Dear Investor,

The Altrinsic Global Equity portfolio gained 1.4% (1.2% net) during the second quarter, as measured in US dollars. This compares with the MSCI World Index’s 6.8% return, culminating in our worst quarterly underperformance in the firm’s 23-year history.i Narrow market leadership by highly priced US growth stocks has been a thorn in our side, and we have written extensively about the combination of factors that would cause markets to broaden out. Despite the most significant of these conditions being well underway (rising rates and inflation uncertainty), the lack of breadth in markets has returned to historically extreme levels, with enthusiasm surrounding generative AI contributing to the surge.

AI is a significant technological innovation, but we believe it is being greatly overhyped and overestimated in the short term, as is typically the case with new technologies. Stock prices for leading “AI stories” discount growth rates that will be difficult to achieve, thus impairing their underlying margins of safety. Although there are pockets of excess and exuberance, 68% of global stocks underperformed the MSCI World Index in the second quarter – and 44% actually declined – leaving many companies offering very compelling risk/return propositions. We see opportunity among companies embracing AI in their operations to enhance their business quality and efficiency, most notably in health care, non-life insurance, exchanges, global consumer franchises, industrials, and business services, to name a few.

Performance Summary

Our relative performance suffered from growth stock market dominance, a few disappointing investments (discussed below), and no specific holdings that kept up with the surging tech leaders. Putting this surge into perspective, the NASDAQ gained 12.8% during the quarter and had its second strongest first half in history. The greatest sources of negative attribution in our portfolio came from the technology, consumer discretionary, communication services, and financials sectors.

Technology (-232 bps) was the greatest detractor, primarily because of what we did not own; Nvidia (+52%), Apple (+18%), and Microsoft (+18%) combined for over 150bps of negative attribution. Consumer discretionary (-115 bps) suffered by not owning Amazon and Tesla (each +26%) and poor performance by holdings Advance Auto Parts and Alibaba. Advance Auto Parts, an auto aftermarket retailer, is well positioned to capitalize on an aging car fleet and robust miles driven. Poor inventory management and a botched direct sourcing initiative caused margins to plummet. We sold our position, as we lost conviction in management’s ability to close the margin gap to peers. Alibaba continues to improve profitability but has struggled to grow sales amid an uncertain Chinese economy and increased competition. Management is taking steps to drive sales growth while improving shareholder value via increased returns and monetizing non-retail assets.

In communication services, not owning Meta (+35%) and Alphabet (+16%) detracted 76 bps from performance. Additionally, Baidu was adversely affected by the slow Chinese recovery, and Liberty Global faced slowing cash flow growth amid delayed pricing initiatives, contributing to our underperformance. Several of our financials (-72 bps) stocks performed well, but some insurance holdings (Hanover Insurance, Everest RE, Chubb) were weak on fears of peaking profitability. We remain confident in the underlying fundamentals and expect rising demand, continued price hikes, and higher interest rates to generate resilient returns for investors in the medium term.

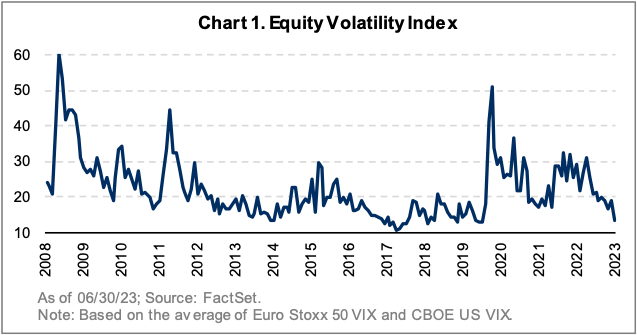

Many things in life are cyclical, which is certainly true with investing. History shows that fear gives way to greed (and vice versa), great ideas often go too far, and stocks and styles often reach extremes before normalizing (and then often overshooting in the opposite direction). The VIX Index (an indicator of expected market volatility) fell nearly 30% this quarter (Chart 1) and is near multi-decade lows, implying a high degree of market complacency. This complacency, coupled with high valuations in large growth stocks, suggests a preponderance of greed being reflected in many popular areas of the market. Our discipline, longterm perspective, and risk tolerance have led us elsewhere in pursuit of our objectives.

Perspectives from the Road

Our research efforts have been robust this year, with extensive due diligence visits to China, Japan, South Korea, Taiwan, Continental Europe, Scandinavia, the UK, India, and Brazil. Each trip is different but generally involves meetings with company management and operations teams, government officials, regulators, industry experts, and others in our network offering useful perspectives.

Our visit to China included stops in Shanghai and Chengdu, among other cities. Meetings and on-the-ground observations made it clear that China is experiencing the opposite market dynamic from the US. An uneven economic recovery has led to disparate sentiment across sectors in the US, but Chinese economic growth has been underwhelming since the January re-opening, broadly pressuring stock prices and prompting calls for more aggressive government stimulus. Discussions with local contacts suggest activity is returning, albeit uneven, with more nuanced government support than during previous cycles. While we wait for economic activity to normalize, companies like Alibaba and Baidu are undertaking shareholder enhancement measures, including simplifying operations and returning excess capital to shareholders. These actions highlight how undervalued their core e-commerce and search businesses are.

Several different European trips involved meetings in the UK, Scandinavia, and Germany. A warm winter provided relief to the European economy, as lower demand for energy cooled prices and minimized warinduced supply concerns. Geopolitical uncertainties in Russia, while unfortunate, are less impactful, as the continent’s reliance on Russian energy has dropped since last year. Inflation is declining, but policymakers remain vigilant in raising rates, clouding the economic outlook. As in the US, the impact of rising rates is yet to be fully realized, and the change will be long-lasting. We remain overweight in our exposure to Europe, with investments primarily in the consumer staples, financials, and health care sectors. Each have organic growth paths less reliant on economic growth with ample opportunities to increase profitability through efficiency and other management initiatives.

Traveling to Japan demonstrated that value exists – on the streets and in the stock market. For the first time in our careers, everything in Japan (except hotel rooms) feels inexpensive – food, transportation, experiences, and many stocks included. The yen’s undervaluation is collateral damage from the Bank of Japan’s policies to suppress rates via its Yield Curve Control (YCC) policy and the resulting inflation. Having suffered deflation or disinflation since its asset bubble burst more than three decades ago, there is greater reluctance to control inflation for fear of overcorrecting and falling back into the deflation trap. The result is continued pressure on the yen – and our preference for companies with pricing power. Since it has been 20 years or more since Japan Inc. has raised prices, it remains to be seen if corporates can follow through. Still, management teams embracing the principles of financial productivity and generating long-term shareholder value have a tremendous opportunity to drive investor interest. Our current exposure is approximately 8% via companies in the financials, industrials, and health care sectors.

Within emerging markets, we visited Taiwan, South Korea, India, Brazil, and the aforementioned China. Emerging markets in general are in a much better position than in previous down cycles, as central banks have been more proactive in tightening policy rates than their developed market peers, and political leaders are managing deficits more responsibly. Currency valuations are depressed versus Western currencies and the US dollar, specifically. There is a growing list of investments with attractive business models, deeply discounted valuations, and seasoned management teams accustomed to operating in volatile environments. This presents an increasingly attractive investment proposition.

Our trip to Brazil was timely given the challenging investment landscape characterized by political risks, volatile inflation, currency depreciation, and high financial leverage. These factors have driven valuations to rock-bottom levels, reflecting the weak sentiment we witnessed among investors on the ground. However, our meetings highlighted that, contrary to common perception, higher-end consumers and large corporations represent pockets of resilience within the economy. Having avoided the high leverage that has plagued small businesses and the average consumer, there are a handful of overlooked companies with proven business models, improved balance sheets, and years of experience operating through volatility. Currently, we are invested in two Brazilian stocks. The first is Itau Unibanco, a leading private bank that caters to high-end households and large corporations, which is trading near all-time lows on price-to-normalized earnings despite its strong capital and risk management. The second is Lojas Renner, a top apparel retailer with a renowned brand, a net cash balance sheet, superior operational capabilities, and opportunities to expand its ecommerce offering. Despite these strengths, the stock is trading near all-time low valuations.

Individual companies and countries have their own risk factors and idiosyncratic growth drivers, but many of the risks present today stem from broader macroeconomic dynamics. Geopolitical risks are well telegraphed; regardless, they must always be respected. Corporate earnings expectations in Western nations have been revised downwards; a pattern of continued declines represents a significant risk for many companies. Changing liquidity conditions could be the greatest risk of all.

The world has been awash with liquidity as policymakers responded to the pandemic by experimenting with massive fiscal and monetary stimulus (i.e., quantitative easing (QE)). Policy measures are now tightening in most large economies (excluding China), but they remain very loose. In the world’s largest economy, US short term interest rates have risen 500 bps, and the money supply has dropped by $669B as debt purchased in QE measures is not rolled over. At the same time, the US Treasury is about to initiate massive debt issuance to fund swelling deficits. The “transitory” path toward policy normalization amidst uneven economic growth, societal conflict, and inflationary pressures is unlikely to be smooth, presenting an underappreciated risk, particularly to the most inflated segments of the market.

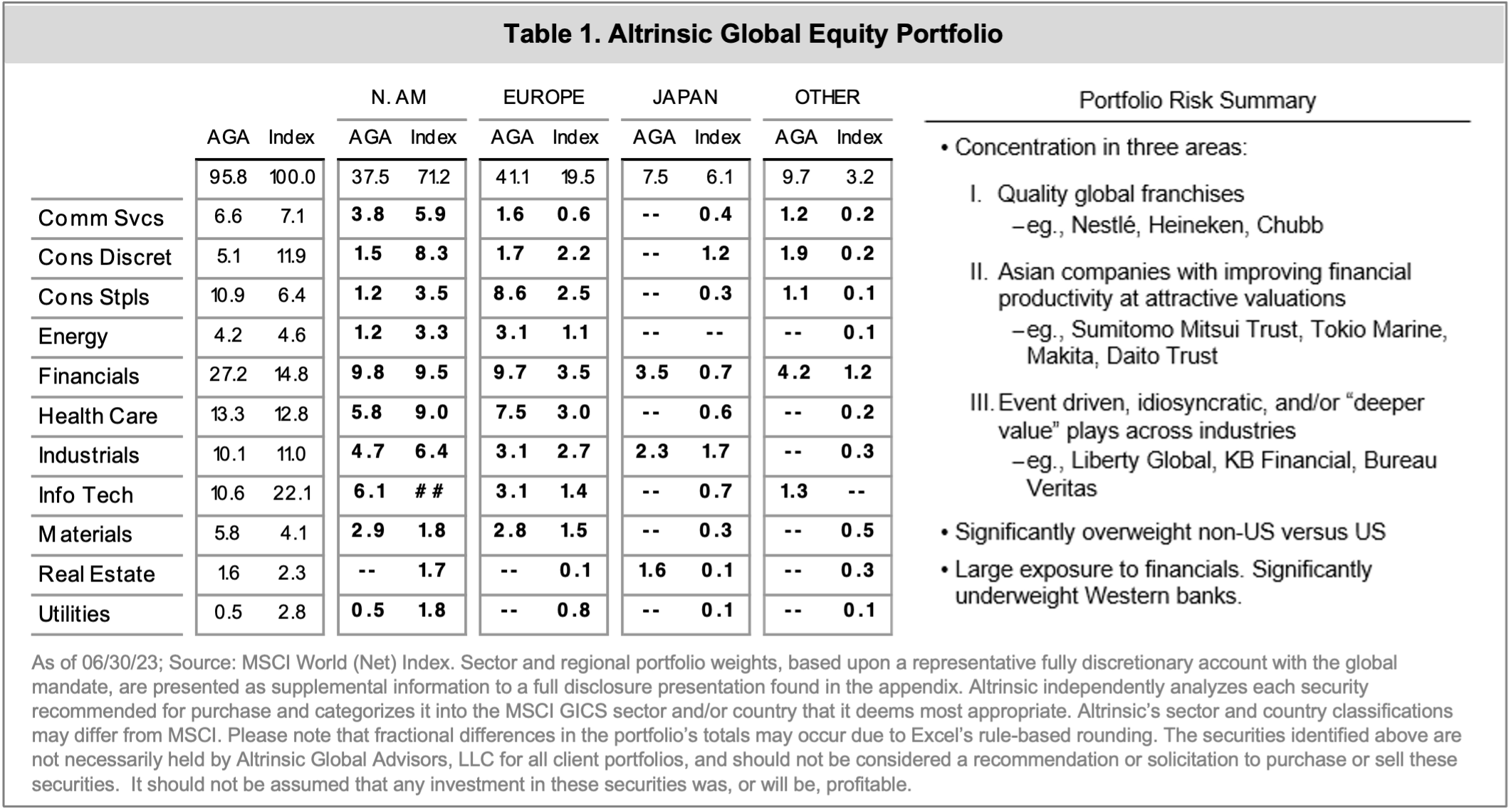

Despite these important risk considerations, meaningful pockets of opportunity exist away from crowded large cap AI and other growth stocks. Our global equity portfolio is positioned very differently from the benchmark at the stock-specific, regional, and industry levels (Table 1), resulting in one of the lowest portfolio risk levels in years, as measured by beta (0.72)1 . We are an outlier, which can be a challenging position, but it is often most important and appropriate to remain disciplined when the associated discomfort is greatest.

Summary

It is more important than ever to be disciplined and not follow the crowd when operating in an environment characterized by excessive complacency, robust liquidity, and unprecedented narrow market leadership. This scenario can test one’s internal fortitude and has certainly tested ours. We respect and admire many large cap market darlings, but massive market capitalization and valuations contribute to unfavorable risk/return profiles. As evident in our portfolio holdings, we are finding very attractively-valued and high-quality businesses elsewhere that we believe will benefit in what will likely be a very different investment environment than the past.

Please contact us if you would like to discuss these or other matters in greater detail. Thank you for your interest in Altrinsic.

Sincerely,

John Hock

John DeVita

Rich McCormick