toward premiumization and the significant tailwinds from the world reopening to consumers also contribute to these companies’ future prospects. While many might consider these companies dull and defensive, we see several avenues for growth.

Pharma Biotech & Life Sciences companies offer very attractive free cash flow yields and are positioned to benefit from innovations in areas including medical devices, Alzheimer’s, oncology, and cardiology. Scientific advancement in drug discovery tools and targets, as well as the increasing use of AI in medical devices, are driving new business opportunities. There is significant underappreciated change taking place in the health care space, including evolving business models, the move toward value-based care, and improved data utilization.

Our three largest underweight exposures include information technology, consumer discretionary, and utilities.

Information Technology companies offer pockets of value, but we expect many of the popular growth stocks to go through a period of value purgatory, similar to what former TMT darlings (including Cisco) experienced in the aftermath of the 1998-2000 TMT bubble. Many of the popular avenues for growth for the largest tech players are much closer to their end than beginning, with global smartphone penetration now at 84%, global digital advertising penetration at 66%, and global e-commerce penetration at 20% (versus 10% just five years ago).1 Either valuations fall to more sensible levels considering underlying earnings, or stock prices wait for earnings to catch up. We see growing opportunities and the most compelling value in enterprise companies with mission-critical products, significant recurring revenue, and drivers of value creation that are within their control.

The Consumer Discretionary sector is dominated by notoriously cyclical auto companies and highly valued retailers and luxury companies. Profitability and valuations in each of these areas are near peak levels as demand was either shifted or pulled forward by COVID constraints or stimulus, leaving them vulnerable to any consumer hiccups.

Utilities tend to underperform in a sharply rising interest rate environment, as it causes liquidity concerns for the sector’s relatively high debt load. Several utilities are already issuing equity to fund capex, and most companies have unappealing risk/reward skews in light of high valuations coupled with regulatory, growth, and cost pressures.

We are seeing pockets of value emerge among cyclical industrials and materials companies, but much of the recent strength has been among highly cyclical and high beta companies whose elevated valuations and lofty profit margins leave little margin of safety in the event of disappointment. We expect these companies to exhibit volatility (as they always do), and we will be opportunistic when attractive investment propositions arise. We have found the most compelling opportunities among companies that are embracing technology and/or enhancing the services components of their business models.

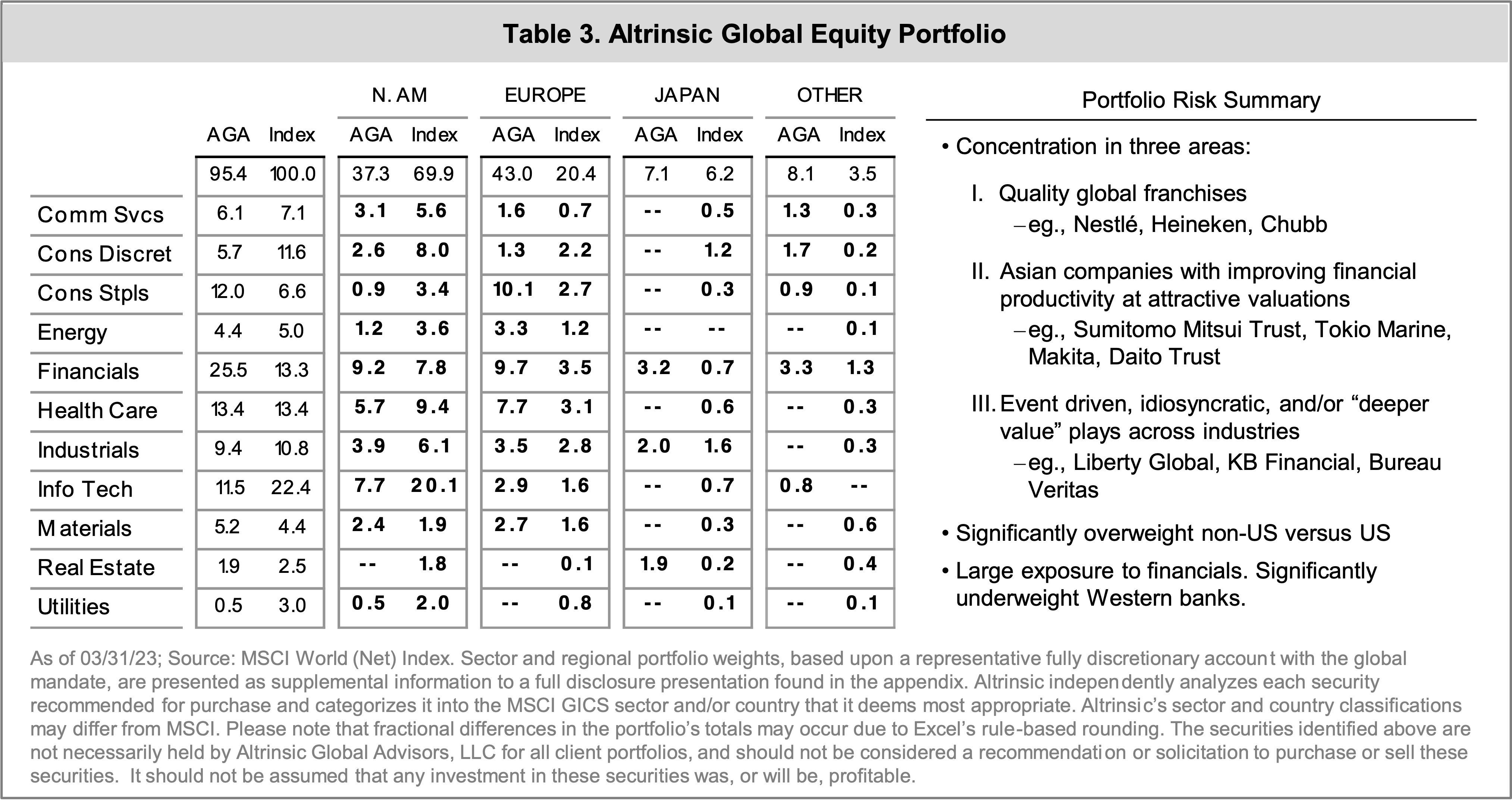

Table 3 provides a cross-sectional view of regional and sector exposures.

Investment activity was somewhat subdued this quarter, as we exited five positions (Astellas Pharma, Berkshire Hathaway, Julius Baer, Smiths Group, Trip.com) and established two new positions (Axis Capital, Kroger). Astellas faces increased competition, degrading the risk/return profile. The other companies were sold as their discounts to our intrinsic value estimates have substantially narrowed. Amidst the extreme pessimism within the financials sector, we initiated a position in specialty insurer and reinsurer Axis Capital. The current stock price does not reflect the improvements being made at both the organizational level (better business mix, more disciplined pricing, new CEO with turnaround success) and industry level (tailwinds of a better competitive environment and interest rate environment) to drive prolonged earnings growth. We also reintroduced a position in leading supermarket operator Kroger. The shares have come well off their post pandemic high (where we sold), but the company is executing well with sharpened price focus, omni channel efforts, and enhanced prepared and local food offerings. The pending merger with Albertsons adds scale and is highly complementary.

In conducting our due diligence, we subscribe to the old adage that “seeing is believing, while reading can be deceiving.” Put more eloquently, investors need to get out there and “kick the tires.” Our team has spent significant time on the road during the last year with recent research trips throughout the US, Brazil, Taiwan, Continental Europe, the UK, Southeast Asia, India, and Japan, among others. These trips have heightened our conviction in some investments while highlighting weaknesses in others. In all cases, the on-the-ground experiences increased our depth of knowledge, broadened our networks, improved our perspective, and have ultimately been additive to our clients’ portfolios. Selective trip notes written by individual analysts are periodically shared with our clients and/or made available on our website and LinkedIn.

The macro conditions around the world range from murky to downright treacherous. Ongoing risks include war, excessive debt, economic imbalances, geopolitical tensions, and – most importantly – those that are not yet known. Macro uncertainties are a given. However, our investments’ combination of compelling valuations and long-term scope for sustainable and/or improving financial productivity, along with the differentiated risk profile embedded in our portfolio give us great confidence in our ability to deliver superior risk-adjusted returns for our clients during these complicated times.

Sincerely,

John Hock

John DeVita

Rich McCormick