Dear Investor,

Our three-year anniversary led us to reflect on what has changed in equity markets since April 2021 and, importantly, where we might be headed (a detailed Three Years in Review is included on page 6). The technology sector continues to make headlines across global markets, contributing 2.3% of the MSCI EM Index’s 2.4% return (in USD) in the first quarter. Not a dinner or meeting seems to pass without mention of the most dominant trend du jour – artificial intelligence. We agree with consensus that tectonic shifts are underway, and a broad range of industries – from financials to health care to industrials – will see substantial benefits. But we also believe that an important element of how this will all unfold, and the breadth of companies poised to benefit, is widely underappreciated.

Perspectives

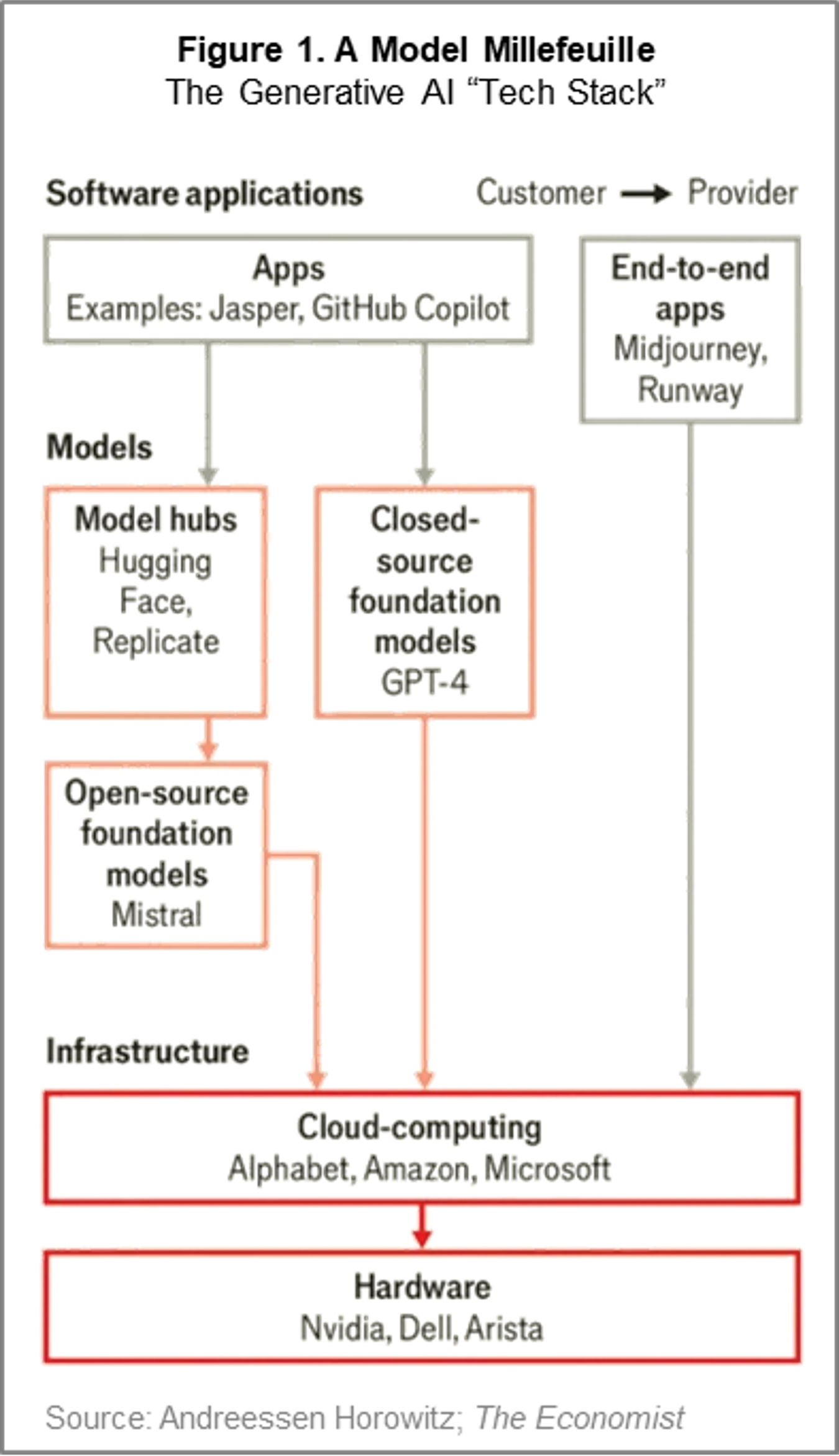

The infographic on the right (Figure 1) shows the categorization and relationships among many of the popular, sexy, high-tech areas of focus – from cloud computing to open-source foundation models to model hubs and more. A great deal has been written in the media about this software-focused “upper tech stack” of generative AI. But, for any of this to matter, what must come first?

The Underground Stack

“In a technology boom: the underlying physical infrastructure needs to be built first in order for software to be offered.”¹

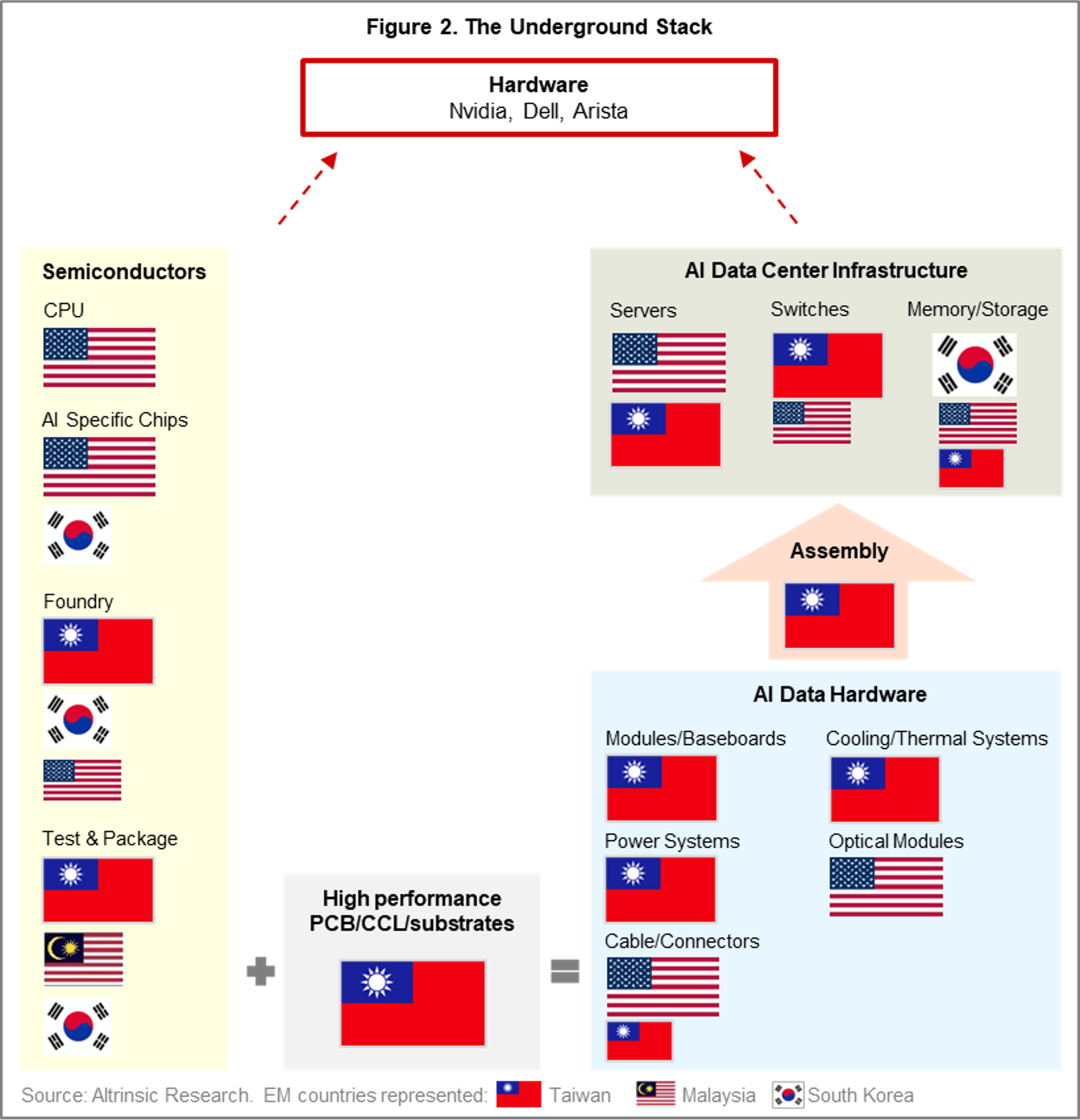

To the casual observer, this “underlying physical infrastructure” might evoke thoughts of the large US tech stocks, which are some of the most expensive across global markets. What is often overlooked is that these large players, including NVIDIA, rely heavily upon emerging markets for their success and execution, obtaining critical components from the supply chain embedded across a myriad of EM countries (Figure 2).

Underneath the surface, other technology players – including many EM companies – are making a substantial impact within this foundational ecosystem. EM companies develop critical underlying physical infrastructure that serves as building blocks for the AI tech stack; we refer to it as the “underground AI stack” (Figure 2). This group of companies is broad and diversified; many are now benefitting from new growth drivers and strong competitive moats linked to the advent of AI.

From chip fabrication at Samsung to server assembly at Hon Hai, the Asian region remains the strategic hardware enabler for global AI infrastructure. Altrinsic’s investment philosophy has always centered on finding companies with demonstrated track records of sound capital allocation that are undervalued. With that in mind, we have identified several companies playing critical roles in the underground stack that have been flying under the radar.

- Chroma ATE is a global leader in power testers. These devices are used to test power in a variety of electronic systems, including those used in EVs/battery cells, handsets, semiconductors, and AI systems.

- Delta Electronics is the global leader in power management systems for servers, data centers, consumer electronics, and EVs. AI infrastructure places a significant burden on data center power needs.

- Tripod Technologies is a manufacturer of printed circuit boards, a low-growth and highly fragmented industry. Tripod has prudently diversified its capacity to serve a wide array of customers, including those in the server/networking and memory industries, which support AI infrastructure.

Not only does AI-related revenue provide growth opportunities for these companies, but also the AI business comes at a much higher margin; average selling prices are often double those of non-AI products. With that said, all three companies also serve a much broader array of end markets than their specialized corners of the AI supply chain. In fact, as an independent growth driver, AI is often less than 20% of the companies’ revenues. This business mix balance allows for capitalizing on the upward AI-driven swing while also ensuring operational sustainability should volatility or challenges hit the AI infrastructure segment.

AI Opportunities…Beyond Tech

Despite the opportunities that now exist for EM technology companies to capitalize on the growing prevalence of AI, market concentration in the sector is high, and embedded discount rates reflect expensive valuations (Chart 1). At the same time, financial productivity levels remain below 30-year averages (Chart 2). This combination has created a challenging hunting ground for us and has led to an underweight exposure to technology (17.6%) relative to the MSCI EM Index (22%). From a targeted, bottom-up perspective, we continue to find unique undervalued opportunities and remain excited about our holdings, but on an overall basis, we are finding a wider array of attractively valued beneficiaries of the AI trend in sectors outside tech.

As a business driver, we see opportunities for some of our other portfolio companies to commercialize and/or capitalize on elements of AI enablement. Reliance Industries, an Indian conglomerate, is on a path to become a key supporter of India’s digital ecosystem by using AI to better service and address customer needs, particularly in the field of e-commerce. PT Telkom, an Indonesian state-owned telecom operator, is using AI to manage data center demand.

As a productivity booster, AI can reduce software development costs. Our holdings NetEase and Tencent are using AI to enhance productivity within their operations. For example, NetEase is using AI to reduce time-tomarket for new game development.

As an operations enhancer, AI can be used to optimize cost management practices and make smarter (and faster) business decisions. During our recent trip to South Africa, we observed several instances of AI being used in ways that make standard developed markets practices look quite outdated. In the retail sector, AI is used to control operating costs (electricity, energy) in pharmacies (Clicks) or to identify popular trends in apparel fashion and adjust supply chain and working capital responses more rapidly (Mr. Price).

Retail = Risk

Like many, we are excited about the AI-driven expansion of addressable markets for many of our holdings. However, the strong market momentum and stock performance seen in certain countries, including India, South Korea, and Taiwan, have been largely driven by retail investors, which presents some risks. Retail investors tend to be fickle and short-term-oriented; therefore, appreciating stock prices may not prove sustainable. In last quarter’s commentary, we presented an assessment of the elevated (and therefore, less attractive) valuations in India. In South Korea, while recent market performance has been driven by seemingly friendlier shareholder policies through the Corporate Value-Up² Program, local elections and intense political debates will likely induce higher volatility in this retail-driven market. But what about Taiwan?

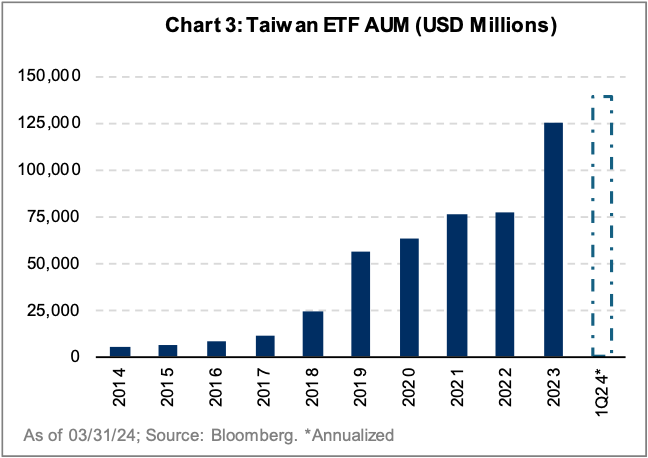

Taiwan might be the most retail-driven of the group. It is now the third largest ETF market in Asia-Pacific (behind Japan and China), and in 2023, Taiwan’s ETF AUM increased 70% (Chart 3), with 80% of that increase driven by the retail market. A recent article highlighted that retail investors are “taking out reverse mortgages to buy ETFs.”³ It is also a very concentrated market, with over 64% of capitalization exposed to the information technology sector.

Furthermore, one stock alone – wildly popular TSMC – represents 35% of the market.4 The investor buying behavior and market concentration in Taiwan is more reminiscent of frontier markets (think: Kenya) than a market waiting in line for a DM status upgrade. The last piece of this (unstable) puzzle is liquidity. The average liquidity of stocks outside the top 10 is 20x less than those in the concentrated top 10. For the roughly 1000 Taiwanese stocks included in the index, the median six-month daily value traded is a meager $1.2 million (USD). What happens when the market sneezes?

Performance and Investment Activity

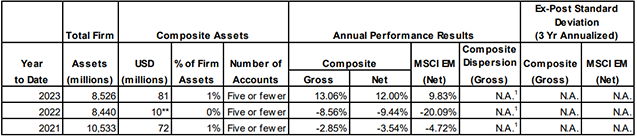

The Altrinsic Emerging Markets Opportunities portfolio declined 1.2% gross of fees (-1.4% net) in the first quarter, compared to the 2.4% increase of the MSCI Emerging Markets Index, as measured in US dollars.i Investments in IT (Parade Technologies), financials (Commercial International Bank of Egypt, AIA Group, Branco Bradesco), and consumer discretionary (Minth, Topsports) weighed on relative performance. Our underweight exposure to technology also detracted from relative performance. In financials, both weaker underlying results and currency depreciation impacted stock performance. In consumer discretionary, the operating environment remained weak for some of our Chinese companies. Key positive contributors were individual stocks in industrials (Yutong Bus Co, Larsen & Toubro, Airtac), energy (Petronet LNG, Tenaris), and health care (Gedeon Richter).

Geographically, detractors included our investments and allocation in Taiwan (Parade Technologies), India (UPL Ltd, HDFC Bank, Axis Bank), and Egypt (Commercial International Bank of Egypt). India delivered weaker-thanexpected results, and the Egyptian government finally proceeded with the long-awaited floating of the foreign exchange rate but incurred a substantial currency devaluation. The greatest sources of outperformance came from individual investments in China (Yutong Bus, Shenzhen Transsion, Netease), South Korea (KB Financial Group, Samsung Electronics), and Peru (Credicorp).

Portfolio activity was higher than usual this quarter, as we initiated two new investments in China (Centre Testing International, China Resources Beer) and exited ITC Limited (India).

Centre Testing International is China’s leading domestic provider of third-party testing, inspection, and certification (TIC) services, an attractive market due to secular demand tailwinds supported by increasing product complexity and greater regulatory, health, and safety standards. Due to cyclical concerns regarding the Chinese economy, the company’s valuation has de-rated to levels that underappreciate growth prospects and CEO Richard Shentu’s ability to improve profit margins. China Resources Beer, the largest beer producer in China, is attractively positioned through its product portfolio and distribution network to capitalize on the structural trend of premiumization in China. We believe the stock price is not reflecting the upgrade of its mix towards premium products, underestimating the execution ability of CRB. With a recalibration of capacity and a focus on profitability, we believe the market is vastly understating not just the growth of free cash flow CRB can deliver, but also the realignment towards greater return of capital and more shareholder-friendly policies. ITC Limited, the dominant player in Indian cigarettes, has enjoyed strong pricing power in one of only a few markets that offer volume growth. Additionally, with a growing fast-moving consumer goods business and a shift to an asset-light model (linked to a potential spin-off of their hotel operations business), ITC’s valuation has discounted our thesis and moved beyond our estimated intrinsic value. We sold the position in favor of better opportunities.

We started managing the Altrinsic Emerging Markets Opportunities strategy on April 1, 2021, with an objective to grow client capital over the long term in a differentiated manner, developing a portfolio that truly reflects the DNA of the EM asset class. Today, as we assess how our differentiated perspectives and exposures have played out, we find great alignment with several elements of our starting hypothesis:

- Geographic breadth: We found underappreciated gems in less popular, non-traditional EM countries.

- Asset class DNA: We stayed true to the DNA of the asset class, finding more opportunities in the small and mid-cap space than the index reflects.

- Contrarian nature: Our contrarian approach led us to find undervalued companies in a stormy and volatile sector – Chinese real estate.

- Frontier exploration: Our expanded universe and willingness to spend time analyzing the path for off-the-beaten-track economies allowed us to identify unique companies in frontier markets.

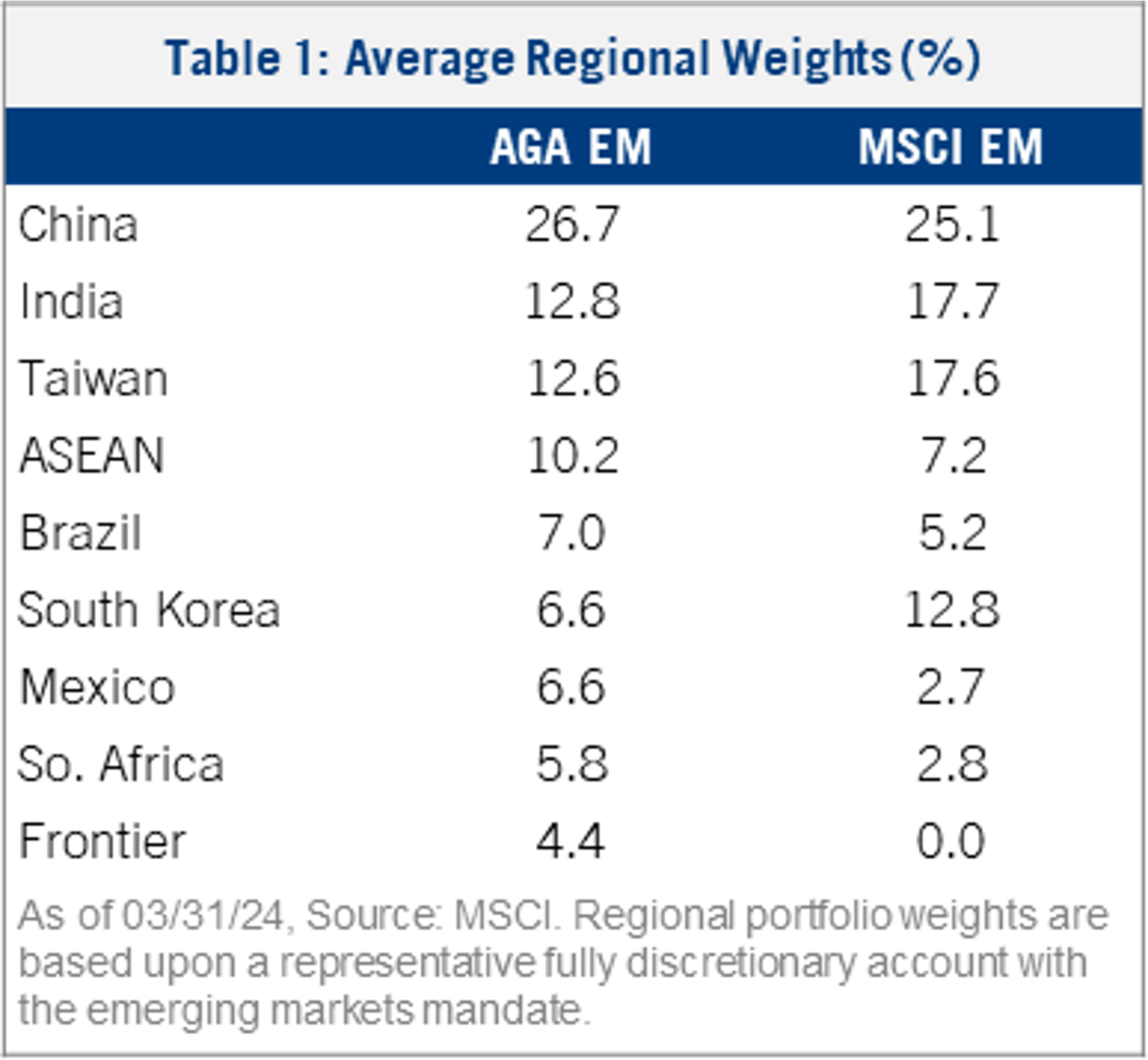

The “Other” EMs – Exposures within the MSCI EM Index remain lopsided and concentrated in three countries (China, South Korea, Taiwan), vastly ignoring the diverse set of smaller countries also classified as emerging markets (Table 1). Meanwhile, our companies in these “other” countries (including Mexico, Indonesia, and South Africa) have outperformed and contributed positively to portfolio returns over the past three years. Internal demand across these countries is supported by greater self-reliance given healthy demographics and pent-up consumer demand. Our portfolio companies across these countries have generated superior financial productivity and trade at attractive valuations.

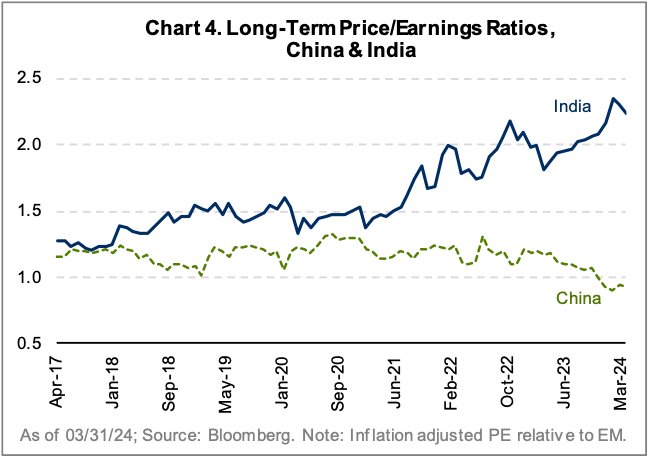

Our willingness to explore and invest in smaller countries does not imply that we are against investing in larger and more popular markets including China and India. In fact, from a bottom up perspective, we are now finding many undervalued Chinese companies (Chart 4), leading to our overweight exposure to China versus the benchmark. We invest where we find the best value, not where the index or headlines suggest investors should – or should not – put their money. Another good example is India, where we continue to find some compelling company specific opportunities in financials, energy, and utilities. However, from a financial productivity standpoint and based on recent on-the-ground due diligence, we believe many Indian stocks are now overvalued – right as the media is hyping the country as an “incredible”5 destination for investor capital.

Our willingness to explore and invest in smaller countries does not imply that we are against investing in larger and more popular markets including China and India. In fact, from a bottom up perspective, we are now finding many undervalued Chinese companies (Chart 4), leading to our overweight exposure to China versus the benchmark. We invest where we find the best value, not where the index or headlines suggest investors should – or should not – put their money. Another good example is India, where we continue to find some compelling company specific opportunities in financials, energy, and utilities. However, from a financial productivity standpoint and based on recent on-the-ground due diligence, we believe many Indian stocks are now overvalued – right as the media is hyping the country as an “incredible”5 destination for investor capital.

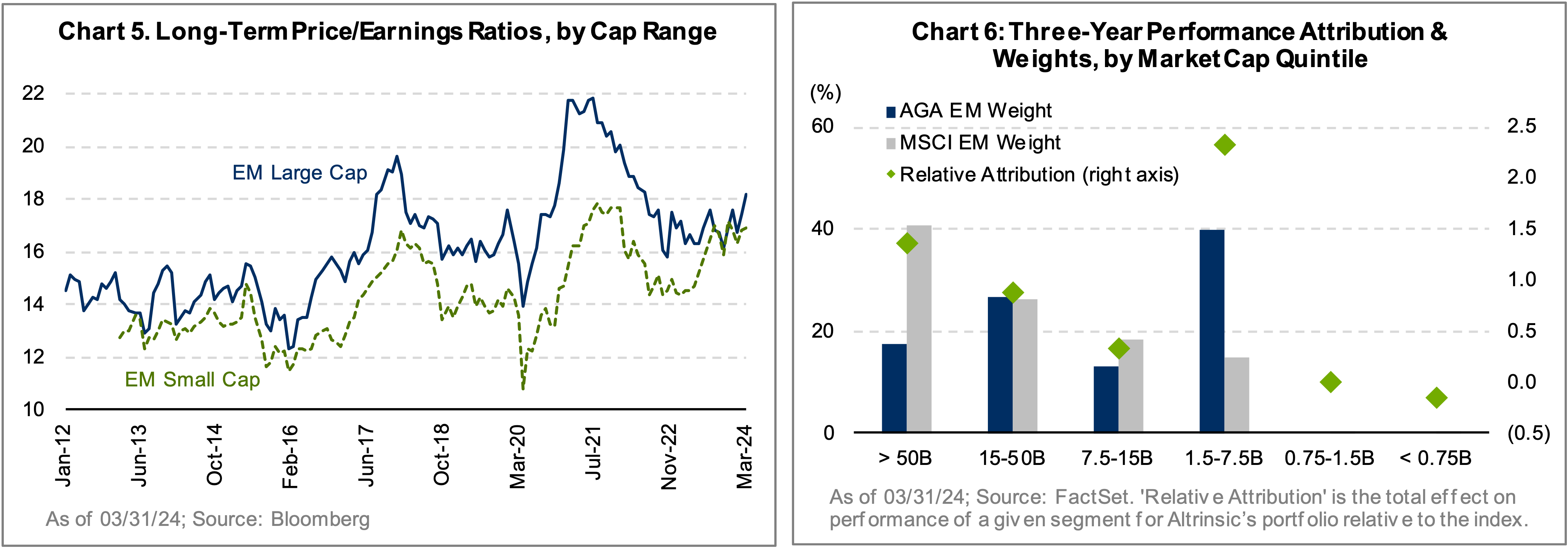

Small and Mid-Cap, the True DNA of EM – The DNA of the EM asset class is largely anchored in small and mid-sized businesses. For context, over half of EM companies (by count) fall into the small/mid-cap range ($1.5B- $7.5B USD), and yet this same group of companies represents just a 14.7% weight in the MSCI EM Index. Over the past three years, we observed the underperformance of the large-cap EM segment – driven predominantly by Chinese mega-caps – and the broader outperformance of small and mid-cap companies (Chart 5). Our bottom-up analysis and security selection process uncovered many mid-cap EM companies with compelling valuations, enabling us to build a portfolio that looks different than the mega-cap-dominated composition of the index. This overweight exposure to mid-cap stocks has contributed to about 50% of our outperformance since inception6 (Chart 6).

Contrarian and Unafraid to Look at the Unloved – We found value in unloved corners of the market, one example being contrarian investments in two SOE7 Chinese real estate developers. The Chinese government began tightening the screws on the sector, but despite this upheaval, we saw a clear dichotomy in company-specific performance across the sector and an opportunity to capitalize on a degree of market fear. Over the last three years, SOE developers with strong balance sheets have gained market share in this consolidating sector. These players have the ability to grow given their attractive landbank and funding, despite industry-wide concerns about inventories and demand. Despite the challenging post-pandemic economic conditions, both of our companies have recently increased their dividend payments and/or payout ratio, highlighting balance sheet strength and confidence in the outlook.

Frontier Markets Exposure – We specifically defined our universe to incorporate frontier markets, as we see untapped potential within countries that are evolving toward “emerging” status. In Vietnam, for example, we believe cyclical headwinds from local regulatory and political changes have been overly discounted in company valuations. Structural tailwinds remain in place with the relocation of the Asian supply chain supporting high foreign direct investment (FDI), income growth, and sustainable, higher consumption levels. Taking advantage of our ability to be nimble in less liquid markets, we watch for technical catalysts including settlement systems and EM status upgrades, which facilitate visibility (and potential opportunity) for the long term.

Closing Thoughts – Widespread AI-Driven Opportunity in EM

The breadth and depth of AI’s impact is undeniable. From an emerging markets perspective, we look beyond the top of the generative AI tech stack and instead focus on the diversity of companies – and opportunities – within the hardware supply chain that underpins the success and reach of AI. We believe this cycle’s value chain will be captured by a wider range of stakeholders – not just a handful of well-known and highly trafficked companies, including TSMC, Samsung, and Hynix. For many of these EM tech companies, the AI theme is a new, marginaccretive business driver with long-term optionality. But despite its potential impact, AI is not the only focus area driving growth for these companies. Importantly, we look for diversified and sustainable moats.

Our years of experience in emerging markets, disciplined investment process, and carefully cultivated networks lead us to find unique, undervalued, and financially productive companies focused on steady cash flow generation across the cycle and returning capital to shareholders.

Sincerely,

Alice Popescu