Dear Investor,

The Altrinsic Emerging Markets Opportunities portfolio gained 12.59% gross of fees (12.33% net), compared to the 8.72% increase of the MSCI Emerging Markets Index, as measured in US dollars.i After considerable volatility throughout the quarter, emerging markets performance took a dramatic positive turn during the last few weeks of September when Chinese leadership announced sweeping measures, both monetary and regulatory, to support the economy and boost capital markets. Coming into 2024, our portfolio was overweight China based on a bottom-up assessment of many high-quality, undervalued local businesses. While this positioning certainly contributed to our returns this quarter, the diversified and differentiated nature of our portfolio, including exposure to companies in other unloved and undervalued areas (Brazil, South Africa), had an even greater impact on performance.

Perspectives – Don’t Judge a Book by Its Cover

Two of the themes we are investigating this quarter can, for different reasons, be filed under the saying “don’t judge a book by its cover” – first, the relationship between return of capital and actual yields, and second, the investment opportunity set in the EM pharma sector.

Within developed markets, headlines tend to focus on the billions of dollars that a small subset of technology companies are spending on stock buybacks. These actions typically suggest that the companies feel their stock is undervalued and/or that they are confident in their future earning potential – yet a closer assessment of results shows pedestrian yields in many cases. Meanwhile, we believe that return of capital is one of the most overlooked features of EM investing, as more companies are simultaneously returning higher levels of capital and investing for the future.

Another underappreciated theme is the bottom-up investment opportunities in the health care industry within EM. Overall, the sector (and, specifically, the pharmaceutical sub-sector) has been a drag on broad market results. This poor track record, however, is driven by a concentrated set of companies that does not reflect the entirety of the opportunity set. When viewing the universe with a wider lens and a more contrarian perspective, we have found plenty of high-quality opportunities off the beaten path.

Buy High, Sell…When?

“Apple unveils record $110 billion buyback”– Reuters, 3 May 2024

“Big tech growth and lower rates to drive $1 trillion US share buybacks”– Share Magazine, 17 July 2024

“Nvidia’s $50BN share buyback”– CNBC TV18, 29 Aug 2024

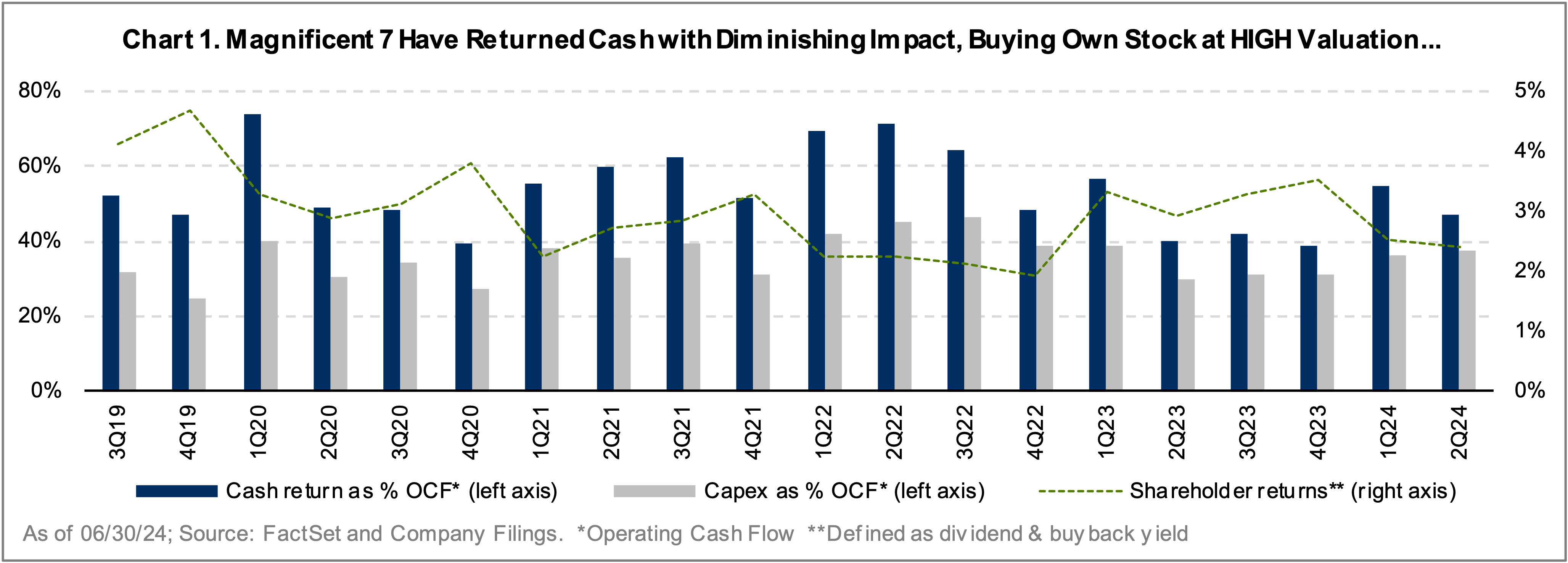

Financial engineering tends to be largely the domain of developed market companies seeking to drive earnings growth above operating income growth. Publications have been peppered with such headlines in recent months. Many DM companies have significant cash balances, enabling significant capital returns, which, in theory, should generate strong yields. However, upon closer inspection, we see that cash return yields for the largest companies remain at fairly disappointing levels in developed markets (Chart 1), partly due to these companies buying back their own stock at high valuations.

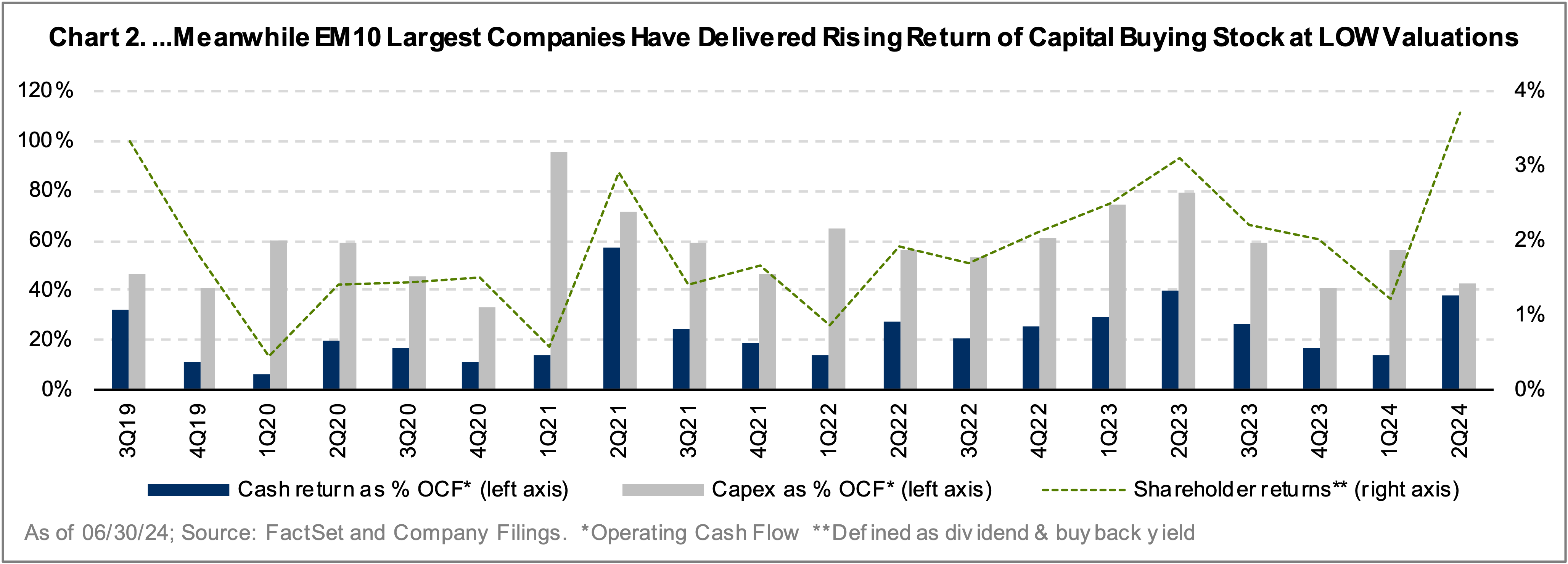

In emerging markets, the prevailing view has been that companies use operating cash flow primarily for capex (rather than cash returns), given the greater opportunities for capacity expansion in addressing new markets. What we find today, however, is that large EM companies are delivering increasing levels of capital returns while simultaneously also investing for growth by spending 40-60% of operating cash flow on capex (Chart 2). This dynamic is underappreciated and a potential driver of further stock re-rating.

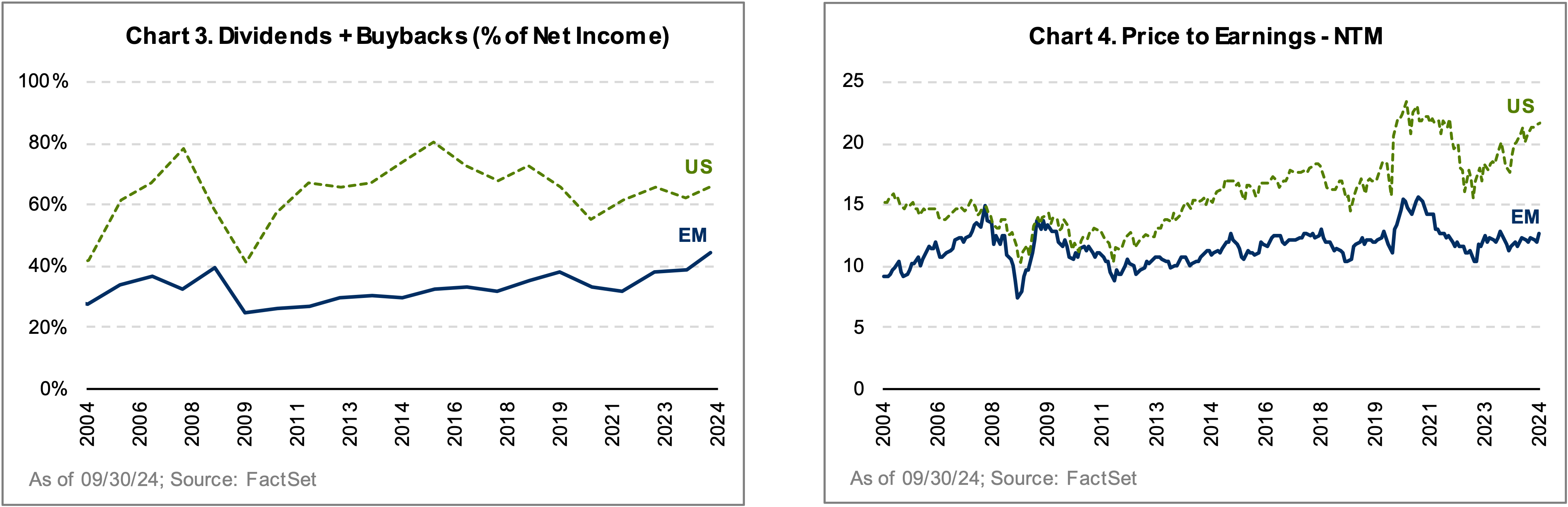

Despite such high capital intensity levels, EM companies actually increased their total cash return yields and have surpassed prior historical peaks, reaching 44% of net income (Chart 3). By comparison, US companies have failed to return to peak cash return yields while operating with lower capital investment intensity.

As is the case for us as investors, ‘price paid matters’ when companies initiate financial engineering schemes. Management teams in the developed world are buying back stock at ever-increasing valuations, particularly in the US (Chart 4), challenging future growth and showcasing deteriorating capital allocation choices. Meanwhile, EM management teams have done the opposite, buying low (at attractive valuations) so as not to sacrifice future growth.

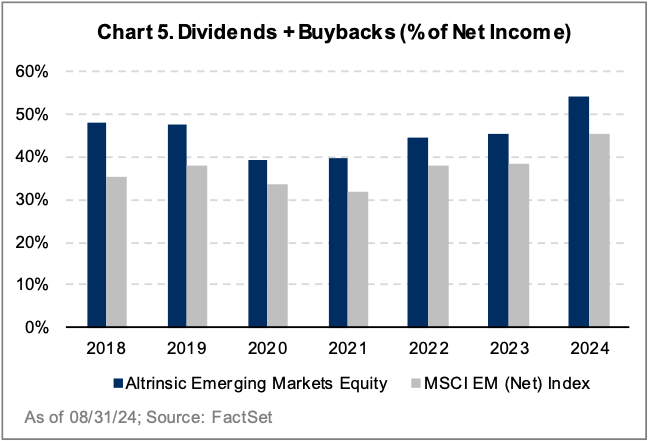

Looking at the companies in our Emerging Markets Opportunities strategy, return of capital has been an important source of alpha. Our continued focus on companies’ financial productivity has led us to businesses generating superior cash return yields compared to broad emerging markets (Chart 5). This trend has persisted even as cash return yields for the EM universe overall have been reaching new highs over the last several years.

EM Pharma…Not a ‘Jagged Little Pill¹

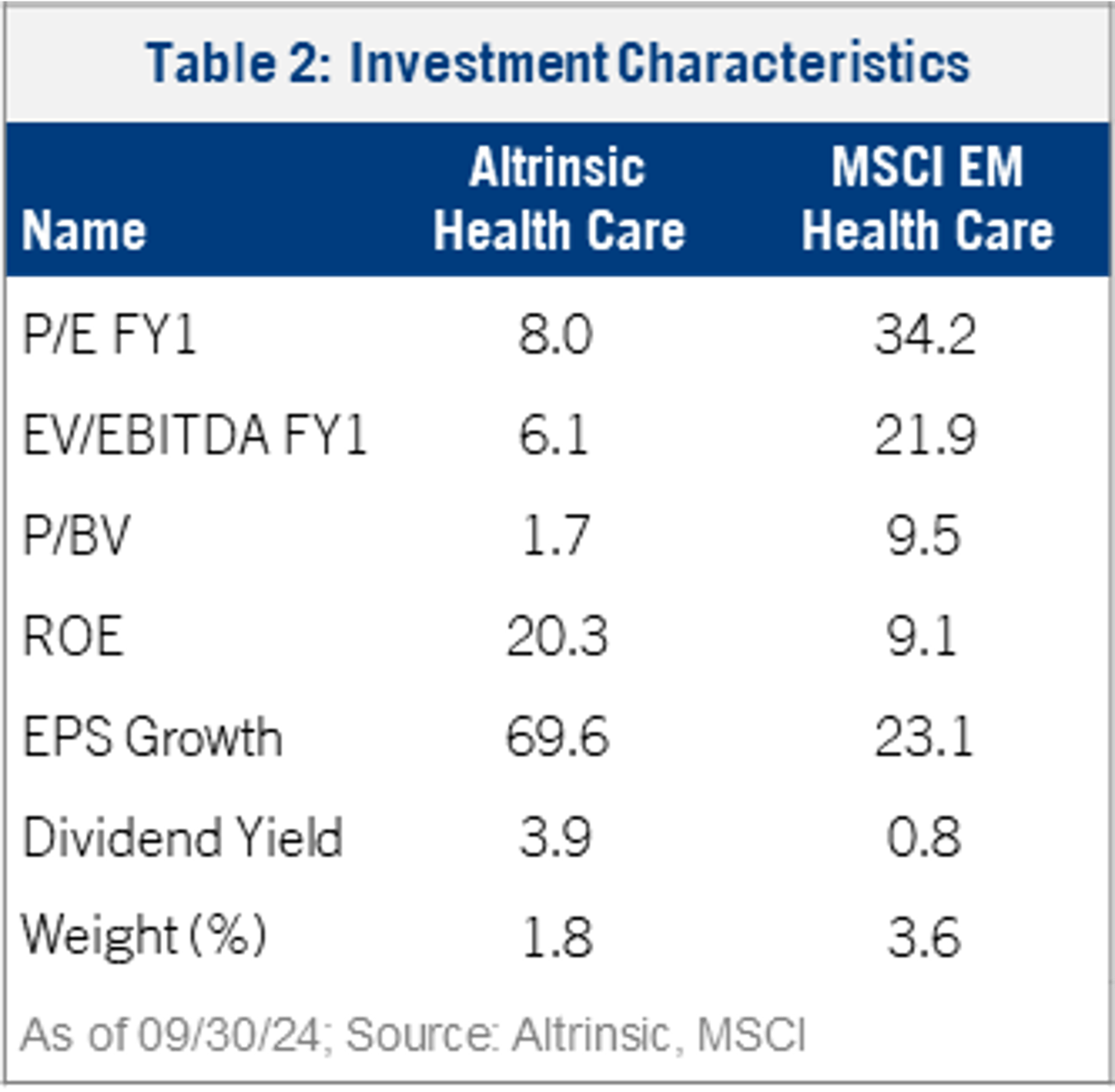

Looking at both short- and long-term performance, it is easy to see why investing in EM health care feels like a ‘jagged little pill.’ Relative to the broad EM index, as well as the MSCI World Healthcare Index, EM health care performance has lagged by meaningful margins across all major time periods (Table 1). We have been cautious about expanding our health care exposure (1.8% weight, versus 3.6% in the MSCI EM Index) given the less compelling broad trends, but we see some important drivers and themes that are underappreciated by the market and warrant additional focus and consideration. The EM health care companies we do own (based on a careful bottom-up analysis) have demonstrated superior returns on equity, earnings growth, and dividend yields, while being undervalued across several different measures, relative to benchmark constituents (Table 2).

Taking a deep dive into the data reveals that the disappointing results across the broad EM health care ecosystem have been driven primarily by Chinese companies. The EM health care universe is very concentrated; approximately 57% of the liquid and investable universe overall is made up of Chinese companies, with most of the rest from India and South Korea. Further, about two-thirds of the investable universe is comprised of pharmaceutical companies, of which about 65% are Chinese.² The MSCI EM Healthcare Index is similarly concentrated in terms of geography and even more concentrated in terms of pharma representation. Collectively, the companies that we will refer to as the “Pharma & Co.”³ segment (for simplicity) represent a 73.7% weight within the MSCI EM Healthcare Index.4

Broadly speaking, Pharma & Co. companies across emerging markets have not been known as innovation leaders relative to their developed market peers. Even China, widely considered to be the most innovative country within the EM landscape, still faces a clear technology gap within the innovative biopharma segment, capturing far less market share than it does within other industries (Chart 6). Nonetheless, amidst the recent volatility across EM, and despite the lackluster results overall for EM health care companies, we believe that EM Pharma & Co. (particularly outside the major EM markets) offers some compelling opportunities for those willing to look – easier pills to swallow, if you will.

For the last several quarters, we have talked about the broadening prevalence of financial productivity outside of the large, well-known markets of China and South Korea – and in the case of the health care sector, it is important to look beyond India as well. As we assess the quality and value of companies in the Pharma & Co. sector, four key themes stand out:

-

- First, the financial productivity of EM pharma companies has risen above pre-pandemic levels, and in countries outside Asia, the ascent has been notably steeper (Chart 7). Meanwhile, the financial productivity of developed market pharmaceutical companies has largely plateaued in recent years.

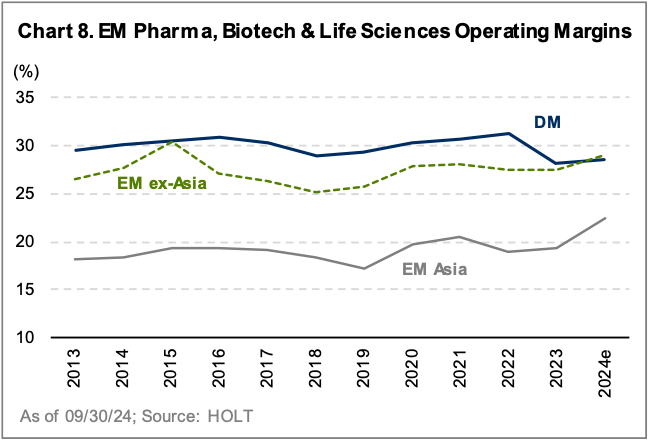

- Second, returns for EM Pharma & Co. companies outside large Asian markets are rising faster. Profitability levels of EM ex. Asia companies have historically been superior to EM Asia. Recently, companies in these less mainstream countries have closed the margin gap to DM pharma companies as well (Chart 8).

- Third, the laser-focused management of the asset base has delivered productivity. Asset turns have stabilized in EM ex. Asia, while we see deteriorating trends in other regions

- First, the financial productivity of EM pharma companies has risen above pre-pandemic levels, and in countries outside Asia, the ascent has been notably steeper (Chart 7). Meanwhile, the financial productivity of developed market pharmaceutical companies has largely plateaued in recent years.

- Finally, even with these quality features in mind, valuations are extremely compelling for EM ex. Asia pharma stocks, as prices are discounting near-decade-high risk levels relative to Asian counterparts. We believe the segment will be an enduring source of opportunity as these themes play out.

Richter Gedeon, a Hungarian generic and branded drug manufacturer, is one of the compelling investment opportunities we have identified in the widely unloved EM health care sphere. The company benefits from a globally successful central nervous system drug with a rising royalty stream. These cash flows have enabled the company to invest and build an innovative biosimilar franchise as well as a unique women’s health care (WHC) franchise. The latter has begun to address medical issues from contraception to fertility to chronic diseases, including endometriosis. In a report5 jointly published by the World Economic Forum and the McKinsey Health Institute in January 2024, it was said that “Investments addressing the women’s health gap could add years to life and life to years – and potentially boost the global economy by $1 trillion USD annually by 2040.”

Our investment in Richter also brings a differentiated geographic dimension to our portfolio’s exposure. Richter is a Hungarian company with a low-cost manufacturing footprint predominantly within emerging markets, but its revenue stream has broad global reach. This is unique and refreshing vis a vis the heavily trafficked Asian companies. The company’s ability to drive financial returns through a diversified portfolio while developing an innovative pipeline – at an extremely discounted valuation, to boot – makes us excited about the future.

Performance Review

The Altrinsic Emerging Markets Opportunities portfolio’s outperformance was driven by our overweight positioning in China, South Africa, and Brazil, as well as our underweight exposure to South Korea. From a traditional sectoral perspective, performance was driven by stock-specific factors in information technology, materials, and financials, as well as our underweight exposure to information technology. India and Mexico (from a regional perspective) and health care (from a sector perspective) were marginal detractors due to a combination of relative positioning, FX, and stock-specific effects.

The greatest sources of outperformance from a regional point of view came from stock-specific effects in Brazil (Lojas Renner, Porto Seguro, Banco Bradesco), South Africa (Mr Price, Standard Bank, Clicks), and China (Shenzhen Transsion, Yum China, Centre Testing International), as well as our underweight exposure in South Korea. In Brazil, strong earnings recoveries and upward revisions of economic growth projections drove the performance of our undervalued stocks. In South Africa, the market reacted positively to the newly elected government, and, together with start of an easing cycle, the valuations of our companies started to recover.

From a sector perspective, within information technology, Chinese handset manufacturer Shenzhen Transsion rebounded following the resolution of a prior corporate governance issue, while Taiwanese supply chain vendor Chroma ATE benefitted from strong business execution in the quarter. Within materials, Egyptian gold miner Centamin was bought out by Anglogold Ashanti at a significant premium, boosting the stock price, and Ganfeng Lithium rallied substantially in line with the broader Chinese market. In financials, several of our holdings delivered resilient earnings in the context of changing interest rate cycles (AIA, Porto Seguro, Bank Mandiri), leading to substantial outperformance. Our underweight exposure to information technology also contributed to our outperformance; we had previously trimmed/eliminated positions in this sector to fund new investment opportunities.

Investment Activity

We initiated one new investment (Sumber Alfaria Trijaya – “Alfamart”) this quarter and strategically added to and trimmed several other investments.

Alfamart is the leading convenience store operator in Indonesia with a solid track record of opening new stores and generating above-inflation-level same-store sales growth (SSSG). The company is well positioned in the structural shift from traditional retail to modern trade in Indonesia. The country represents the largest addressable market in the ASEAN region but has one of the lowest levels of modern trade penetration. We believe Alfamart will close the margin gap to regional and global peers through operating leverage, store mix optimization, potentially higher franchise exposure, and increased service fee collections. Currently, the company is trading at an undemanding valuation and provides a compelling risk/reward trade-off. We funded this new position with gains from some of our information technology companies in Taiwan and India and from some of our South African holdings.

Concluding Remarks

“Let China Sleep, for when she wakes, she will shake the world.”

– Napoleon Bonaparte

At the end of the third quarter, China’s president Xi Jinping and his broader leadership team attempted a ‘mic drop’ moment. A very busy and coordinated effort from China’s economic and financial leadership was designed to shore up domestic capital markets and the economy. Whether or not it will ultimately be successful remains to be seen.

The PBOC (central bank) enacted various liquidity measures (including interest rate cuts) and easing for mortgage financing and down payments. Financial markets regulators unlocked the ability for various financial firms to step in and support equity markets. A recapitalization of major state banks was also floated, while additional discussion about unwavering fiscal support was announced.

In the short term, these policy announcements serve as a temporary catalyst for market performance, but for the momentum to continue, we will also need to see improvements in business fundamentals. Stimulatory measures will need to work their way through the system, and both business and consumer confidence will need to recover…sustainably. No matter how excited markets seem right now, those things will not happen overnight.

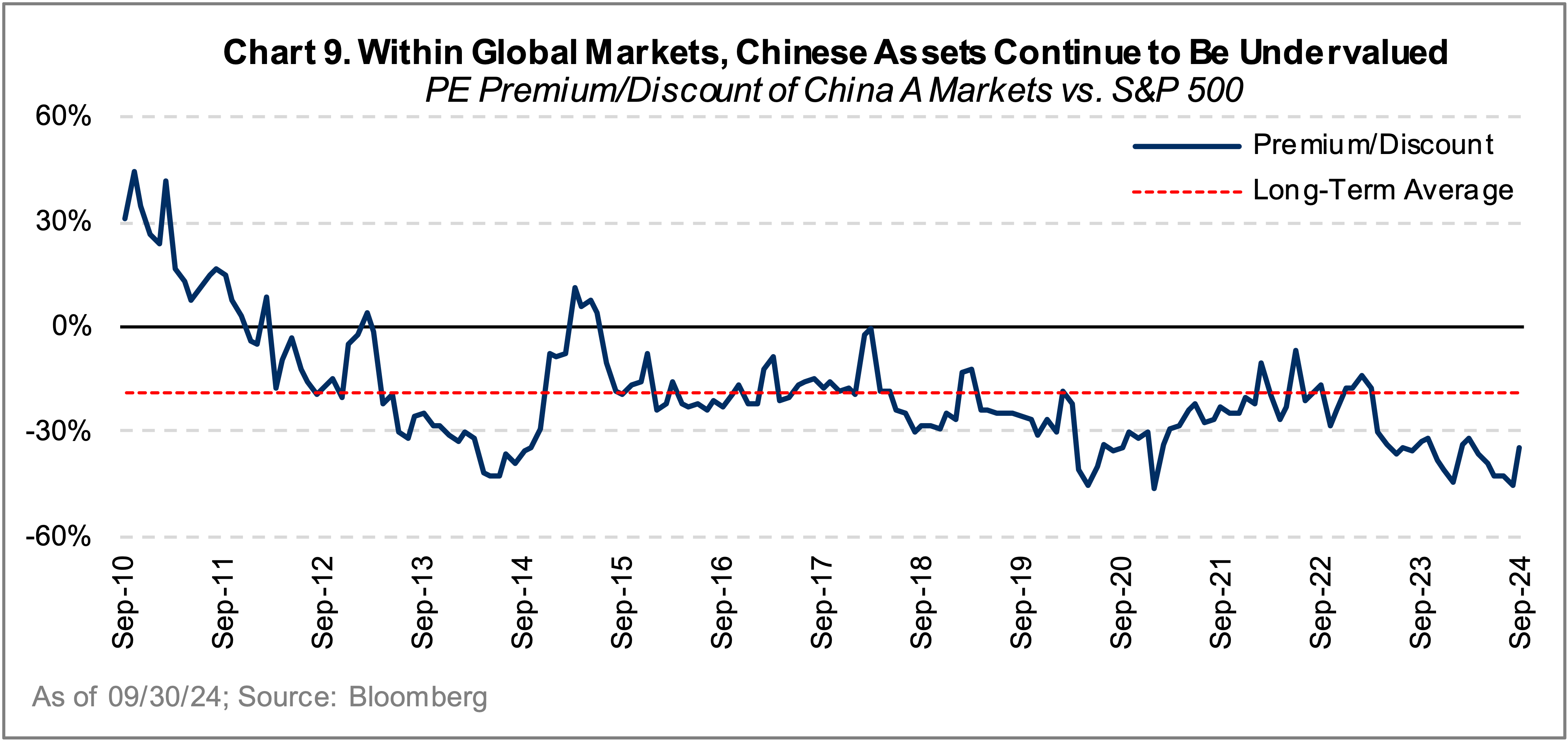

Despite a multi-week market rally, the companies in our portfolio remain deeply undervalued (Chart 9). Interestingly, domestic investors seem to be some of the most bearish ones – and broader buy-in and enthusiasm seems to start with them. The stock reactions show how unloved and undervalued this market has been for some time – and, for now, continues to be.

For now, we have not meaningfully changed any of our assumptions or positioning regarding China. With our inherent focus on undervalued businesses demonstrating sustainable financial productivity, paired with our willingness to take a contrarian stance, our Chinese exposure has reached 29.9% (versus 27.6% within the MSCI EM Index), up from 24.8% at the start of the year.6 Chinese real estate (SOEs) is one of our most differentiated and contrarian exposures, and the discounts to intrinsic values remain substantial. Recent announcements are supportive for the property market, and property adjacent/related companies could also benefit from this effort. However, we believe consolidation and volatility will continue for some time.

Our broad EM decoupling thesis is predicated on emerging markets countries (including China) creating greater self-sufficiency in technology and industrial policy while also increasing trade with other EM nations. While we welcome the rising tide, we are cognizant that it will not lift all boats and that the waters are rough. In the case of China, periods of volatility will continue to test the depth of Beijing’s stimulus coffers, particularly as we wait to see the results of the US presidential election in November. As always, we are ready to buckle up and enjoy the ride.

In the meantime, we just returned from some Andean adventures – stay tuned for on-the-ground insights from Chile and Peru.

Sincerely,

Alice Popescu