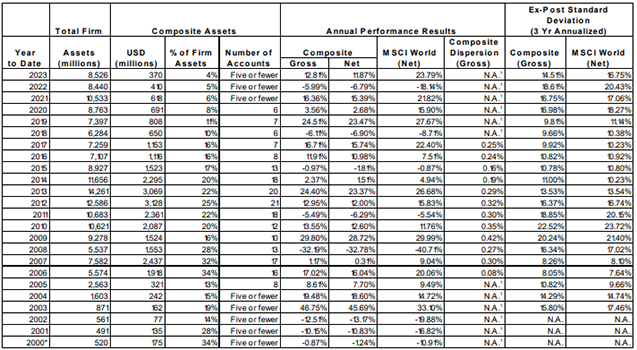

Dear Investor,

It was a strong quarter for risk assets, with robust gains for equities, tightening high-yield credit spreads, rising oil prices, and a spike in cryptocurrencies. The global economy, led by strength in the US, has demonstrated impressive resilience following sharp interest rate hikes, as economic data generally surprised to the upside. Meanwhile, inflation has moderated but it remains well above levels experienced in recent decades. The resulting “soft landing” narrative, expectations for interest rate cuts, and continued excitement surrounding AI have fueled a powerful rally.

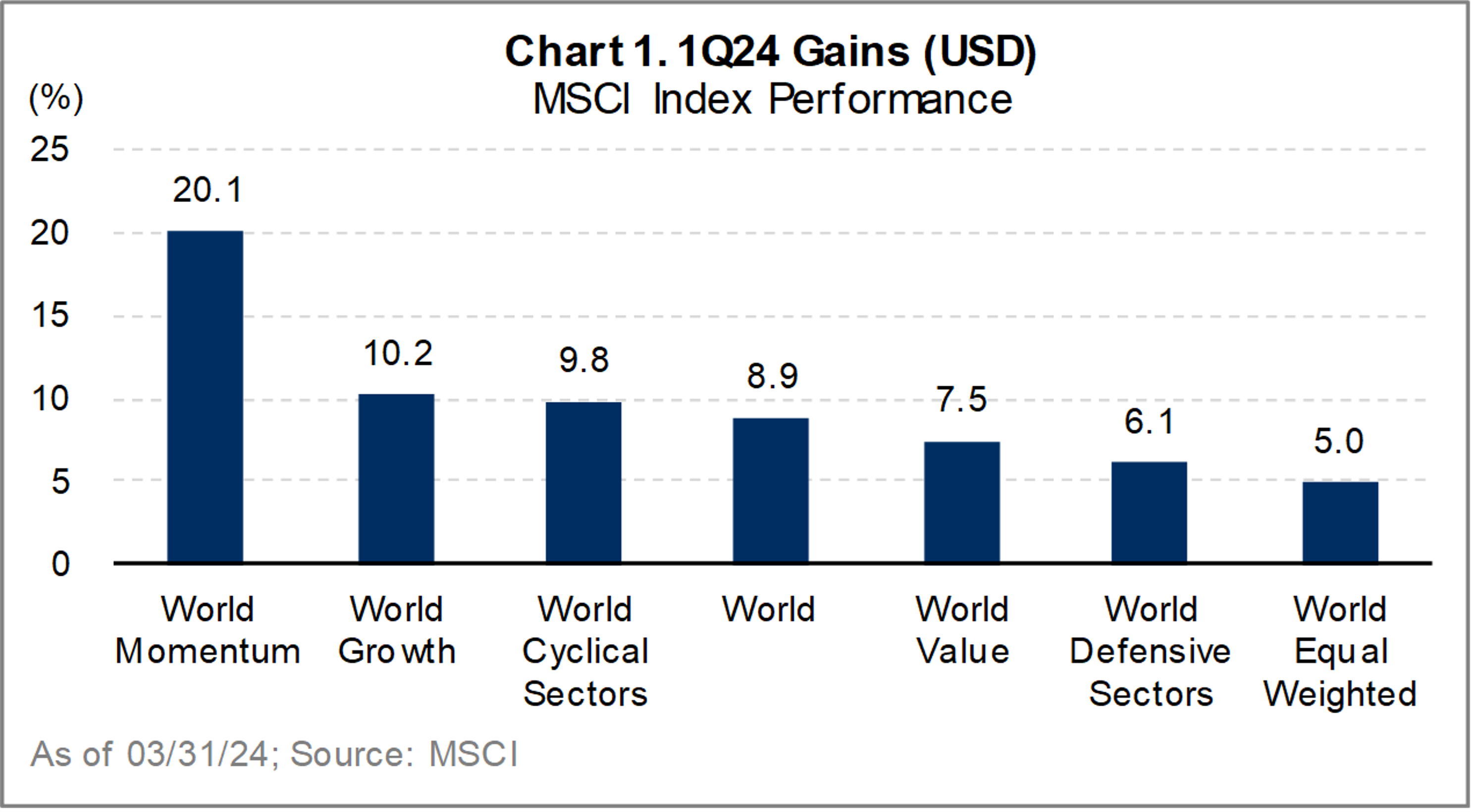

Global equities gained 8.9% (MSCI World Index, as measured in US dollars), ending the first quarter at record-high levels. Momentum stocks had their best quarter since Q3 1999 (MSCI World Momentum +20.1%), and narrow market leadership continued (Chart 1); by comparison, the Altrinsic Global Equity portfolio gained 5.2% gross of fees (5.0% net).i Our underweight exposure to sectors leveraged to AI enthusiasm and a lower overall risk profile were partly responsible, but poor performance by some of our important investments was a major contributor. We believe that many of the issues surrounding Charter Communications, Biogen, HDFC Bank, and Crown Holdings will be short-lived, but we are disappointed, nonetheless.

Perspectives

Economic Resilience, Earnings Vulnerability

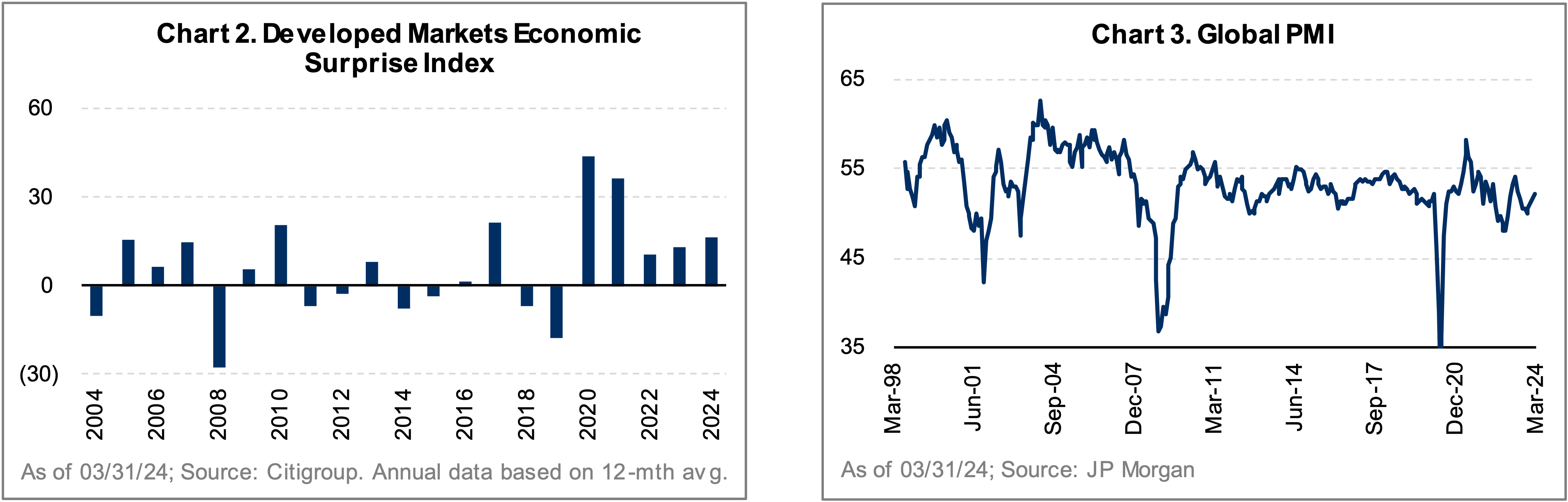

The global economy’s resilience in the face of tighter monetary policy has been impressive. Recession was a consensus view just 18 months ago, but that perspective has faded dramatically following six quarters of better-than-expected global economic data (Chart 2). Global PMI data, a popular measure of corporate activity and confidence, remained in positive territory (Chart 3), as weakness in many areas of the manufacturing sector was offset by robust service demand. Massive government stimulus (amounting to more than 26% of GDP in the US), continued deficit spending, and the drawdown of excess savings have also played a supportive role. Has monetary policy lost its influence on economic activity, or has it simply been delayed?

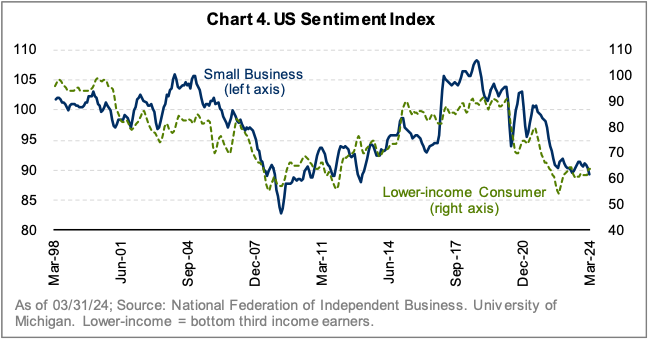

The path forward is not simple. Government budget deficits remain elevated, and the full impact of higher prices and interest rates has yet to be felt. Large corporations and wealthy consumers are demonstrating resilience, but there are signs of weakness elsewhere. In many developed markets, including the US, small businesses are increasingly struggling under the weight of higher borrowing costs, wage inflation, and slowing demand. Lower-income consumers continue to pull back spending as they contend with inflation and higher interest rates. Recent results from retail, restaurant, and apparel companies reflect this trend. Thus, while equity investor optimism is near all-time highs, small business and lower-income household confidence is closer to multi-decade lows (Chart 4). Weakness in small business sentiment is particularly important, as these companies account for more than half of employment in many countries.

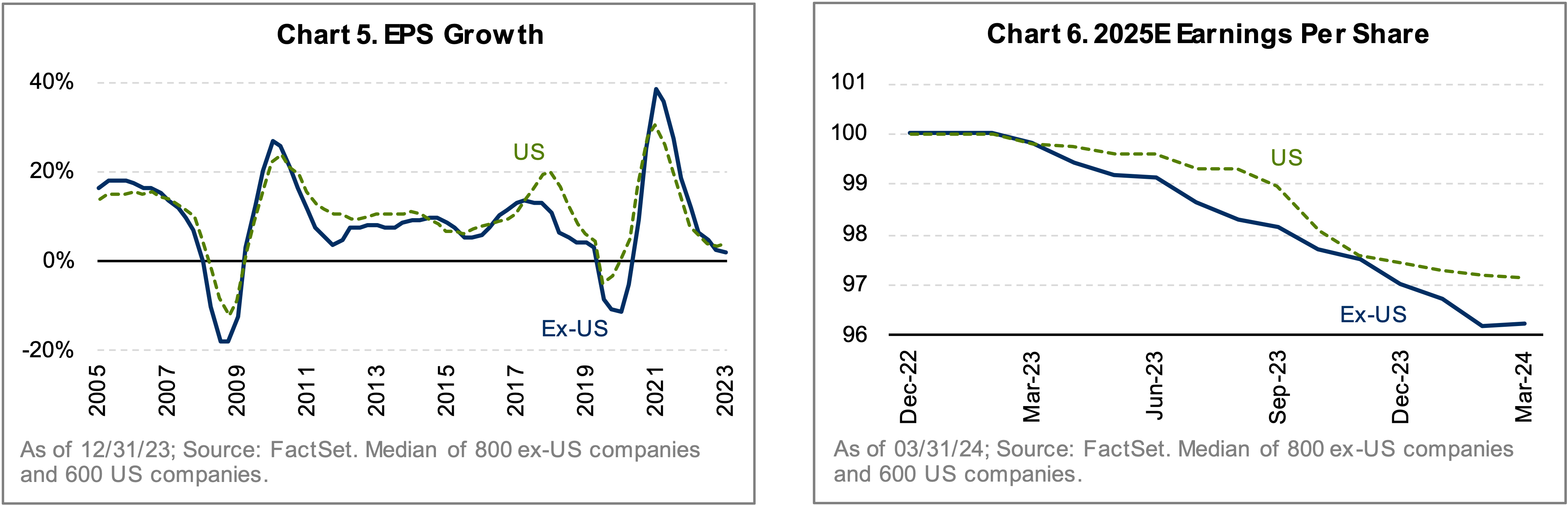

It is not surprising, then, that global corporate earnings growth is continuing to slow, driven by a combination of weakening demand, pricing fatigue, and sticky costs. In 2023, the median company’s EPS growth rate was the weakest in decades, outside of recessionary periods (Chart 5). EPS downgrades stabilized in Q1 (Chart 6), but consensus still expects a robust 9% EPS CAGR over the next two years, which we believe is a high bar to clear.

Narrow Market

Leadership with Indications of Broadening While global equity markets continue to reach fresh highs, this is largely due to the continued narrow leadership of a few large-cap growth equities. We have begun to witness bouts of strength among highly cyclical stocks, including during the first quarter, but this broadening out is in a very early stage. Given the extent to which valuation differentials and expectations are stretched, some of the tangible catalysts already in place include long-term regime changes in interest rates, inflation expectations, and tax policy, as well as intensifying regulation and intensifying competition in previously monopolistic tech verticals.

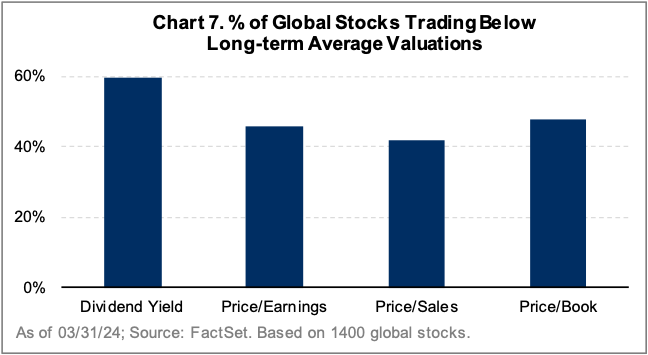

The average global stock has underperformed the MSCI World Index by 34.4% over just the last five years.¹ From our perspective as bottom-up, global investors, this prolonged concentration of outperformance by just a handful of stocks creates a significant opportunity set elsewhere. There are many companies that are improving capital allocation, product innovation, and cost management, both due to industry and company-specific evolutions. Valuations remain attractive, with about half of all global stocks trading below long-term average earnings multiples (Chart 7). Just as we saw during previous market peaks – TMT bubble, pre-GFC – there are plenty of compelling investment opportunities away from those capturing the headlines – for those willing to look.

Change Underway in Japan: Glacial in Scale, Glacial in Speed

The Nikkei 225 was the best-performing developed market index during the first quarter, gaining 28.6% in local currency terms and finally returning to its prior peak – in 1989! Weakness in the yen versus the US dollar offset some of these gains. Change in Japan is taking place on multiple fronts, with several compelling forces capturing investor interest. The Bank of Japan recently ended its Negative Interest Rate Policy (NIRP), marking the end of a period defined by extraordinary monetary easing. We are also beginning to see rising inflation following decades of deflation and disinflation. Meanwhile, new corporate reform initiatives promote shareholder returns and reduce cross-shareholdings. The impact of these reforms will be glacial in scale but also glacial in speed.

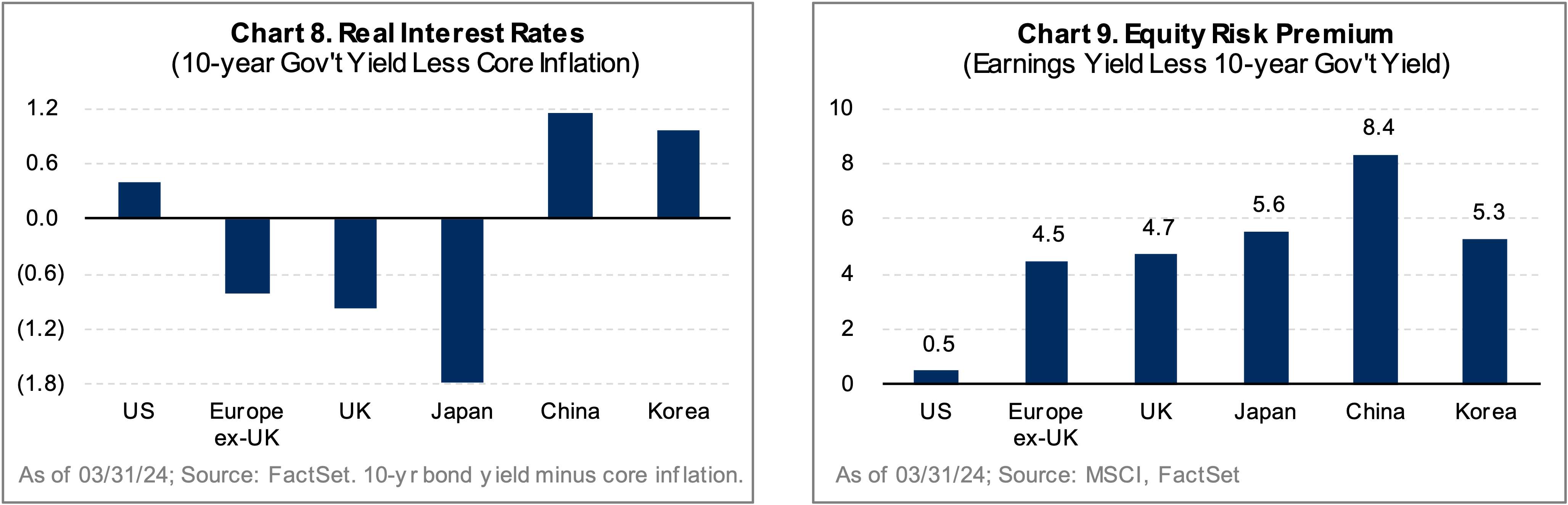

While the interest rate outlook is marching higher, real interest rates in Japan remain among the lowest in the world (Chart 8), incentivizing risk-taking and aiding growth. At the same time, equity valuations relative to bond yields are among the more attractive in global markets (Chart 9).

At a company level, operational efficiency and corporate governance are improving but remain low by global standards – not to mention US standards. We see progress, but it is more incremental than transformative, and recent improvements in profit margins may have more to do with rebounding economic activity than corporate reform. Having been investing in Japan for our entire careers, we see a big opportunity but also recognize that Japan is slow to change – and any delay might disappoint investors new to the market. Our exposure includes positions in Suzuki Motor, Kubota, and Makita. Suzuki is growing its EV offerings in Japan while broadening its product portfolio in India and other emerging markets. The company has been returning excess cash to shareholders through higher dividends and its first share buyback in a decade. Kubota, a global supplier of construction and agriculture equipment, is a beneficiary of increased infrastructure spending in the US and rising farm mechanization rates across Asia. Despite this, the company continues to be perceived as a low-growth, highly cyclical business. As a leading producer of battery-powered tools, Makita is well-positioned to benefit from the rising penetration of cordless tools for professional users. Increasing input and supply chain costs have depressed margins, and current valuations imply little improvement despite pricing initiatives, easing costs, and improved operating efficiencies.

A Few Words on Risk

Our primary objective is to identify a select portfolio of companies that can deliver outsized long-term performance while considering the range of risks surrounding these investments – including, but not limited to, macro risk. Among the many risk factors we consider in our analysis, a few are worth noting in the current investment environment:

- Inflation could prove stickier than many believe. Uncertainty surrounding the contributing factors (unsustainable deficits, trade wars, de-globalization, geopolitical risks, costs associated with the green transition, uncertain energy prices) produces greater volatility in rates. There is a wide range of outcomes related to inflation and rates, all of which are very different from the benign conditions that persisted in the decades leading up to the COVID-19 pandemic.

- While investors are obsessed with soft or no-landing scenarios, elevated inflation introduces growth risk and stagflation as possible macro outcomes.

- The implications of transitioning from QE to QT are unchartered territory, and the many benefits of QE will likely come with associated costs as QT unfolds.

- Geopolitical issues are well-telegraphed, but the risk of miscalculations leading to escalation in many areas is significant – and growing.

- Liquidity considerations introduce an array of risks. From a monetarist perspective, the world is awash with liquidity, and contraction can weigh on speculative asset prices and economic growth. From an investment perspective, liquidity related to trading volumes in many segments of equity and bond markets is low, contributing to increased risk of dislocations.

Performance Summary and Investment Activity

The market leadership of 2023 – namely growth, cyclical, and momentum stocks – continued into Q1 2024. In this environment, the Altrinsic Global Equity portfolio generated positive performance (due in part to our financials and industrials holdings) but lagged the broader market due to our underweight exposure to those leaders and poor performance by investments in communication services, health care, and information technology.

In communication services, Charter Communications’ stock price was down 25% on slowing subscriber growth and elevated capital spending. Charter has several avenues for growth, including share gains from legacy DSL competitors, broadening their product portfolio into mobile, and an acceleration in network expansion. The current valuation implies de minimis growth, a sharp contrast to our view that free cash flow can double in three years.

Health care stocks Ionis and Biogen came under pressure due to delays in bringing promising drugs and technology to market. Investors greatly underestimate the potential future success of Ionis’s innovations and the enormous addressable market for Biogen’s Alzheimer’s drug.

Information technology’s negative attribution had more to do with what we didn’t own – namely, US largecap technology companies. From a stock-specific perspective, two other notable laggards were beverage can-maker Crown Holdings and Indian bank HDFC Bank. Crown Holdings is facing cyclically depressed volumes and rising working capital requirements, which is hindering free cash flow. However, we see these issues as temporary and expect attractive growth ahead due to improving industry discipline and a continued consumer shift from plastic bottles to metal cans. HDFC Bank has struggled to integrate a recent acquisition, but we see this as a temporary phenomenon. We expect the company to utilize superior technology and customer service to gain market share and compound profits as it benefits from considerable investments and excess capital.

Industrials and financials were the primary sources of positive attribution in the quarter. Industrial holdings Acuity Brands, Daimler Trucks, and Bureau Veritas all had thesis-confirming earnings results. Under new leadership, Acuity has been gradually transitioning its leading lighting business away from more commoditized areas while improving costs to a level more commensurate with peers. Daimler Trucks continues its post-spin-off turnaround, including right-sizing its manufacturing footprint and cost base, leading to strong 2024 guidance and a rally in the shares. Bureau Veritas, a leader in testing and inspection, continues to improve its growth and free cash flow under a new CEO. Strength in financials was also stockspecific. Korean bank KB Financial rallied on the potential for reduced regulation of dividends and buybacks, along with continued strong fee income execution. Spanish bank BBVA continued to expand its ROE, as its crown jewel Mexican franchise benefits from higher interest rates and considerable digital investments. Leading insurer Chubb guided to solid profit growth in 2024, as it continues to see strong demand and an improving competitive backdrop. Lastly, Willis Towers Watson is finally turning around its growth and free cash flow after years of disappointment, leading shares to rally sharply in Q1.

This quarter we established positions in Spanish bank Bankinter, German exchange operator Deutsche Boerse, and French beverage maker Pernod Ricard. Bankinter can improve ROEs (to the mid-teens, from low double-digits currently) through a combination of its superior cost structure, customer service platform, higher-for-longer interest rates, and a far more disciplined competitive backdrop. Deutsche Boerse continues to find new avenues for growth through its FX, commodity, and interest rate products, which when combined with improved cost management, should lead to considerable free cash flow growth in the years to come. Pernod Ricard’s shares have de-rated sharply on post-COVID demand normalization and some weakness in emerging markets (particularly China), but we believe the franchise’s long-term ability to improve premiumization and compound profits is greatly underestimated.

We exited our positions in Kinross Gold, Novartis, and Vodafone, deploying funds to more attractive riskreward opportunities. Kinross shares rallied sharply over the last 18 months after a period of disappointments, and we believe shares reached fair value given some ongoing execution questions. Novartis has greatly improved its innovation and capital allocation in recent years, and the stock price reflected much of this upside potential. We sold Vodafone as we expect the company to struggle with free cash flow growth due to high product penetration, high competitive intensity, difficult regulation, and continued cost inflation. The shares remain cheap – but cheap for good reason.

Summary

We see the greatest risk in the popular and crowded segments of global equity markets, with the greatest opportunity among those companies away from the mainstream. The wide gap in valuation differentials, current earnings expectations, and the underappreciated positive change taking place in many companies contribute to our optimism. The complacency in markets concerns us, but we have great conviction in the long-term opportunity embedded in our investment portfolio – and the associated risk profile.

Please contact us if you would like to discuss these or other matters in detail. Thank you for your interest in Altrinsic.

Sincerely,

John Hock

John DeVita

Rich McCormick