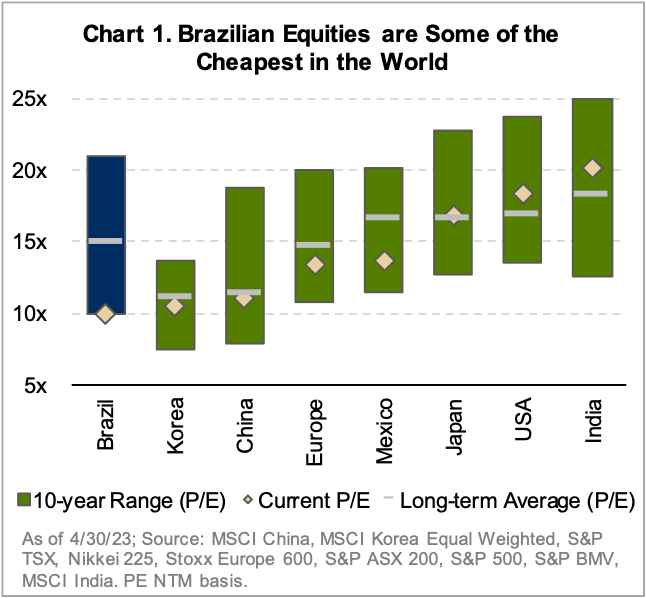

We spent two weeks in Brazil engaging with contacts in the technology, banking, retail, industrial, and materials value chains to strengthen our network and deepen our insights about the macro and micro factors at play. Political risks, volatile inflation, currency depreciation, and relatively high financial leverage have made Brazil a challenging investment environment for years. Over the past decade, Brazilian equities1 delivered a -16% total annualized return (USD); even in local currency, inflation-adjusted returns were just +17%. The return to power of a leftist president, anti-business rhetoric, and interest rates back at decade highs have turned many investors away altogether – resulting in some of the lowest valuations in the world (Chart 1). Our prior due diligence trips have coincided with plenty of bouts of economic malaise (Greece in 2010, Spain in 2011, Turkey in 2018). However, investor pessimism on the ground in Brazil was some of the most extreme we have seen over the past decade or so. Where there is extreme pessimism, there may also be value.

Quick Reflections

- Fiscal and monetary policy will hinder economic activity for an extended period: Memories of hyperinflation loom large, and central bankers are inclined to keep interest rates well above inflation for longer. Yet given that Brazil’s real interest rates are the highest in the world, there will be enormous opportunity when they do fall. On the political front, new leadership lacks congressional control to enact sweeping changes; our base case still must assume higher corporate taxation, partially offset by higher fiscal spending.

- Volatility is normal in Brazil, and many companies have adapted: Attitudes of corporate leaders in Brazil are reminiscent of past visits to Turkey, Thailand, and Indonesia, to name a few, where entrepreneurs are used to volatility. Many have built strong business models designed to withstand ups and downs.

- Higher-end consumers and large corporations are stronger than many realize: Low-income households and very small businesses are suffering under the weight of high leverage and, in many cases, falling real incomes. However, higher-end consumers and large corporations spent the last few years improving their balance sheets and are more resilient than the investment community gives them credit for. This presents company-specific opportunities as investors sell en masse.

- Equities present significant idiosyncratic opportunities: Brazilian equities are priced for much lower profits and a permanently higher cost of capital. With the highest real interest rates in the world and plenty of quality companies on sale, overall investor pessimism has led to opportunities for positive micro and macro surprises to emerge. We have recently acquired shares in Itau, a high quality and well capitalized bank trading near multi-decade lows on price-to-normalized earnings. In retail, some companies with strong operating models, good balance sheets, and sensible management teams are seeing their shares cut in half, providing an increasingly attractive risk/return skew.

Key Issues & Implications

1. The Interest Rate Backdrop

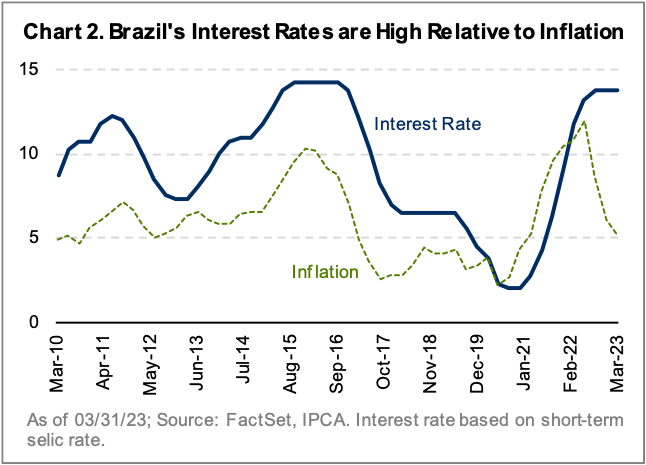

Brazil enjoyed low and stable inflation from early 2017 to late 2020 but quickly experienced a painful spike similar to other regions around the world. Given Brazil’s history with inflation (it ran at 3000% in the early 1990s), the central bank was quick to adjust, rapidly raising interest rates from 2% to nearly 14% in just 21 months (Chart 2). Those rate increases are now putting significant pressure on the economy (Chart 3).

Brazil’s real interest rates are far higher than most of the world, and we were hopeful that rates could drop quickly from here. But after two weeks on the ground, we now think central bankers are likely to keep rates higher for longer. Although inflation slowed to less than 5% in March (below Europe and the US), this trend needs to extend and go lower before central bankers cut rates significantly. Should the world enter a global recession, Brazil would have enormous monetary firepower—something many other countries cannot say.

Brazil’s financial leverage is far above many emerging market countries, but this does not tell the whole story. Many retail and banking executives say much of the excessive borrowing was among lower-end consumers and very small businesses. By our estimates, these segments increased their debt by at least 80% in the last three years alone. Higherend consumers and larger corporations are in much better shape, but even the latter signaled some reduction in investment spend.

Long-term investment opportunities in companies exposed to higher-end consumers and larger corporations are likely to emerge as the selloff of Brazilian equities continues. If inflation continues to decline, interest rates are likely to fall sharply, stimulating the economy and equity markets, and leading to a lower cost of capital, rising equity flows, and upward earnings revisions. It remains to be seen how much damage the economy will sustain in the short term, and whether Brazil will experience a negative feedback loop.

2. The Consumer

We sought to assess the state of the Brazilian consumer and investment opportunities in retail through meetings with retailers, mall operators, and banks—including specialized retail tours. While we received mixed messages, one

negative aspect that emerged is that many consumers have become overly reliant on credit to fund purchases, particularly those in the low-end retail segment. Based on company anecdotes and central bank research, our best guess is that half of purchases at many stores over the last two years were funded with credit,. As a result, many households are now struggling to keep up with payments, especially given borrowing rates are often 3-5x those of developed markets. Even high quality retailers like Lojas Renner have seen past due loans more than double over the last year (approaching 26% of total loans). We expect the cumulative effect will be a further softening of retail sales as the year progresses and low-end consumers are denied access to more credit card spending.

Whenever we visit Brazil, we are struck by the love for malls, which still dominate the shopping landscape. The reasons are multifaceted: cultural factors (preference for highly social and experiential shopping), ease of access (10 minute walks versus 30 minute drives in many US cities), security (lower crime risk compared to shopping on the street), and infrastructure challenges (slower and costlier logistics related to online shopping compared to developed markets). During this recent trip, the malls were fairly busy, particularly those catering to middle-to-high income consumers. The CEO of one such mall operator mentioned that their clients’ sales were up 20% year-over-year in March alone. Although e-commerce has gained ground in Brazil, its penetration rate is still below the global average of 20%, currently standing at less than 10%. This rate has nearly doubled over the past five years, driven in part by foreign players that have managed to avoid import taxes and greatly undercut local players on price. Our discussions suggest that the government is finally starting to address this issue as it aims to improve its fiscal position, which could significantly benefit brick-and-mortar retailers.

The talk of the town in retail was Lojas Americanas, the 3G Capital-backed chain that recently defaulted on US$8 billion in debt after struggling with weakening sales and allegedly fraudulent supply-chain financing. The collapse of Americanas appears to have spooked investors across the retail sector despite the fact that balance sheet structures vary widely. While many retailers are indeed struggling due to high leverage, high interest rates, slowing sales, and tighter financing, this situation is also creating significant opportunities for those with robust balance sheets and a skew toward higher-income consumers.

3. The Consistent Theme of Political Volatility

The general sentiment among most business people we met in Brazil is that President Lula’s return to power poses a significant challenge for the country’s economy and investors. Brazil blossomed under his leadership from 2003 to 2010, but Lula’s stewardship of the economy benefited from growing commodity demand and higher leverage. After leaving office, Lula spent nearly two years in prison on corruption charges that were later annulled, and narrowly won re-election in late 2022. What was clear from our meetings is that Lula has ambitious fiscal spending plans but lacks sufficient tax revenue to fund them. As a result, tax increases on corporate profits and dividends, and higher value added taxes, are likely. Surprisingly, we found more support for these tax hikes than we initially expected, largely because of the need to simplify Brazil’s complex and frequently evaded tax system.

On a positive note, while Lula’s rhetoric is often anti-business or anti-capitalist, those more involved in the political sphere emphasized that Lula’s weak influence in Congress would make it difficult for him to enact any extreme measures, which is a nuance that seems overlooked by international investors. Either way, negative headlines are here to stay in the near-term. For the banks, we estimate the potential impact of a new tax regime to be a 10% drop in profits, but the question remains as to how much they will recover through increased fees and lending spreads.

4. Bank Risk Meets Valuation Opportunity

Banks are clearly facing significant pressure from the economic and political environment in Brazil. Tax rates will go up, credit losses will temporarily rise, and lending demand will slow. But in all of our interactions, we were pleased to see an increasingly disciplined competitive backdrop. Six banks control 75% of Brazil’s lending, and none seem willing to make more aggressive competitive decisions. Even state-owned banks are far more focused on profitability than in the past and have recently pushed back on any government initiatives aimed at promoting aggressive competition. In addition, while fintech has taken market share over the years, these companies are facing sharply rising credit losses due to aggressive lending practices, and fintech investors are now demanding a greater focus on profits rather than growth. This competitive backdrop should help keep elements of banking profitability stable while the industry navigates through a difficult economic period.

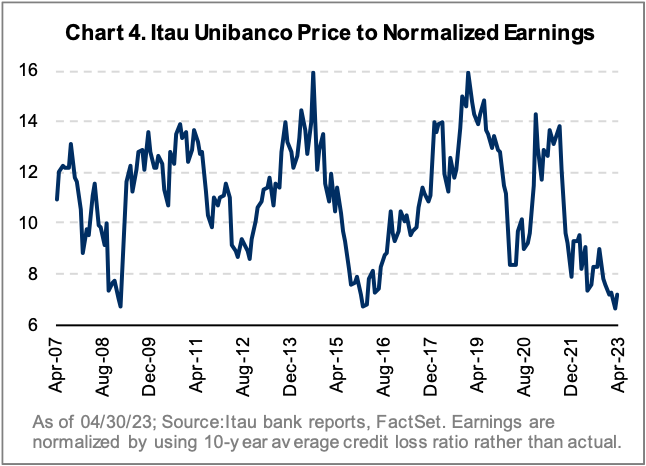

Current valuations are reflecting a highly pessimistic economic outlook, evident in even the highest quality banks including Itau Unibanco, which is trading near alltime lows on price-to-normalized earnings (Chart 4). Given Itau’s strong capital position and profitability, it would need to see a substantial 17% loss on its loan book before requiring an equity raise, making it a particularly compelling investment opportunity in our view.

5. Investment Implications

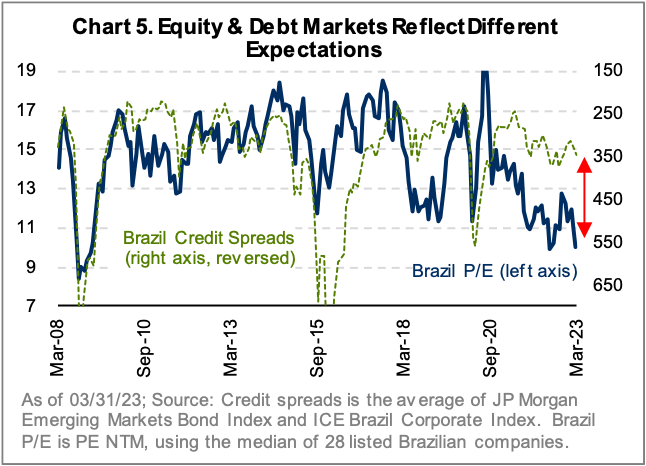

Brazilian equities are presently trading near all-time lows on price-to-earnings. Interestingly, the fixed income markets paint a more optimistic picture, with credit spreads in line with long-term averages (Chart 5). This divergence between equity and debt markets is the largest since the Global Financial Crisis. While this deviation may be partly due to investors pricing in a higher cost of equity in a higher rate environment, it is still noteworthy.

The companies that we find most attractive are those with strong balance sheets, capable management teams, exposure to high-income segments of the economy, structural growth opportunities, and discounted valuations. Currently, we are invested in two Brazilian stocks. The first is Itau Unibanco, a leading private bank that caters to highend households and large corporations, and trades near alltime lows on price-to-normalized earnings despite its strong capital and risk management. The second is Lojas Renner, a top apparel retailer with a renowned brand, a net cash balance, superior operational capabilities, and opportunities to expand its e-commerce offering. Despite these strengths, the stock is trading near its all-time low valuation.

We are currently conducting more due diligence in the food retail, investment banking, and health care sectors, as we believe investment opportunities could emerge in these areas in the near future. Risks run high in Brazil, but as valuations adjust lower, we believe that the current environment presents attractive prospects for investors with a long-term time horizon. As always, we will maintain our conservative and disciplined investment approach.