Dear Investor,

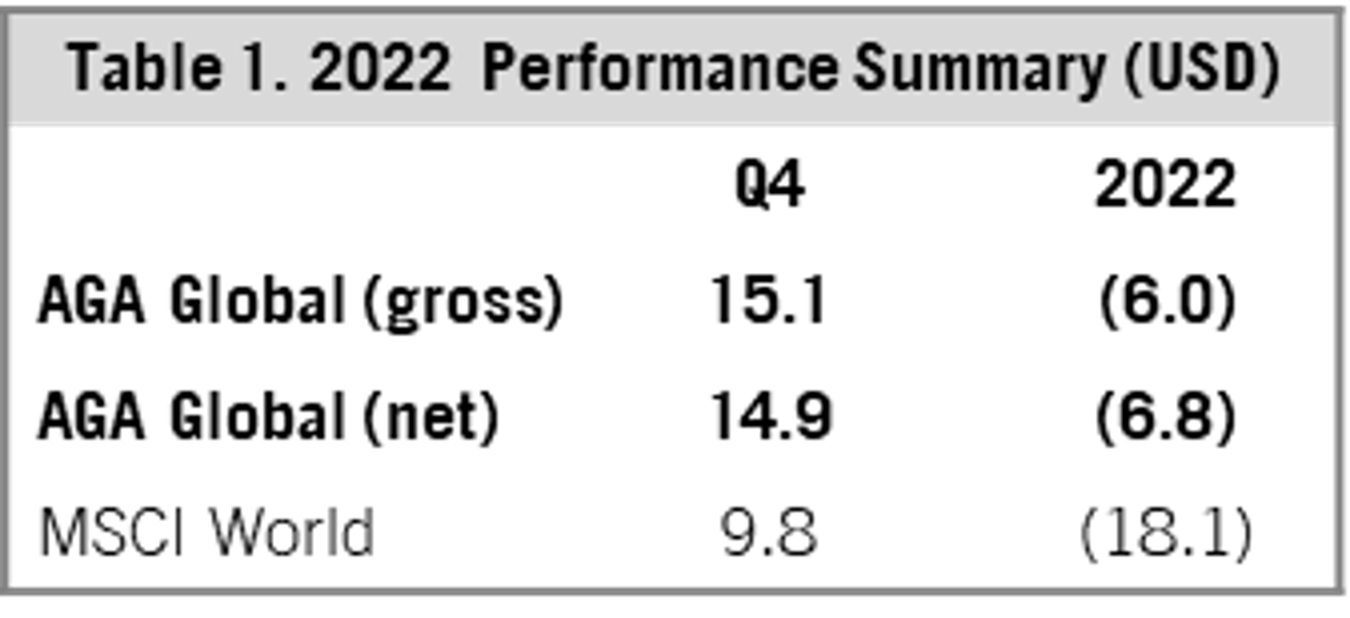

Global markets recovered strongly during the fourth quarter, aided by falling inflation expectations, optimism that the US Federal Reserve would move away from aggressive policy tightening, an improved energy outlook in Europe, and President Xi’s unexpected decision to unwind zero-COVID policies. The rally was certainly welcomed, but 2022 was the most challenging year since the global financial crisis. According to Michael Howell of CrossBorder Capital, global investors lost US$23T of wealth in housing and financial assets in 2022, equivalent to 22% of global GDP and greater than the US$18T of losses suffered in the 2008 financial crisis.1 Commodities were the only refuge, as long-term bonds had their worst year since the 18th century (according to the Financial Times) and equities fell 18.1% in 2022 (MSCI World Index) even after rising 9.8% in the fourth quarter, as measured in US dollars. The Altrinsic Global Equity Portfolio outperformed global markets, declining 6.0% for the full year and gaining 15.1% for the fourth quarter (Table 1).i

Fourth Quarter Performance Review and Investment Activity

Our investment activity leading up to 2022 largely involved companies whose future growth was not highly dependent upon the broad economy and/or companies with idiosyncratic drivers of value creation that were within their control. There was dangerous crowding in the popular “growth” stocks and extreme valuations for the large index constituents. These conditions, coupled with our investment discipline, led to a materially different portfolio than benchmark indices, including below-market risk (beta), and was the primary source of our relative outperformance in 2022.

At a more granular level, the most significant sources of positive attribution in the quarter were our investments in the financials, consumer discretionary, and information technology sectors, offset partially by our investments in the traditionally defensive health care and consumer staples sectors.

In the financials sector, our insurance-focused holdings rallied due to continued positive competitive momentum, particularly in reinsurance. Insurance broker Willis Towers Watson (WTW) continued to improve operational performance following its failed merger attempt with Aon. With that distraction removed, WTW is focused on employee recruitment and retention as well as increased efficiency. Insurers Everest Re and Chubb were strong performers as the dynamics within the insurance industry continued to improve. Rising rates are forcing competitive discipline and weeding out weaker underwriters, while Chubb’s and Everest Re’s efficiency and scale are accruing to the benefit of customers and shareholders.

In the consumer discretionary sector, our performance was positively impacted by China’s move away from zero-COVID restrictions. The abrupt turnaround buoyed travel and leisure businesses Trip.com and Las Vegas Sands. Although a return to normalcy will not follow a straight line, with the worst-case scenario eliminated for each company, we expect vastly improved 2023 operational performance. Not owning highly valued market darlings Amazon and Tesla also benefited performance. We greatly admire their products and services, but valuations were – and remain – impediments.

Within the information technology sector, software provider Oracle showed healthy cloud-based product demand and closed its acquisition of medical IT systems leader Cerner. Oracle’s database strength is particularly well suited to capitalize on data security trends in health care and widens the company’s scope for margin expansion. Like the consumer discretionary sector, not owning large index constituents Apple and Microsoft also proved beneficial.

The primary sources of negative attribution were investments in the health care and consumer staples sectors. In health care, Medtronic faced lingering pandemic effects on surgery demand, but we believe its capable management team is incentivized to capture the growing addressable market for cardiovascular, neurological, and renal interventions.

In the consumer staples sector, beverage providers Diageo and Heineken lagged given the defensive nature of their cash flows, but both have compelling value creation opportunities in their premium portfolios, global footprints, and a newfound focus on sales and marketing efficiencies.

Our investment activity during the fourth quarter involved establishing new positions in six companies and exiting five. Broadly, purchases were in line with earlier activity – adding companies in more cyclical areas (industrials, emerging markets, and banks) that became oversold considering their long-term, fundamental prospects.

We initiated positions in premium tire maker Michelin and aluminum can producer Crown Holdings. Each exhibits dominant market share and benefits from secular industry trends – rising EV/SUV sales and beverage can penetration, respectively. We also initiated a position in Brazilian retailer Lojas Renner, which is leveraging its leading apparel and lifestyle franchise to expand into the attractive ecommerce and omnichannel markets. Two banks were added to the portfolio: Spanish bank Banco Bilbao Vizcaya Argentaria (BBVA) and Brazilian bank Banco Bradesco. BBVA has simplified its banking portfolio in recent years, and its highquality Mexican and Spanish divisions are heavily discounted due to manageable risks in its Turkish division. Banco Bradesco is one of Brazil’s largest banks and has considerable opportunities to grow returns through its industry-leading insurance business in an underpenetrated market. Lastly, we re-initiated a position in Japan Exchange Group, as valuations do not reflect the significant growth opportunities for passive investing in Japan.

We sold positions in Continental AG and Aena, as we saw diminishing ability for each company to offset cost inflation in an increasingly challenging operating environment. We also exited Aon, AXA, and Otis, as strong operational execution caused shares to re-rate. We redeployed the capital into more compelling investment opportunities.

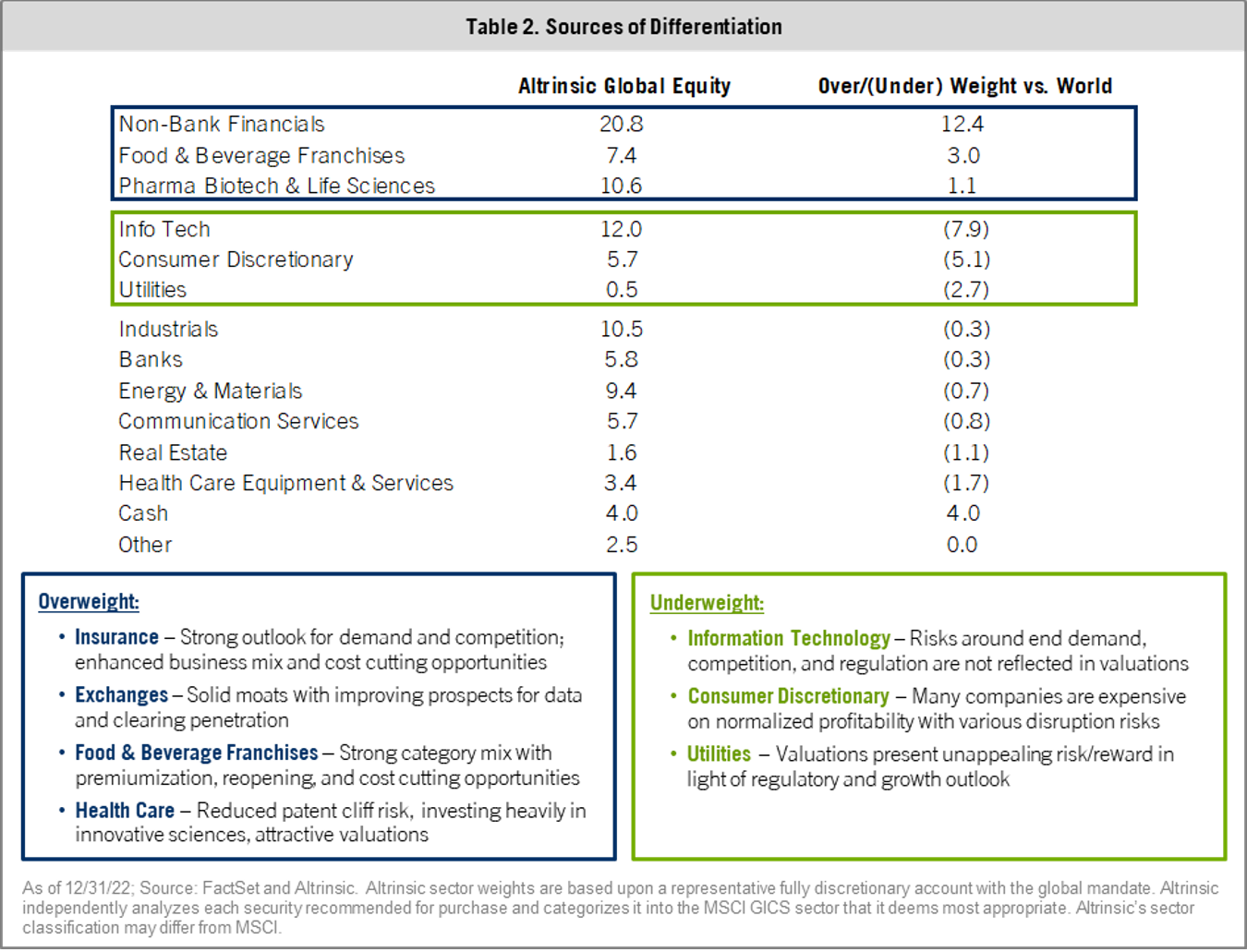

A summary of our portfolio positioning is illustrated in Table 2.

Perspectives

I. Regime Change

The shift in inflationary expectations and tightening monetary policies during 2022 marked a significant regime change with long-lasting implications. Over the last decade, subdued inflation, falling rates, and stimulative policies elevated valuations of long duration assets, including “growth” equities, to excessive levels. Those who benefitted most under the old regime (“profitless” technology companies, early-stage growth companies, and SPACs, to name a few) felt the initial brunt. “Growth” companies that became the largest index constituents and market leaders were among the hardest hit. Valuation did not matter until, inevitably, it did. As we sift through the ashes in our search for value, we are amazed by the excesses that still exist in these areas. The current situation reminds us of the post-TMT bubble (2000) when many companies either disappeared or were caught in a long purgatory. In the second case, there were two outcomes: either earnings caught up with inflated share prices or share prices fell to levels justified by the underlying quality of the business.

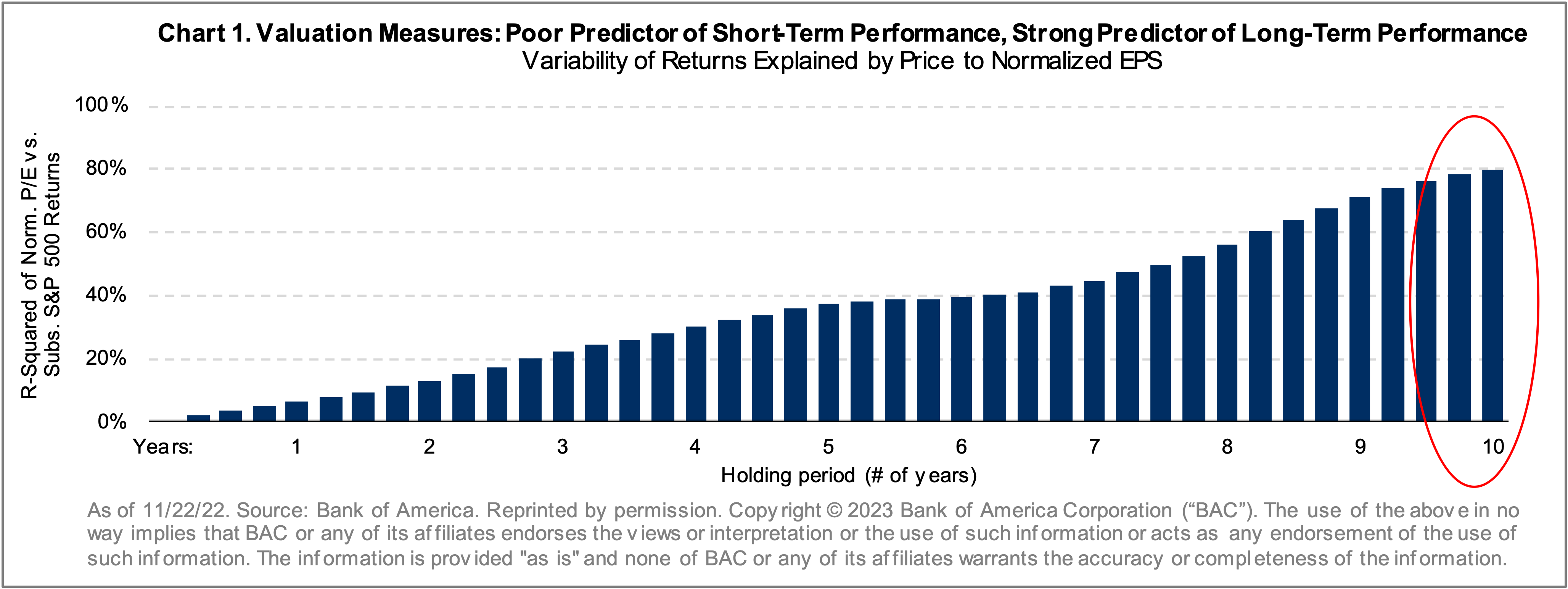

Above all else, 2022 reaffirmed that valuation matters – and it matters a lot. Historically speaking, valuation measures have little predictive power in determining short-term performance, as macro factors and other dynamics bear influence. Meanwhile, as shown in Chart 1 from Bank of America, valuation is the overwhelming determinant of long-term performance. Bank of America’s research is based on an analysis of US stocks, but it is our experience that this finding holds true in international markets as well. Perhaps unsurprisingly, business quality, valuation, and margin of safety are the pillars of our investment discipline.

A shifting regime, combined with a renewed focus on company valuations, supports further broadening out in markets. The leadership of highly-priced, long duration growth stocks and US equities has given way to other underappreciated segments of equity markets – non-US, in particular. We have discussed this transition in our commentaries throughout 2022 (Q1 | Q2 | Q3), and evidence suggests we are still in the early stages. Undervalued non-US currencies further support the growing opportunity.

II. From Macro to Micro

“The only thing we know about the future is that it is going to be different.”

– Dr. Peter Drucker, renowned author and management consultant.

Front pages are filled with macro risks – geopolitical (Russia/Ukraine, China/Taiwan, Middle East), economic (inflation, policy, recession, EU energy crisis), societal (inequality, COVID-19), and market (wealth destruction), to name a few. Risks are plentiful, and this risk landscape will likely persist for some time. Consequently, emotions are running hot, but we believe the temperature will subside. The risk premium assigned to a growing number of companies already reflects many prevailing concerns. Over time, things tend not to be as good as hoped but also not as bad as feared.

One macro risk factor we believe is not getting the attention it deserves is Quantitative Tightening (QT) and the shrinking of bloated central bank balance sheets. Central bankers’ extraordinary volume of bond purchases was a massive experiment that flooded the world with liquidity, artificially suppressed interest rates, and lifted asset prices. Like the broader regime change, QT is underway in the US, expected soon in Europe, and will inevitably happen in Japan; the global implications are unknown. The timing and pace of QT add to central bankers’ challenges when setting interest rate policy while juggling inflationary pressures and fragile economic conditions. The risk of policy errors in this area seems elevated to us. To paraphrase Warren Buffet, this is a movie that nobody has seen before, and therefore nobody knows how it will play out. If 2022 was overwhelmingly about macro events, micro developments are poised to define 2023.

Corporate earnings were resilient in 2022, but this will be the greatest fundamental challenge to markets in the near to intermediate term. The good news is that market observers are increasingly telegraphing this concern. The bad news is that the scope for EPS downside in many companies is greater than what companies are communicating and prognosticators are expecting. Supportive factors over the last decade – benign input costs, outsourced production, declining tax rates, and low interest rates – are reversing course, in some cases significantly. There is also a wide range of potential outcomes related to how a central bank-induced recession will affect corporate and consumer behavior after a period of excesses.

Although many companies are likely to deliver disappointing earnings results, it is important to remember that stock prices bottom long before earnings. Most of our new purchases this year involved cyclical companies with attractive long-term growth profiles where we believe share prices largely discounted the downside. Although one can never perfectly time or bottom tick an investment, the upside potential relative to the downside risk for many companies is very compelling.

Reflecting this positively-skewed risk-return tradeoff, we have seen an uptick in private equity activity involving public equities. We believe the return potential in public equities is meaningfully greater than in private markets. There is a tremendous amount of “dry powder” following massive PE fundraising efforts, and with the attractive propositions on offer in public markets, we expect to see a pickup in activity.

Notably, midcap software companies have become an area of interest. Most technology stocks remain overvalued, and many have questionable business models, but a growing number have fallen to prices near the discounted present value of their recurring revenues. Private equity investors have become active in this space, acquiring 12 software companies in 2022 at an average value of 10.4x EV (Enterprise Value) / NTM (next-twelve-months) sales or a median premium of approximately 39% to the prior unaffected price. Like other segments of the public equity markets, software company valuations are more attractive than those in private market transactions.

III. Regional Perspectives

While the US possesses many of the most innovative and highest-quality companies in the world, valuations remain above levels justified by underlying fundamentals in many cases. We continue to see more compelling investment propositions outside the US.

Europe has been the subject of the most unfavorable headlines and, not surprisingly, offers the cheapest valuations. Facing an energy crisis, a war on its periphery, and excessive debt in the southern regions, it is understandable that stocks are trading at meaningful discounts to US peers and relative to history. With uncharacteristic haste, European nations have made significant progress in reducing their dependence on Russian gas. After peaking in August2, European natural gas prices have fallen €350/MWh to €76/MWh3, aided by reduced consumption by consumers and industry, mild weather, and aggressive purchasing of liquefied natural gas to replace Russian supplies. Europe appears to be averting a shortage this winter, but we have two more months of winter, and European supply will remain tight until 2024/2025 when new LNG facilities come online. Barring Russia’s use of tactical nuclear weapons, the most significant near-term risk in Europe stems from ECB’s policy choices to control inflation and shrink its balance sheet while not destabilizing weaker southern European nations.

Our investments in Europe have been concentrated in global franchises in the consumer (Heineken, Diageo), health care (Sanofi, GSK, Medtronic), and financials (Willis Towers Watson, Chubb, Zurich) sectors. While not immune from some of the risks noted above, they operate globally, increasing revenue growth opportunities and reducing risk. Developments during the last year have led to new sources of value in more cyclical industries, including banks (BBVA), industrials (Sandvik), and materials (CRH).

Significant macro and micro developments are underway in Japan, increasing our interest. Conditions from decades of embedded deflation weighing on asset prices and mindsets appear to be transitioning. CPI levels have reached their highest level since 1991, the year we first visited the country when its bubble began to unwind. The BOJ has kept rates near zero as others tightened, contributing to the yen’s decline to the weakest levels since the late 90s. That is until December 20, when the BOJ surprised global markets by announcing an unexpected loosening of its yield curve control, sending Japanese bond yields and the yen sharply higher and generating global spillovers across debt, currency, and equity markets. This action potentially removes one of the last global anchors suppressing rates and borrowing costs. Our Japanese exposure has expanded to include companies in the financial, real estate, industrial, and health care industries and is differentiated from the large benchmark constituents. We believe Japan has significant value yet to be unleashed.

Similarly, compelling value exists within certain pockets in emerging markets. Pundits often refer to emerging markets as a homogenous group, but there are wide differences among countries politically, economically, and in fundamental investment appeal. At one extreme, the above-mentioned regime change and the strength of the US dollar are putting profound pressure on indebted nations with weak external balances (Pakistan, Sri Lanka, Turkey). On the other hand, many developing countries are ahead of developed nations in their policy response to inflation (Brazil and Mexico) and are on more solid footing. The largest EM country, China, has to address a property bubble and avoid falling into a perilous middleincome trap, and they are just beginning to open up post-COVID lockdowns. After lagging materially, we believe the combination of macro uncertainty, attractive valuation, and improving company fundamentals in EM presents compelling opportunities. During Q4, we established new positions and/or added to existing investments in China, Mexico, Brazil, India, and Korea. We have approximately 7% direct exposure (or approximately 21% if looking through to our holdings’ aggregate end sales exposure4) and are conducting extensive due diligence on a range of other EM companies.

Summary

The brutal performance of most asset classes during 2022 appears to be signaling an end to the macro regime of secularly declining interest rates, subdued inflation, abundant liquidity, and a view that valuation does not matter. Markets are nowhere near fire-sale levels, but a growing number of companies are providing investment propositions that are very favorably skewed to the upside. Adhering to our intrinsic value discipline, we will responsibly deploy capital in pursuit of the greatest risk-adjusted opportunities.

Thank you for your interest in Altrinsic.

Sincerely,

John Hock

John DeVita

Rich McCormick