Dear Investor,

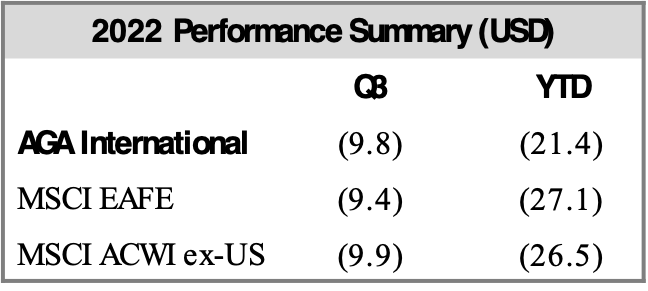

The downturn in markets continued during the third quarter as concerns over tightening monetary policy, inflationary pressures, weakening economic growth, and geopolitical risks intensified. Despite strong gains early in the quarter, the MSCI EAFE Index declined 9.4% (as measured in US dollars), ending approximately 27% below peak levels reached in September 2021. The Altrinsic International Equity portfolio declined 9.8% over the same period.i

Greed has given way to fear. We have not reached a stage of extreme capitulation, liquidity unwinds, or distress, but fear emanating from headlines and market declines is reflected in poor investor sentiment and the growing presence of value.

Risk factors could certainly deteriorate, with the greatest ones emanating from 1) geopolitical developments (Russia/Ukraine, China/Taiwan) and 2) deteriorating confidence in policymakers as they attempt to juggle both inflationary and recessionary pressures amidst a surging US dollar. While headline valuations look very enticing, we expect many companies to revise earnings downward – quite meaningfully in some cases.

Geopolitics: Uncertainty to Persist, as it Always Does

“In three words, I can sum up everything I’ve learned about life: It goes on.”

– Robert Frost

Geopolitical risks have escalated and are likely to remain elevated for years to come. Among the many contributing factors, the evolution from a Cold War era “bipolar world” (the US and its allies versus Russia and its allies) to the current “multipolar world” (US, Russia, China, North Korea, Middle East, non-state actors) is foremost. Additionally, advancements in the tools of warfare (cyber, drone, hypersonic missiles, and bioterror, to name a few) have resulted in a wider range of outcomes with lower predictability. Nobody can consistently forecast these outcomes and their timing.

Due to the increase in complexity and unpredictability of the geopolitical landscape, diversification is more important than ever. As we determine the price (valuation) that we are willing to pay for companies or other assets, we must do so in a manner that prudently underwrites the associated downside risk and upside potential. Our base case assumption is that the primary risks making headlines today will persist for the foreseeable future, but the emotion surrounding them will ebb and flow. Importantly, this marks a meaningful departure from the last decade, where a preponderance of factors supported company valuations – in many situations, rising to previously unimaginable levels. As is always the case in the long term, price matters.

Policy: Eroding Credibility and a Difficult Juggling Act

Policymakers around the world have their hands full with differing versions of a combustible brew – heightened inflationary risk and fragile underlying economic conditions. Additional fragility stems from mountainous debt levels, rising deficits, and the recognition that much of the recently experienced robust economic growth was largely “pulled forward” by extraordinary stimulus measures that are now behind us. Meanwhile, credibility has been languishing after completely misdiagnosing inflationary pressures as transitory. Most recently, fiscally irresponsible efforts to generate growth further eroded vital confidence, with the UK a notable example. UK Prime Minister Liz Truss’ proposal for unfunded, sweeping tax cuts and additional fiscal expenditures caused the pound to plunge and gilt yields to spike. The market and political uproar forced a quick policy reversal and the sacking of finance Minister Kwasi Kwartang. Confidence is difficult to earn, easy to lose, and very difficult to regain.

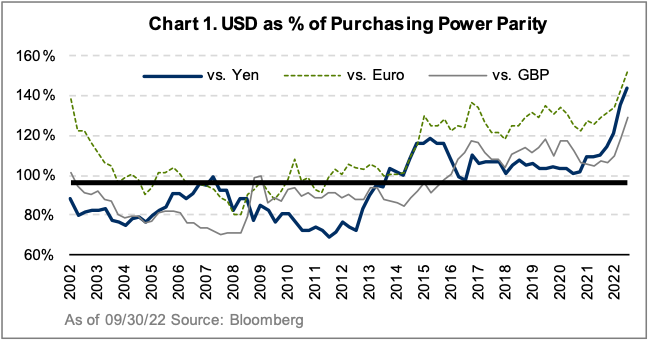

The strength of the US dollar adds to the combustible mix. As seen in Chart 1, the US dollar continues its climb well above fair value, as measured by Purchasing Power Parity and most other measures. Its momentum has been strong, supported by favorable interest rate differentials, relative economic strength, energy selfsufficiency, and its safe haven status. This strength comes with risk, given the US dollar’s central role in the global financial system and commodity pricing and the massive levels of dollar-denominated debt issued by fragile non-US issuers. Sudden and significant movements in global interest rates, a strong US dollar, and varying economic conditions around the world further amplify the associated risks. Historically, these dislocations have emerged where there was leverage, asset/liability mismatches, underlying liquidity risk, or algorithmic based models whose assumptions did not prove correct.

We do not believe anyone can forecast currency markets, including how far they will overshoot and when reversals will occur. However, it is critical to incorporate appropriately prudent assumptions into our models and decision-making process. We approach volatility in currency markets from the perspective of risk at two different levels. At the company level, we embed conservative, long-term, fair value assumptions. We pay particular attention to the business’s sensitivities to the wide range of potential currency outcomes. At the portfolio level, our consideration of hedging depends upon 1) the extent to which we are overweight (as measured against relevant benchmarks) and 2) the risk of absolute capital loss related to this unintended exposure. We currently have no hedges in any mandates and believe many non-dollar currencies and non-US assets are undervalued. Readers who are considering buying a warm weather property might want to consider Portugal rather than south Florida.

Earnings: First Came the Decline in P’s, Now the E’s

Much of the equity market decline year-to-date has been the result of valuation multiples (price-to-earnings) contracting since corporate earnings have been resilient. Despite major cost pressures stemming from supply chain disruptions, input cost inflation, and labor pressures, companies have thus far been able to raise prices and generate positive operating leverage. However, operating leverage works both ways. Customers (both consumers and businesses) have accepted higher prices to date, but we believe that their willingness and ability to do so are waning. The post-pandemic “YOLO” (you only live once) spending mindset is giving way to economic reality.

Valuations: Already Discounting a Lot of Bad News

While a pattern of corporate earnings downgrades presents one of the greatest fundamental risks in the near term, markets have already discounted this to varying degrees, as illustrated in Chart 2-5. These snail charts represent the evolution of consensus earnings estimates from 2017 to 2023F displayed over the representative market index. You can see the COVID-related earnings collapse and subsequent rebound to well above preCOVID levels. It is impossible to predict exactly when or where stock prices will reach a bottom, but we note that historically, stock prices typically bottom long before earnings, and a large degree of earnings decline is ‘baked in.’

Much of our portfolio activity during recent years involved investments in durable businesses, those less driven by the broad economy, and/or among well-capitalized companies executing on underappreciated initiatives to further strengthen their quality. These investments continue to dominate the portfolio, but as noted above, share prices of more economically cyclical businesses are beginning to discount a lot of negative news, leading to a growing number of stocks whose share prices have fallen well below their intrinsic values.

We have been asked frequently in recent years why we have invested less than many of our peers in what some refer to as “value sectors” (defined as lower-quality cyclical industries including materials, commodities, industrials, and banks). The short answer is that they have not offered value. The blend of historically peak profit margins, significant leverage, and more volatile financial productivity has made headline valuations appear artificially low. Essentially, cyclical businesses typically create cyclical opportunities that surface during recessions or other episodes of macro turbulence. We are beginning to see new opportunities emerging in these areas, particularly among 1) higher quality cyclical businesses in the industrial and materials sectors globally and 2) in less cyclical businesses that happen to operate in cyclical geographies (namely, emerging markets).

Investment Activity and Portfolio Positioning

Our investment activity during the third quarter included establishing new positions in Fidelity National Information Services (US), Hanover Insurance Group (US), Samsung Electronics (Korea), Fomento Economico Mexicano (Mexico), Sandvik (Sweden), and Haleon (UK – the consumer health care company spun out of GSK). We exited our positions in companies where management execution has not met our expectations (Fresenius Medical, Cognizant, and Accor), as well as our positions in Nintendo, AutoZone, FTI Consulting, and PepsiCo, as better opportunities emerged during the market sell-off.

Fomento Economico Mexicano (also known as FEMSA) operates specialty retail stores (convenience stores, pharmacies, and fuel) in Latin America and a growing logistics business in North America. It also has a controlling stake in the world’s largest Coke bottler franchise, Coca-Cola FEMSA. After several years of disappointing capital allocation, FEMSA has reorganized its business structure and is now well-positioned to increase penetration of its high-return OXXO convenience stores and improve returns for its Coca-Cola FEMSA division. There is additional optionality for further value creation through monetizing its assets under the new CEO Daniel Rodriguez.

Sandvik, a Swedish multinational engineering company, provides capital goods to general industrial and mining industries, with a growing proportion of revenues from value-added consumables. Sandvik has been making systematic improvements to its operations and capital structure, putting it in a stronger position today than in previous cycles. Decelerating industrial demand and cost inflation present near-term risks, but valuations have declined commensurately, providing an entry point with an improved risk-reward profile.

MinebeaMitsumi is a Japanese industrial company focused on manufacturing critical ball bearings, analog semiconductors, optical image components, and small motors, mainly for the automotive, consumer electronics, smartphone, and data center end markets. It is exposed to secularly growing niches, and its market positions are defendable with strong barriers to entry. The stock has come under pressure due to cyclical concerns and worries about the sustainability of semiconductor margins. While these concerns are understandable, we believe investors underestimate the company’s pricing power, margin improvement potential, and product penetration opportunities over the medium term.

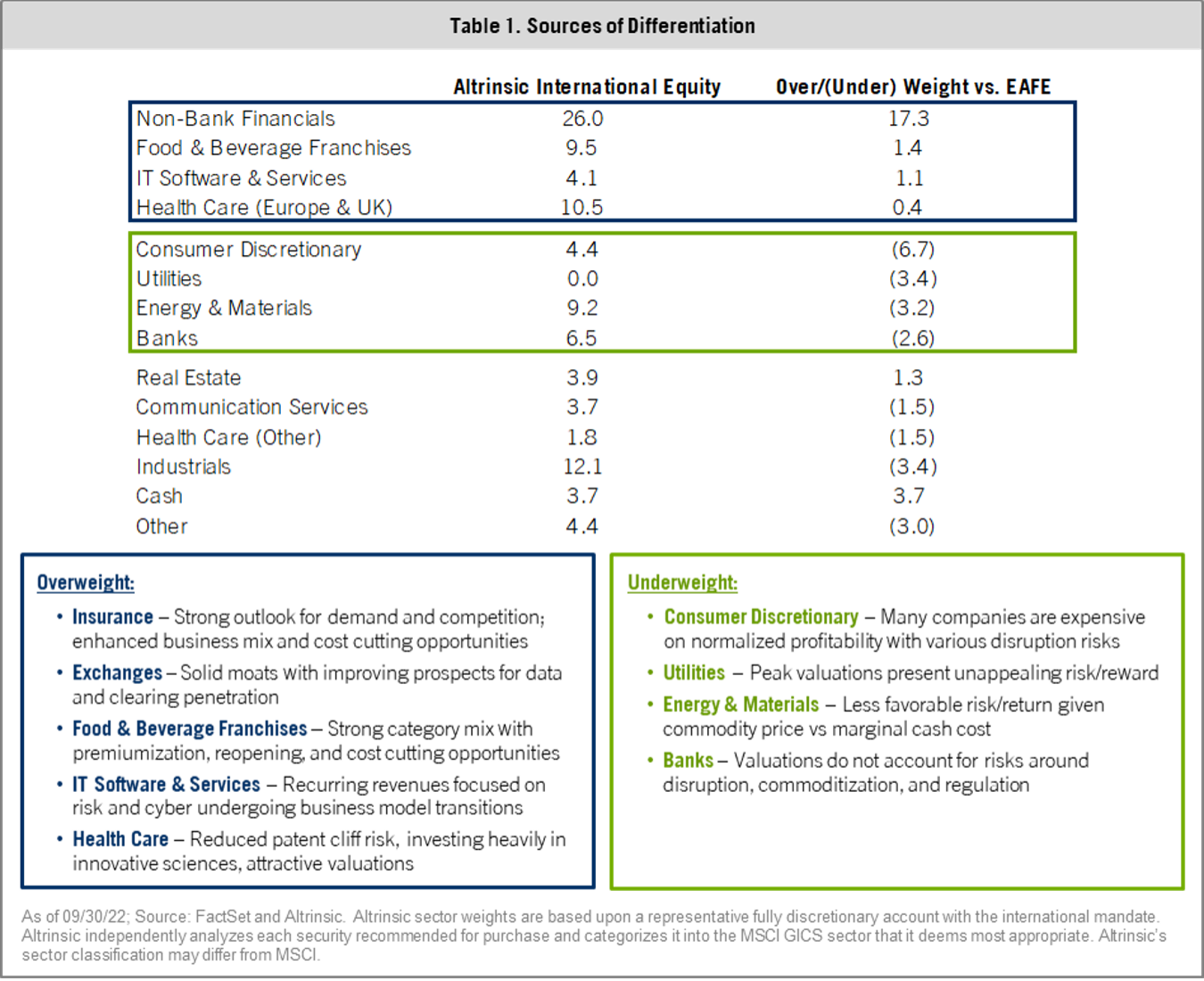

A summary of our portfolio risk exposures is illustrated in Table 1.

Performance Drivers

This was a challenging quarter, as performance tracked broad market indices. Negative attribution primarily came from traditionally defensive health care companies and those more exposed to China and Continental Europe, where macro concerns intensified. The greatest sources of positive attribution were investments in the financials, real estate, and consumer staples industries.

In the health care sector, two of our holdings (GSK and Sanofi) suffered, as the popular heartburn drug Zantac was allegedly linked to cancer if the drug was improperly stored or transported. While no scientific link between Zantac and cancer has been established, and the drug has had many owners since its introduction in the 1980s, the market diverted focus toward potential losses from inevitable litigation and away from the tangible progress both companies are making on their businesses. After the Haleon spin-off, GSK announced positive results for its respiratory syncytial virus (RSV) vaccine and now has one of the best growth profiles in the sector. Similarly, Sanofi is making significant strides in growing its attractive biologic Dupixent franchise alongside its profitable vaccine portfolio. We firmly believe there is a long path for innovation and value creation within health care, to the benefit of companies with well-managed R&D investments.

Ongoing macro concerns in Europe caused downward revisions for companies in several sectors, including communications (Liberty Global, Vodafone) and consumer discretionary (Continental). Companies with material exposure to China (Baidu, Alibaba Group, Adidas), where strict COVID-19 policies are severely affecting the country’s economic outlook and corporate valuations, also experienced pressure.

In contrast, companies expanding their market share (HDFC) and offering defensive cash flows as well as consistent margin execution (Daito Trust, Willis Towers Watson, Heineken, Diageo) contributed to positive portfolio performance.

Timeless Tenets

2022 has been a brutal reminder that excesses ultimately correct, valuation matters, and unexpected things happen all the time. Although it has become quite fashionable in the investment industry to espouse “high conviction” and “concentration,” we believe that the timeless tenets of humility, common sense, and appropriate diversification are more important than ever in these highly charged and uncertain times. As markets continue to transition, we will responsibly deploy capital in fundamentally strong businesses that we believe offer the most attractive long-term upside while considering downside risk, or margin of safety.

Thank you for your interest in Altrinsic.

Sincerely,

John Hock

John DeVita

Rich McCormick