With 280 million people, a median age under 30, and commodity reserves critical to the global green transition, Indonesia is a cornerstone of ASEAN growth and one of the most consequential emerging markets of the next decade.

River He and I recently spent four days on the ground, and our due diligence included company meetings across the financials, telecom, and consumer sectors; asset and infrastructure site visits; and direct conversations with policymakers, including individuals at Bank Indonesia and sovereign wealth fund Danantara. Within hours of arrival, the country was facing an unexpected policy shock driven by mining law changes and a surprise rate hike. What better time for a round of on-the-ground experiences and firsthand conversations? While modest on an absolute basis, Indonesia represents a noteworthy overweight in our portfolio1; trips like this allow us to see beneath the headlines and uncover what the market might be missing.

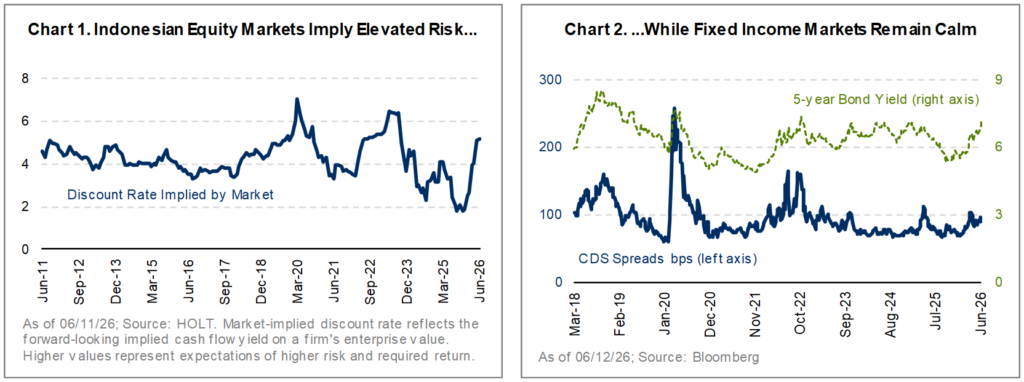

When Equity Markets Price in Crisis…and Credit Markets Do Not…

A notable divergence in Indonesian markets caught our attention before our plane touched down in Jakarta. Equity market-implied discount rates climbed toward 15-year peaks (Chart 1), pricing in risks that credit markets did not corroborate (Chart 2). Bond yields sat near long-run medians; 5-year credit default swap spreads were running 20% below median; and inflation continues to hover near two-decade lows. That type of dislocation, in our experience, is worth investigating. We discovered that policymakers across government institutions, regulatory bodies, and the central bank are still working to rebuild credibility, but the trip reinforced for us that the structural story holds.

View From the Ground: Macro Discipline, Tentative Recovery, and Infrastructure Ahead of Schedule

View From the Ground: Macro Discipline, Tentative Recovery, and Infrastructure Ahead of Schedule

1. Macro: Policy Direction is Right, Execution Remains the Test

What stood out during our conversations at Bank Indonesia (“BI”) was a deliberate shift in focus toward currency stability and fiscal discipline (1% inflation band through 2027). FX reserves have declined as BI defends the rupiah but remain well above international benchmarks. A central bank willing to spend reserves and hike rates simultaneously sends a clear signal in support of repairing macro credibility.

Meanwhile, Danantara2 is working through some complexities (and internal conflicts of interest) in terms of the multiple roles it plays: commercial investor, policy arm, and stabilization vehicle. We think their current playbook makes sense, including simplifying the SOE structure, linking KPIs to ROE, and rebuilding credibility through execution. But communication has been its self-acknowledged weakness, as policy details changed frequently and were poorly signaled. That execution gap, not the strategy, has amplified market anxiety beyond fundamentals.

Indonesian financials offer an attractive return profile in a market where credit penetration remains low by global standards. Leading private banks in Indonesia boast some of the strongest low-cost deposit franchises we encounter globally, sustaining ROE above 20%, even under stress. The key risks appear identifiable and, in our view, are being appropriately stress-tested. Our direct macro exposure to Indonesia is through Bank Mandiri, the country’s largest SOE bank. It is policy-adjacent, balance-sheet capable, and a beneficiary of improving sovereign credibility.

2. Consumer: Recovery is Real, but Fragile

Over the last 12-18 months, Indonesia’s consumer backdrop has been partially shaped by weak labor market confidence and persistent food price pressures. Government spending has lifted consumer sentiment, though sustainability is uncertain as the fiscal base normalizes from 4Q25. Currency depreciation is the dominant management concern, impacting pricing, procurement, and capex. So far, fuel subsidies have largely insulated companies from energy cost pressures. Structural labor cost advantages support near-term competitiveness but may constrain medium-term productivity.

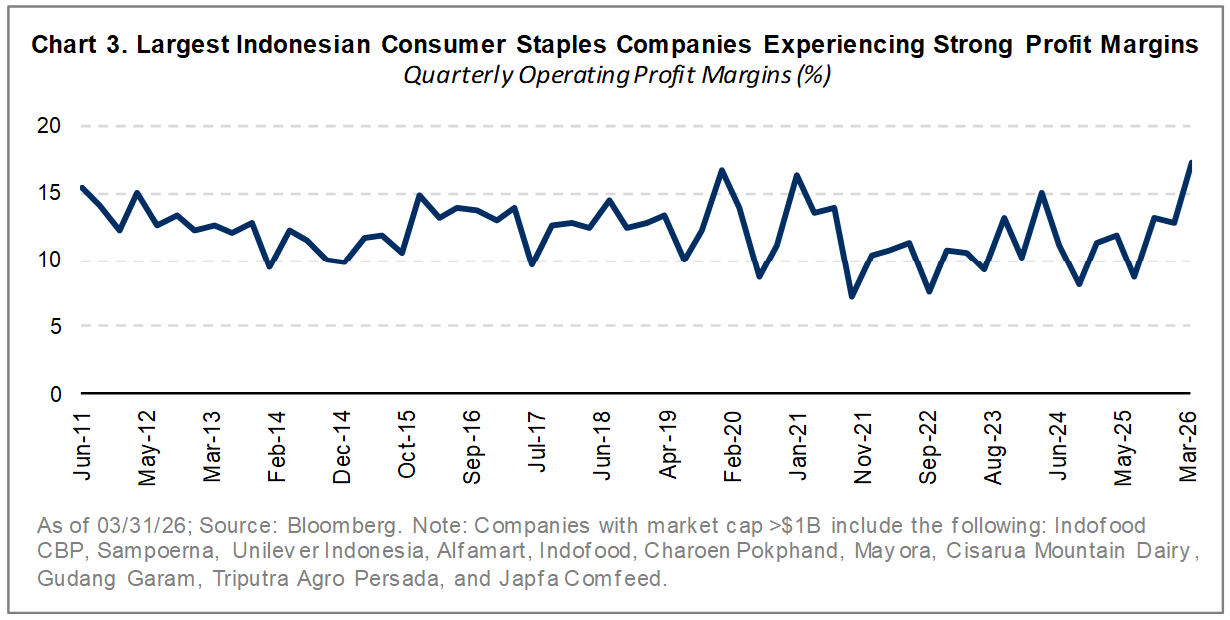

One of our portfolio holdings, PT Sumber Alfaria Trijaya (known as Alfamart), offers direct exposure to Indonesia’s consumption recovery (Chart 3). Our visit to their distribution center reinforced the retailer’s scale, logistics discipline, and service reliability, all of which are difficult for smaller competitors to replicate. Deferring USD-linked capex amid rupiah weakness signals capital discipline consistent with quality.

3. Tech: AI Enablers are Being Built Now

NeutraDC Cikarang, PT Telkom’s flagship hyperscale campus, sits within a large, newly developed industrial park alongside other major Asian e-commerce and industrial operators. Our visit there reinforced our view that Indonesia’s AI data center buildout is farther along than markets appreciate. Phase 1 is already operational, and while modest in terms of capacity, the facilities are state-of-the-art; Phase 2 targets 100 MW by 2027 and triple that capacity by 2030, with next-generation cooling and NVIDIA-chip clients. Telkom’s SOE-level power agreement with the national grid operator is a structural moat that no private competitor can easily replicate. Across the ASEAN region, we believe compelling access to the AI opportunity sits with the infrastructure enablers; PT Telkom is positioning itself to be one of the major gateways for AI adoption in Indonesia.

The Quiet Rewiring of EM Trade

Beyond the dynamics at play within Indonesia, renminbi (RMB) internationalization3 is quietly reshaping EM supply chains, and we believe the investment implications are underpriced. Several Indonesian companies have shifted close to 20% of procurement to RMB4 contracts, with direct sourcing in China. According to several conversations with Chinese banking executives in Hong Kong, where we stopped after Indonesia, this contracting shift is deliberate and systemic across the ASEAN region. In fact, collectively, ASEAN countries are now China’s largest trading partner. As regional trade bypasses the US dollar, EM corporates with diversified currency exposure should prove less fragile in episodes of dollar strength or capital flight. This is a perfect example of the decoupling story in practice.

Closing Remarks: A Contrarian Perspective

Policy uncertainty and the threat of MSCI downgrading Indonesia to frontier status have weighed heavily on foreign flows. The risks are certainly real: a fiscal deficit testing an established ceiling, fuel subsidies ballooning as oil prices remain elevated, and mining policy changes that keep resurfacing, to name a few. However, none of these risks is hidden, which means they can be fairly considered and valued when assessing the opportunity set.

Our current exposure5 spans three investments – Bank Mandiri, Alfamart, PT Telkom; and the trip surfaced additional opportunities that we believe could be worth pursuing. At about 9x forward earnings and with a dividend yield above 8%, Indonesia trades at a discount to the broader EM landscape (MSCI EM 12x forward earnings, sub-3% yield).6

The combination of well-understood risks, compressed multiples, and a yield exceeding sovereign spread risk often forms the foundation of an attractive, if contrarian, entry point, provided the earnings base holds. What is harder to model is on-the-ground conviction. Our clearest signal did not come from a boardroom or a policymaker. Instead, it came from Ghozzy, a hospitality graduate in Jakarta who saving up money to open a restaurant on his home island of Sumatra. Young, entrepreneurial, unfazed by the macro noise – that is the real Indonesia beneath the headlines. That willingness to commit and invest in one’s own country, which seems fairly prominent among the generation that will compound the next decade of growth, does not appear directly in any discount rate. But in our experience, it tends to carry weight – particularly at historic inflection points.

Epilogue

When it’s convenient, it’s a principle. When it’s inconvenient, it’s a technicality.

– Modern maxim inspired by philosopher Bertrand Russell

As we go to print, one poignant observation: when SpaceX debuted on the Nasdaq on June 12, it was the largest IPO in history, valued at roughly 92x trailing revenues (not earnings) from a company losing nearly $5 billion per year. To accommodate it, Nasdaq scrapped its longstanding 10% minimum free float requirement entirely.

Meanwhile, MSCI threatened to downgrade Indonesia, which trades at 13x earnings (not revenues), from emerging to frontier market status, in part because many listed companies had free floats as low as 7.5%. While Nasdaq rewrote its rules for a loss-making company, MSCI threatened to penalize a profitable market, even as Indonesia committed to a much higher float level. The contrast speaks for itself, and we think it speaks loudly.

*******************

Behind the Scenes

A few photos from the road!

[right] Behind the Racks: Alice and River toured PT Telkom’s new state-of-the-art data center, 40km from Jakarta.