WE CONTINUE TO VIEW THE ASEAN REGION AS ONE OF THE BEST SOURCES OF INVESTMENT OPPORTUNITY, PRESENTING A UNIQUE COMBINATION OF ATTRACTIVE VALUATIONS, RECOVERY POTENTIAL, AND SUSTAINABLE LONG-TERM GROWTH. WITHIN THE REGION, AND CONSIDERING BOTH SHORT- AND LONG-TERM POTENTIAL, WE BELIEVE VIETNAM IS ONE OF THE MOST PROMISING INVESTMENT PLAYS, UNFOLDING IN FIVE ACTS.

1. OPENING ACT: ATTRACTIVE DEMOGRAPHICS

Vietnam is large, young, and prepared. With a population of 97 million, Vietnam is one of the world’s most populous countries. Beyond the aggregate number, and more exciting from an investment perspective, is the fact that its population is young and vibrant. The average age in Vietnam is 32.5 years, comparing very favorably to the more established emerging economies of North Asia – namely China and South Korea – where the average ages are 38.7 and 43.4, respectively (Chart 1).

The Vietnamese are not just young and numerous, but also highly literate. The adult literacy rate in Vietnam (95%) is among the highest in key emerging countries (Chart 2). The combination of a favorable demographic profile and high literacy rate should contribute to attractive, sustainable economic growth for years to come. A rarity in many key emerging countries, these dynamics warrant real consideration.

2. SECOND ACT: STRONG ECONOMIC OUTLOOK

Vietnam is poised to deliver one of the fastest economic growth rates in both the short- and medium-term. Impressively, since the COVID-19 outbreak, Vietnam has been one of the few economies worldwide that has continued to grow every year. As economies continue to re-open, Vietnam is expected to deliver leading global growth levels in the 6-8% range (Chart 3). Further, while the pandemic has slowed key drivers like trade and investment, we expect these dynamics to resume their secular growth patterns and prove sustainable into the future, underpinning consumption.

Trade: On January 1, 2022, the world’s largest free trade agreement (FTA) – the Regional Comprehensive Economic Partnership (RCEP) – took effect, and ASEAN nations including Vietnam stand to be some of the greatest beneficiaries. The key benefits of this FTA include large reductions in regional tariffs, lower trade barriers, and easier capital flows, strengthening current accounts and reducing currency volatility.

Domestic Investments: The Vietnamese government remains committed to a 6.5-7% GDP growth target through 2025. In support of this commitment, lawmakers are focused on infrastructure projects that will improve logistics, efficiency, and productivity as well as tax incentives that could lead to a reduction in value-added tax (VAT) rates, lifting purchasing power, profitability, and business confidence.

Foreign Direct Investment (FDI): FDI has been a key driver of Vietnam’s healthy current account balances and its economic momentum; in fact, the country reports the highest FDI/GDP ratio within the ASEAN region at approximately 6% (Chart 4) and experienced consistent FDI inflows during the pandemic period. Continued strong economic growth and improving trade prospects suggest that sustained FDI sits on solid footing in the years ahead. One key driver behind FDI has been a shift in the Asian supply chain from North Asia (China, Korea, and Taiwan) to a more competitive Vietnam. Although incomes are rising modestly, Vietnam remains very attractive relative to the rest of the ASEAN region from a cost perspective. Lower relative wages (Chart 5) and manufacturing costs, complemented by a series of free trade agreements, are an attractive combination for foreign investors.

3. THIRD ACT: RISING INCOMES, RISING DIGITIZATION, RISING CONSUMPTION

Vietnamese consumption is on a structural upswing due to rising wages. Additionally, urbanization has significant runway, as Vietnam’s General Statistics Office reports that only 37% of the population was distributed in urban areas as of 2019, up from just over 20% in 20051. Migration to cities – likely an attractive opportunity for the predominantly young and educated population – leads to higher average income levels (Chart 6) and elevated consumption patterns.

Beyond the direct and more rudimentary relationships between urbanization, incomes, and consumption, the pandemic period provided great insight into digitization trends in Vietnam and the rise of e-commerce-based consumption. Smartphone penetration in Vietnam is high (65%), and e-commerce revenues increased 31% last year, with expectations that this segment will continue to grow at a 29% CAGR through at least 2025 (Chart 7). We expect further inflows from foreign and domestic investors into Vietnam’s digitization journey – especially given that the country is viewed as a vibrant innovation hub in the ASEAN region, housing many incubators, accelerators, and innovation labs – which will continue to promote increased consumption.

4. FOURTH ACT: A BENIGN POLITICAL BACKDROP (BUT CHINA REPRESENTS A WILDCARD)

The current political backdrop in Vietnam is rather benign and presents a lower level of risk than other leading emerging markets countries. Incumbent general secretary Nguyen Phu Trong secured an unprecedented third term during the early 2021 election cycle, and the next National Congress elections will not occur until 2026. With political instability being a significant consideration when investing in emerging markets companies, we are encouraged by what we see in Vietnam today.

However, trade agreements and the geopolitical relationship with China are key drivers for Vietnam, which introduces a degree of risk given the uncertainty surrounding Chinese government policies and regulations. While the RCEP agreement is important for Vietnam’s trade relations with many countries, China represents 25% of Vietnam’s total trade volume (net exports) (Chart 8), dominated by machinery, textiles, and footwear materials. This is something that we will be watching closely due to the overall unpredictability of China’s actions – but given that a large part of the trade with China reflects the interconnected global supply chain, we believe there are strong incentives for both neighbors to maintain favorable relationships.

5. FIFTH ACT: IMPROVING CONDITIONS FOR EM AND GLOBAL INVESTORS

With macro conditions trending favorably for Vietnam, a collection of key technical elements is the lynchpin that will enable greater investment participation by a broad set of long-term oriented investors – both those dedicated to emerging/frontier markets and truly global investors.

Improving Liquidity: Greater recognition by investors around the globe has contributed to increasing flows in Vietnam. Liquidity surged more than four times over the past two years to an average of USD 1.3 billion as of March 31, 2022 (Chart 9). While domestic retail investors are an important driver, the number of foreign trading accounts has also increased by 40% over the last three years and over two-fold since 2016 (Chart 10).

Regulatory Tailwinds: A relaxation of intraday trading is expected to materialize sometime in 2022 or 2023, thereby making the Vietnamese market a more attractive capital destination. Additionally, foreign ownership limits (FOL) are expected to rise across several sectors, including commercial banks.

Law of Enterprises: The ongoing parliamentary review of the Law of Enterprises2 could result in positive outcomes for foreign investors in the form of access to NVDRs (non-voting depository receipts, a commonly used share structure for international investors in the region), better minority shareholder protections, and a revised definition of what is considered a state-owned enterprise (SOE). This should lead to a high potential for government capital divestment and more capacity for foreign investors.

Upgrade to EM Status: Several ongoing reviews suggest that Vietnam will receive a status upgrade across different entities over the next 12-24 months. FTSE Russell is expected to upgrade Vietnam to EM status (from frontier status) sometime between late 2022 and September 2023, and MSCI is expected to follow suit by mid2024. Importantly, this upgrade is a government policy goal and, therefore, a key area of focus for legislators; in fact, the States Securities Commission of Vietnam is targeting to achieve MSCI EM status before 2024.

THE FINE PRINT

Although we are enthusiastic about how this play is coming together, there are several technical details to consider – namely, potential risks associated with COVID-19, currency performance, political friction, and geopolitical skirmishes.

- COVID-19 Risks: The pandemic continues to present economic risks, particularly in EM countries. That said, vaccination progress has proven superior to our initial expectations, and to-date the country has avoided a zeroCOVID type policy, allowing for frequent testing and maintaining higher levels of capacity utilization in key industries. Signals point toward a continuation of these trends, but we know the pandemic brings unpredictability, so we will continue to monitor closely.

- Currency Risks: Currency performance has been eerily quiet over the past decade, but we retain memories of prior periods of high volatility when the currency devalued multiple times in a decade. While mindful of the risk, the banking system appears more robust relative to the past, and the State Bank of Vietnam has a more focused approach relative to rising US Federal Reserve rates, so we are cautiously optimistic about the future. A positive real interest rate differential and manageable inflation pressures provide headroom for central bank policy decisions.

- Political Risks: Although the next Congress election is not until 2026, a central one-party system run by a leadership group almost twice as old as the median citizen may generate some intra-period friction. That said, political risk feels lower in Vietnam relative to other emerging countries.

- Geopolitical Risks: Vietnam’s proximity to China and the South China Sea presents plenty of opportunity for conflict. To-date, skirmishes have arisen in the South China Sea rather than at its land border with China, but it is impossible to predict what the future might hold. We will continue to monitor any apparent escalation in geopolitical tension in the region.

DÉNOUEMENT: WHY VIETNAM, WHY NOW?

As we look across the emerging and frontier universe, Vietnam’s five-act play presents a strong case for investment in the country. A large, young, and literate population will support the continued economic recovery. Trade will be a source of momentum, supported by domestic investments and structural, sustainable FDIs alike. A confluence of factors will promote higher levels of consumption, and a series of market structure and policy-related shifts would make it easier for foreign investors to deploy capital in Vietnam. While risks are ever-present, we believe Vietnam’s risk profile is quite manageable compared to other large emerging markets.

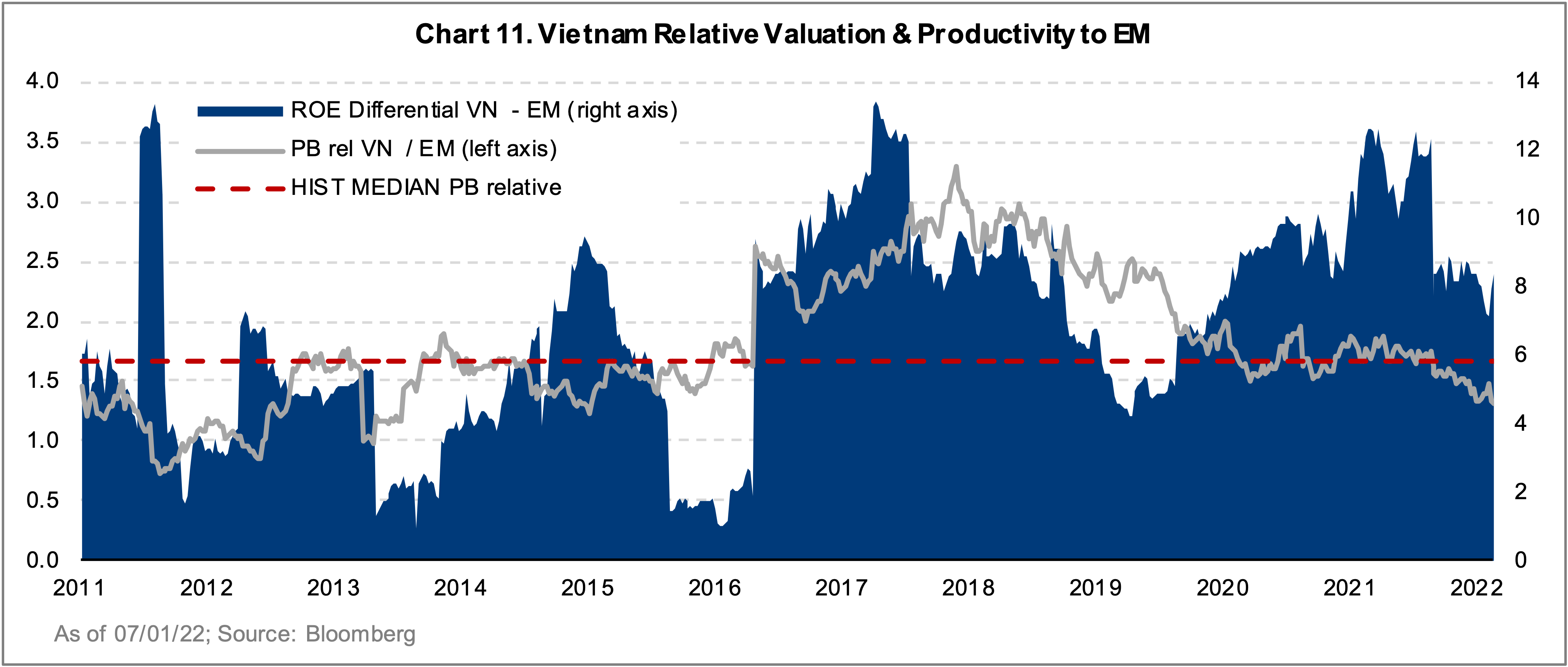

Underpinning the positive forces and positioning highlighted above, we also find tremendous support from a bottomup valuation perspective. Vietnam offers one of the highest (and most sustainable) growth prospects in the EM region and within the ASEAN Tiger Cubs, specifically. Valuation is quite attractive relative to growth, level of returns achieved, history, and the rest of the emerging markets opportunity set. A recent government crackdown on misconduct in both property markets and the stock market has led to a de-rating of the Vietnamese market. Despite a stronger structural position today, including sustainable growth prospects, relative to the last decade, Vietnam is currently trading lower than its historical median level (Chart 11).

Although Vietnam has yet to reach EM status, we believe it harbors quintessential consumption and growth characteristics supporting an array of investment opportunities not seen in other markets. The Altrinsic Emerging Markets Opportunities portfolio includes investments in three Vietnamese companies (representing 4.5% of the portfolio and adding differentiated frontier exposure)3 , and we continue to search for additional opportunities in the region. We are looking forward to seeing this five-act play hit the main stage!

About Altrinsic Global Advisors, LLC

Altrinsic Global Advisors, LLC, founded in 2000, is an employee-controlled and majority-owned investment management firm. Altrinsic manages approximately US$8.6 billion3 in global and international equities, applying a long-term private equity approach to public equities. Altrinsic’s clients include corporate and public pension plans, endowments, foundations, sovereign wealth and sub-advisory clients. For more information, please visit www.altrinsic.com or contact Sara Sikes at +1 (203) 661-0030.