Flying back from Japan, I found myself reflecting on the significant changes the country has undergone since my first visit fifteen years ago. Over that time, we have witnessed significant societal shifts, with political leaders taking steps to address demographic challenges by easing immigration barriers and boardrooms gradually embracing corporate governance reforms. This time, I was also struck by a meaningful cultural shift toward greater shareholder engagement. Business conditions remain challenging, as Japanese companies face mounting pressure from both Chinese competitors and nearshoring trends. Many companies are still clinging onto overly diversified portfolios and resisting change, but some are making the necessary strategic adjustments to drive long-term sustainable growth. Within this evolving landscape, we see emerging opportunities.

Shareholder-Friendly Changes Underway

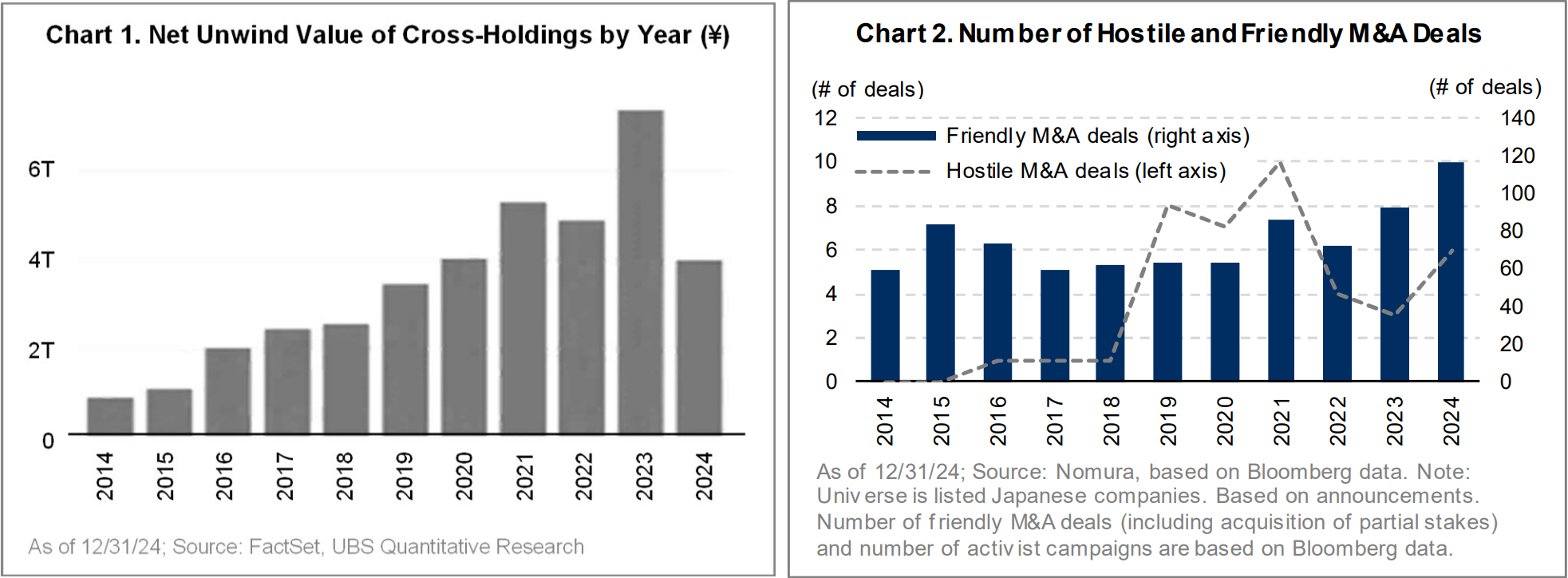

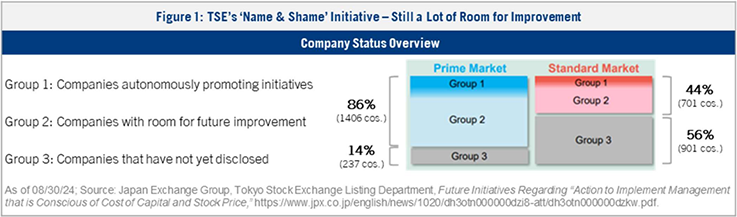

I visited with over 35 companies across the electronic components, industrial, and semiconductor sectors during a ten-day research trip. It was encouraging to see management teams displaying a heightened willingness to engage with shareholders in both subtle and significant ways. Impressively, about one-third of my meetings were conducted entirely in English, and even interactions at factories underscored the growing adoption of English as the language of business. Management teams are also responding to the Tokyo Stock Exchange’s (TSE) two-year-old “name and shame” initiative to improve capital efficiency and corporate governance practices of Japanese companies. This initiative has been instrumental in driving incremental improvements, as evidenced by several metrics, including the reduction of cross-shareholdings (Chart 1) and improving ROE in an increasing number of companies. Increased shareholder activism and M&A are also on the rise (Chart 2). However, there remains scope for further progress. TSE’s latest analysis puts a significant number of companies from both the ‘Prime’ and ‘Standard’ markets1 in Group 2 (‘Room for Future Improvement’) or Group 3 (‘Have Not Yet Disclosed’) (Figure 1).

Japan remains an outlier among developed markets with nearly 50% of listed companies holding net cash on their balance sheets (Chart 3). Furthermore, about 40% of Japanese companies in the TOPIX still trade below book value (Chart 4). Given the significant role shame plays in Japanese society, management teams and boards are highly motivated to keep making progress in order to avoid public scrutiny.

Industrials and Autos: Challenges and Opportunities

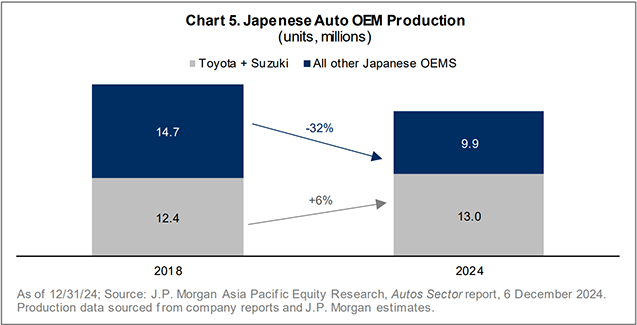

Beyond the TSE initiatives, structural challenges such as rising Chinese competition, nearshoring trends, and the threat of tariffs are forcing Japanese management teams to embrace change. Apart from the few companies riding the AI boom, Japan’s industrial base is facing considerable strain. The automotive sector, a crucial industrial vertical, is under significant pressure, as Chinese original equipment manufacturers (OEMs) rapidly gain share both domestically and internationally. Japanese OEMs produced 15% fewer vehicles in 2024 compared to 2018, with only Toyota and Suzuki showing modest (+6%) growth (Chart 5).

The rest of the players have seen production decline by 32%, and their transition to EVs remains slow. The global expansion of Chinese automakers, coupled with their increasing reliance on domestic supply chains, is posing a challenge to Japanese suppliers as Japanese OEMS lose market share. This challenge was highlighted in my meeting with THK, a linear guide manufacturer, as key customers like Nissan face mounting pressure in the evolving automotive landscape. Despite the uncertainty surrounding the ongoing Nissan-Honda merger discussions, we believe that eventual industry consolidation across OEMs and the entire supply chain is essential for survival. THK and other suppliers face constraints in adapting to industry shifts due to the strategic decisions of OEMs, which limit their autonomy. In contrast, Denso, an automotive parts manufacturer aligned with the industry leader Toyota, has greater flexibility to act and is forging ahead with restructuring efforts. During my discussions with them, Denso’s management noted its decision to divest its spark plug business to Niterra, the dominant spark plug manufacturer, as part of a mutually beneficial consolidation in a mature industry segment. We believe that Japan needs more of this type of collaboration within the auto industry.

The automotive sector also drives over half of the demand for factory automation and has become an increasingly important driver of semiconductor and electronic component demand. Cyclical and structural issues impacting the automobile end market have pressured the fundamentals of factory automation companies, resulting in significant multiple compression (Chart 6).

In my meetings with TDK and Taiyo Yuden, key Japanese manufacturers of multilayer ceramic capacitors, it became clear that there is significant overcapacity in the industry, along with mounting competition from Chinese and Korean manufacturers. SMC, a leading pneumatics components manufacturer, lost over 50% of its market share in China’s mid-to-low-end market over the last few years. Although we are not currently invested in this segment, we see emerging opportunities, as some of these companies possess meaningful intellectual property and are adapting to the changing landscape, offering pathways to generate improving shareholder value over the medium- to long-term. Despite the challenges noted above, we see opportunities in the Japanese market and have identified and invested in several companies that are largely insulated from key competitive pressures. My on-the-ground due diligence during this latest trip helped reinforce my beliefs about their many strengths:

- Suzuki Motor derives the majority of its profit from India and Japan, where it faces limited Chinese competition. Its strong market position in India remains underappreciated by investors. In India, its partner Maruti Suzuki commands a 41% overall market share but an extraordinary 72% share in the compressed natural gas (CNG) vehicle segment. The CNG segment, representing 20% of the passenger vehicle market, grew 35% in CY2024. Government support suggests continued growth in this segment, underpinning Suzuki’s long-term growth prospects.

- Yamaha Motors faces minimal Chinese competition in its motorcycle and marine businesses, which generate most of its profits. Management reaffirmed the company’s commitment to its strategy of driving profitability and pricing higher through premiumization. This disciplined approach sets Yamaha Motors’ management apart from other Japanese management teams we meet, many of which attempt to chase market share at the expense of profits.

- Sony is an example of a leading company that has succeeded by embracing reform. The company has demonstrated significant ROE improvement since initiating restructuring in 2014 (Chart 7). Sony’s management reaffirmed plans to IPO its financial division and consider further divestments, highlighting their ongoing commitment to strategic transformation.

Closing Remarks

As with prior visits, my recent trip to Japan offered valuable insights. Engagement with Japanese C-suite executives and senior management at manufacturing facilities revealed a significant cultural shift driven by nearshoring trends, intensifying competition from China, and the looming threat of tariffs. Although this shift is not uniform, clearly there are a growing number of management teams embracing change with a commitment to enhancing shareholder value. This left me convinced that Japan will increasingly be a source of compelling opportunities for global investors.