Dear Investor,

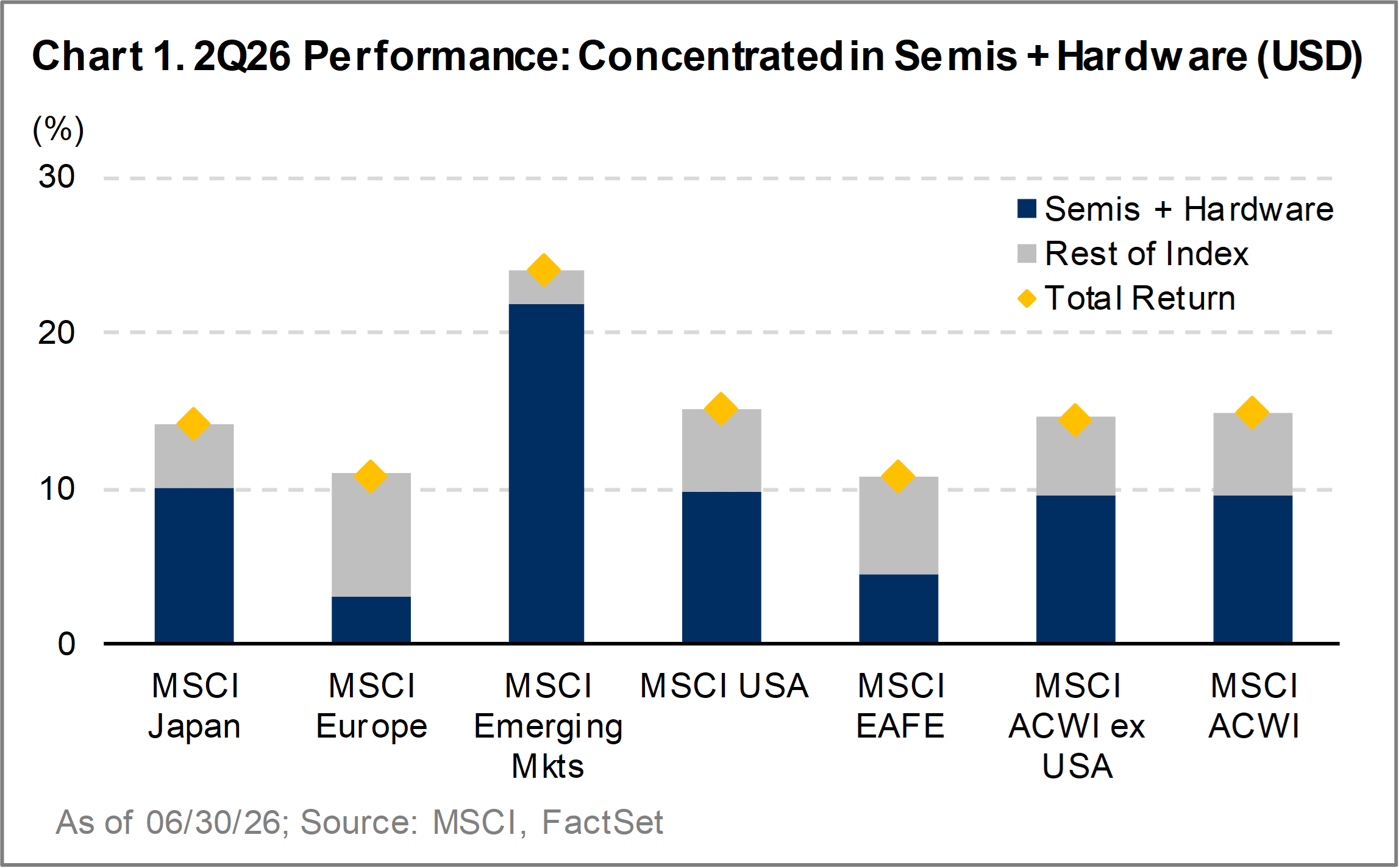

As Mark Twain once said, “Whenever you find yourself on the side of the majority, it is time to pause and reflect.” This quarter, the “majority” was easy to identify. Roughly 90% of the MSCI EM Index’s returns came from semiconductors and tech hardware, and nearly 70% came from just three stocks. As the market considers the implications of this unprecedented level of concentration, we have been more deeply investigating several considerations receiving less attention – commodity price exposure, peak-cycle earnings, and borrowed money.

Our curiosity and investigative discipline shapes what we own and how the portfolio is built. We have exposure to the technology theme, including memory, but we are selective – avoiding the commodity producers whose pricing power we believe to be cyclical rather than structural. Across industries, we are focused on companies with some of the sturdiest balance sheets we have seen in EM in years, built to withstand higher-for-longer rates. In both cases, durability designed, not declared.

The MSCI EM Index gained 24.1% this quarter, as measured in US dollars.i Against this backdrop, and amidst the narrow market leadership driven by a small subset of companies (Chart 1), the Altrinsic Emerging Markets Opportunities portfolio underperformed, gaining 12.1% gross of fees (11.8% net).

Technology: Investing in the Theme, Owning It Differently

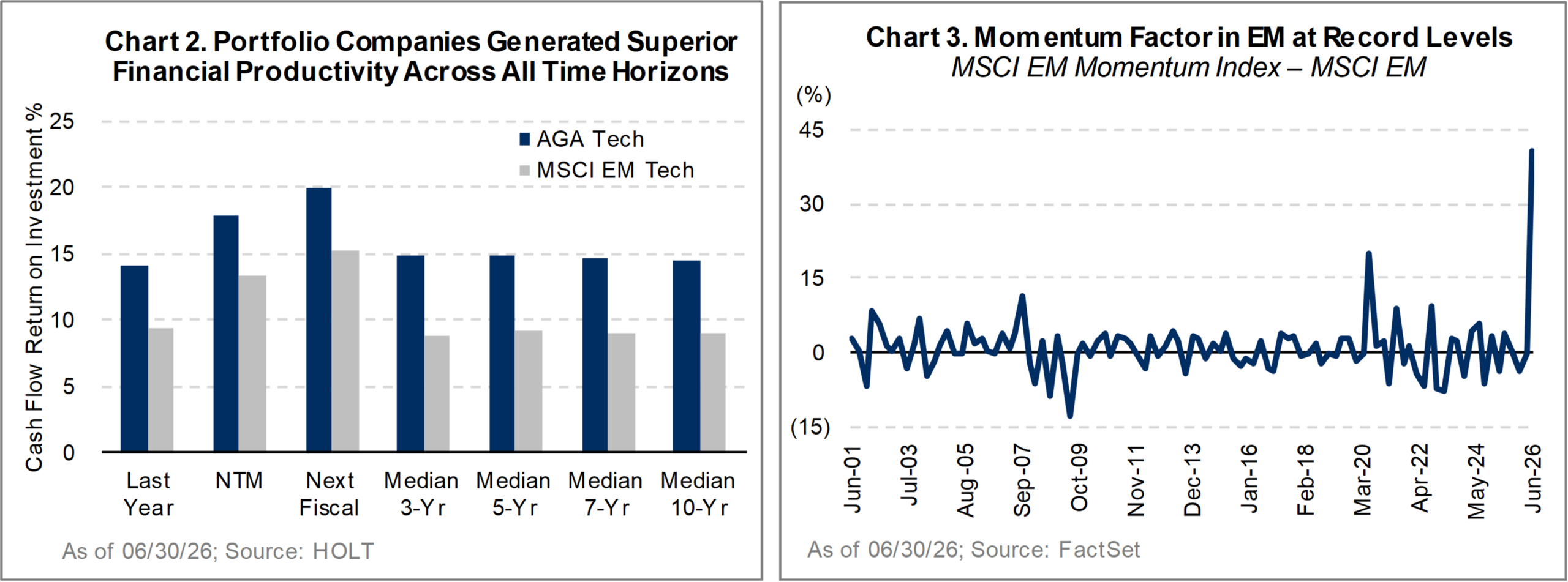

History suggests that stock market returns powered by a highly concentrated market are rarely sustainable over the long term. Across four decades, rising returns on invested capital have driven EM technology companies to grow their balance sheets in pursuit of that opportunity, only for surging asset growth to push industry returns back down toward the cost of capital as capacity normalizes – most starkly illustrated during the dot-com build-out. Now, forecasted returns on invested capital sit at record highs just as capital intensity accelerates. Technology hardware is capital intensive and highly cyclical. The current cycle has surpassed previous peaks and duration, with powerful driving forces that are susceptible to change. In light of this, and consistent with our long-term perspective, we seek undervalued technology companies that compound quietly through multiple cycles (Chart 2), applying the same balance sheet lens we use for all emerging market businesses. By doing so, we accept that we might be out of step when a single trade dominates the tape, as it has this quarter (Chart 3).

1. Separating Cyclical Benefits from Structural Advantage

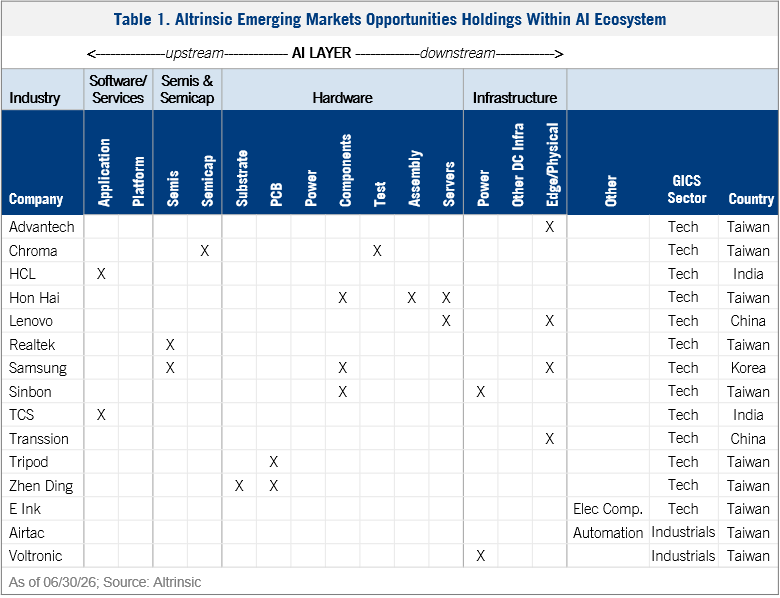

We believe the market is conflating short-term pricing power (created by explosive growth in demand and an exceptional supply shortage) with genuine structural innovation. Today’s supernormal profitability reflects scarcity as much as technological leadership, making it difficult for many companies to sustain current returns on invested capital as supply normalizes. That is why we choose to be positioned differently. We prefer businesses with unique technology, recurring demand, and defensible market positions over those reliant on commodity pricing. Our technology exposure spans companies involved in semiconductor testing, uninterruptible power, cabling and connectivity, printed circuit boards and chip substrates, PCs and smartphones, and servers – much of the critical infrastructure that allows AI to function (Table 1).

We have owned Samsung since the inception of the Altrinsic Emerging Markets Opportunities strategy over five years ago; our concern is not memory companies themselves, but rather the current tendency to treat peak-cycle economics as permanent. Meanwhile, a concentrated position in South Korean memory stocks like SK Hynix is, in our view, a single commodity bet, as Chinese competitors are closing the gap every quarter, adding further pressure. South Korea’s financial services regulator publicly expressed regret1 for approving leveraged single-stock ETFs on the two memory makers, products that pushed retail margin lending to a record $40 billion USD. When a regulator laments the speculation built on two stocks, we take note.

2. The Bar for Memory Earnings is Exceptionally High

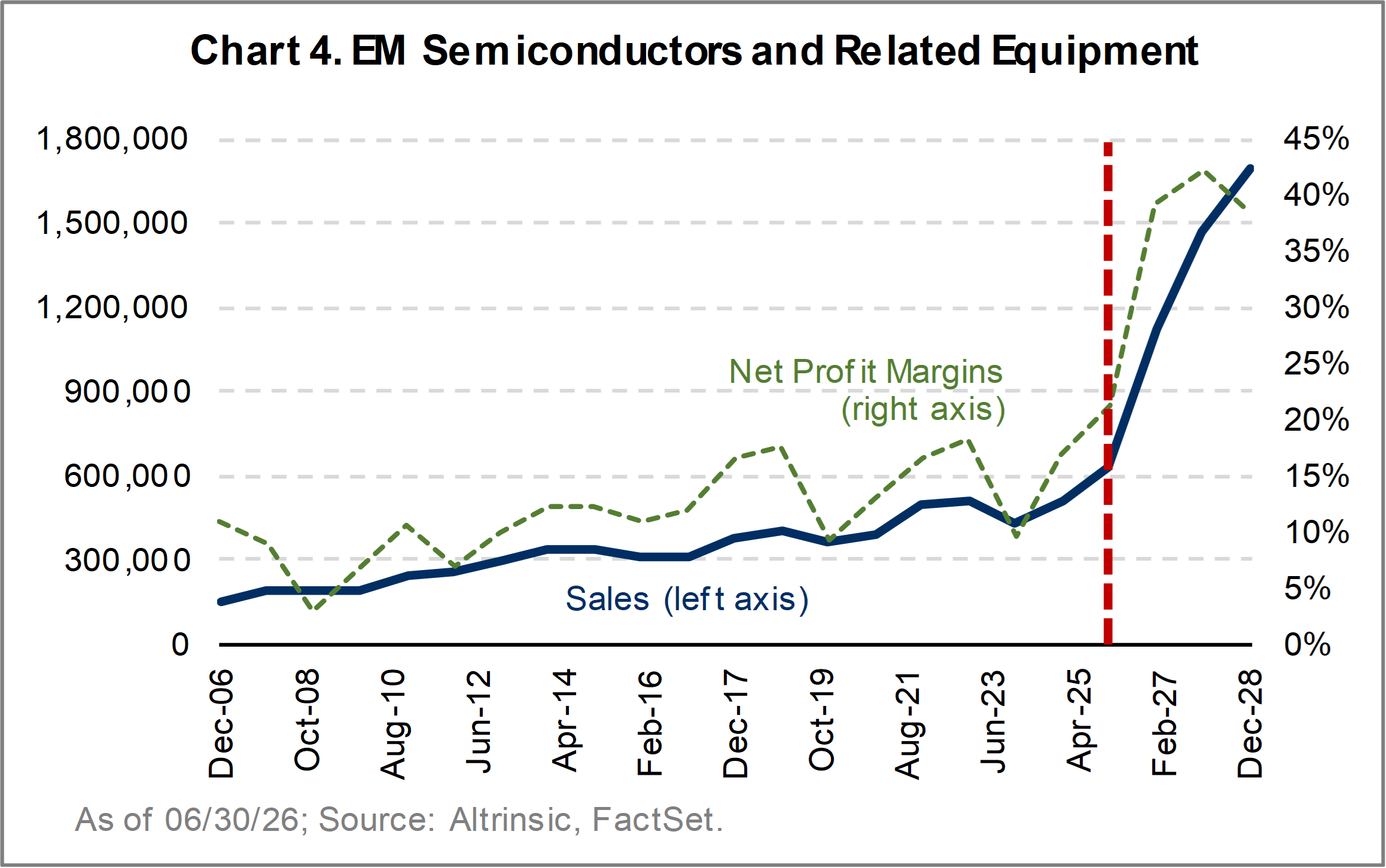

Commodity DRAM contract prices are up over 600%; every prior surge ended in 50–60% drawdowns. EM semiconductor stocks may, in aggregate, appear cheap on a forward profit margin basis, but we believe those expectations are exceptionally high as that view assumes sales nearly triple between 2025 and 2028 and profit margins sustain at 2-3x their long-term average (Chart 4). Hitting that bar would require multi-year linear growth in an industry defined by short, sharp cycles – even when the long-term structural trend is intact. The real threat of accelerating Chinese competition further exacerbates the challenge. We are looking for businesses where normalized, through-cycle earnings compound. Memory, by contrast, tends to destroy capital at the trough.

3. China is Closing the Gap, One Qualification at a Time

We see Chinese competition as a clear emerging threat, not a tail risk.2 China’s leading memory players, CXMT3 and YMTC, already hold about 10% of the global DRAM market share. Apple has requested permission to buy from these ‘blacklisted’ Chinese companies, and should they receive it, others may not be far behind.4 When the world’s most powerful component buyers formally approve Chinese memory manufacturers, excess supply is likely to follow, severely hampering the incumbents’ pricing power.

4. Where Compounding Meets Quality Multiples

Businesses like Chroma ATE (test and measurement), Advantech (industrial computing and edge AI), Sinbon (electrification and electronification cabling), and Tripod (printed circuit boards) earn through the cycle with recurring demand, defensible niches, and no commodity price exposure. We believe the compounding math favors them over producers that are hostages to a spot price over the long-term. This shows up directly in our bottom-up driven positioning: hardware and equipment – including the multi-cycle businesses above – represent 84% of our technology holdings versus 38% for the index; semiconductors are 8% versus 60%; and software services are 8% versus 2%, driven by enterprise digitization rather than AI capex.ii The result is exposure to the AI theme’s higher-quality expression, at multiples that do not demand perfect cycle timing.

We believe our emerging markets technology exposure is differentiated in both composition and philosophy. Memory giants like SK Hynix are raising record capital to spend record sums, right at the point in the cycle when capex goes from celebrated to questioned.5,6 Rather than chase peak-cycle memory economics, we favor the infrastructure layer underpinning AI, businesses with recurring demand and defensible niches, and valuations that do not assume flawless cycle timing – while remaining clear-eyed about the competitive threat China’s domestic champions pose to incumbent pricing power. As of this writing, despite an underweight positioning in the tech sector overall (Altrinsic EM Opportunities 22.6%; MSCI EM Index 45.3%), we are invested in thirteen tech businesses, including ten in Taiwan and many off the beaten path (see Table 1 for details).

Sturdier by Design: EM Balance Sheets in a Higher-Rate World

Last quarter, we argued EM financial institutions had quietly become better run, better capitalized, and more durable than credited. This quarter, we widen the lens outside financials: interest rate pressure persists, but EM companies carry less debt and longer maturities, invest without stretching their balance sheets, and earn financial productivity through operating profitability, not leverage. This balance sheet progress is also reflected by EM corporate credit spreads, which are near all-time lows.

Inflationary pressures driven by surging memory prices, the Middle Eastern conflict, and other factors have paused the anticipated global interest rate-cutting cycle. Markets that entered 2026 expecting meaningful EM easing now price in broadly flat rates, with energy-importing Asia pricing roughly 36 bps of hikes.

Still, relative to DM, the inflation differential in EM countries remains near decade lows. By the end of the quarter, oil prices had retreated, but a continuation of geopolitical volatility is keeping interest rate risk elevated. The difference this cycle: EM companies confront it with the sturdiest balance sheets in years.

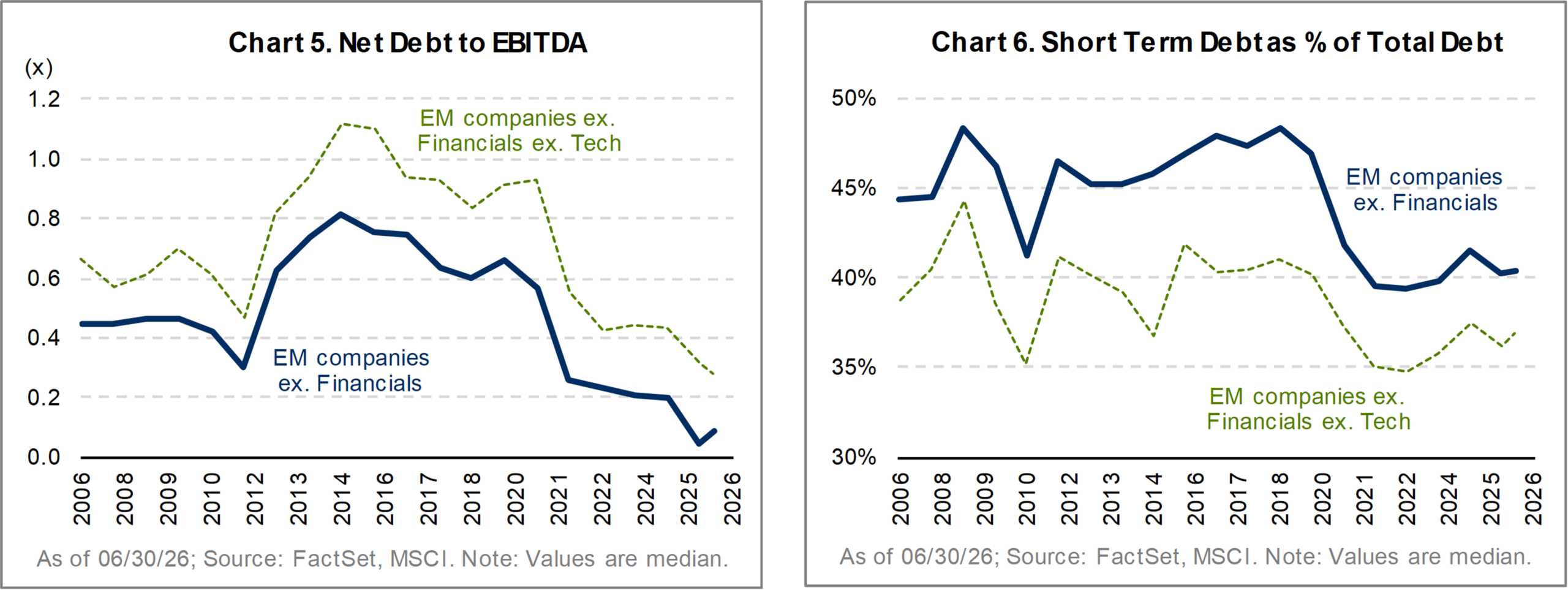

EM companies carry less debt than legacy concerns imply; net debt/EBITDA hovers near historic lows (Chart 5), and interest coverage is at 7-8x, with debt mostly in local currency. Debt maturity management tells the same story: short-term debt is down to around 40% of the total (Chart 6), reducing rollover risk precisely when it matters.

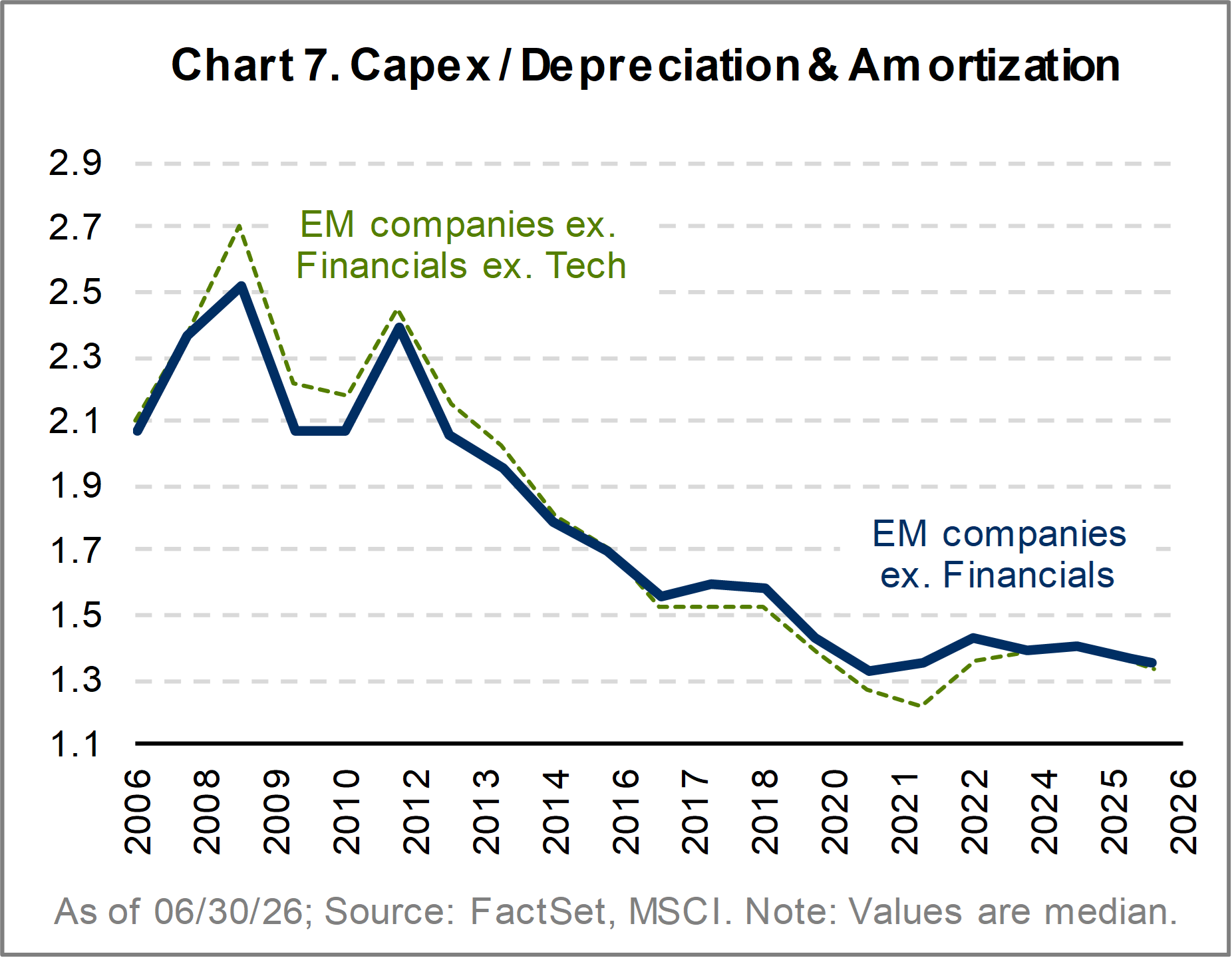

This balance sheet discipline has not come at the expense of growth. Capex/D&A7 has fallen from above 2.0x to roughly 1.35x (Chart 7), indicating EM companies continue to invest. But they have done so prudently, as goodwill8 remains just 0.3% of assets despite also pursuing acquisition-supported growth.

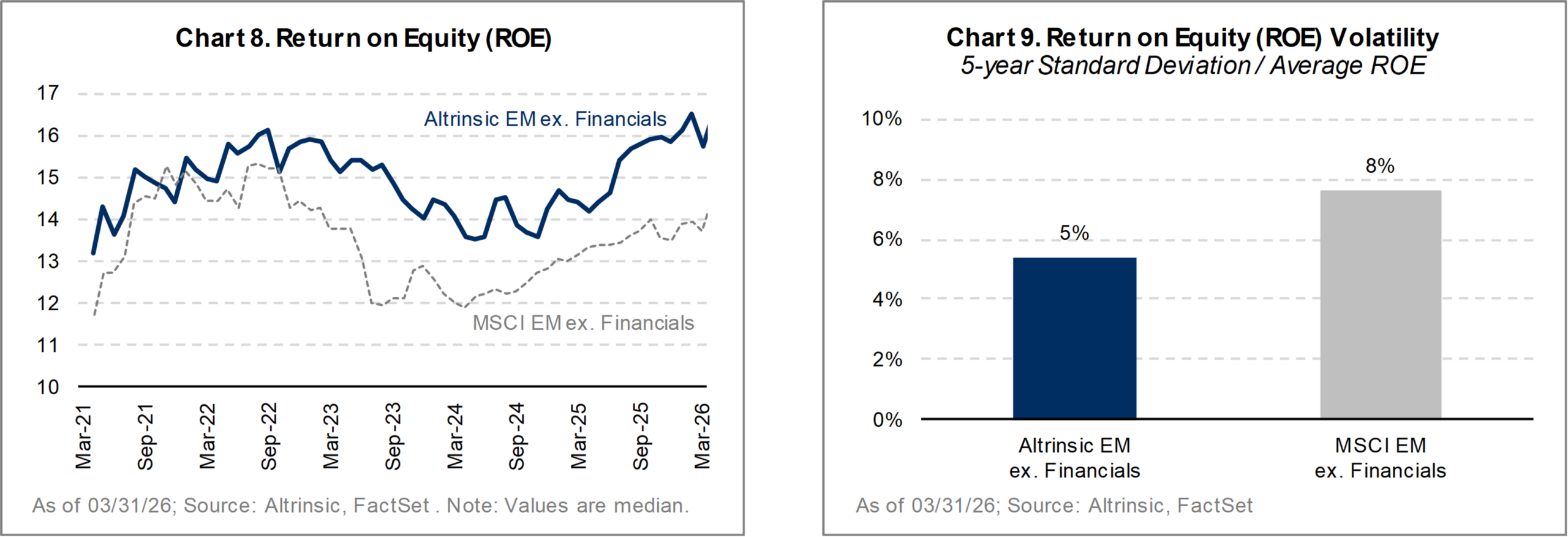

The source of returns on equity (ROEs) matters as much as the levels. ROEs have expanded over the past decade on the back of better profitability and operating quality. Asset turns are near decade highs while leverage peaked pre-pandemic. ROEs from asset productivity are durable, while those from leverage are not.

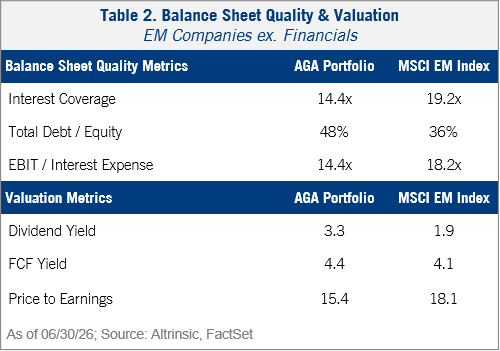

Our portfolio sits at the deep end of this quality upgrade. It has demonstrated a persistent ROE premium of roughly 150-200 bps for most of the past five years (Chart 8), with approximately 30% lower earnings volatility (Chart 9). It earns more…and more consistently…without extra leverage. The portfolio matches the index on balance sheet quality and has interest coverage of 14.4x, while delivering higher dividend and free cash flow yields at a meaningfully lower P/E (Table 2).

The bottom line: Today’s MSCI EM universe reflects a clear quality upgrade with higher margins and stronger ROEs from operating efficiency, rather than borrowed money, as well as falling balance sheet risk. Our portfolio holds the sharper end of that upgrade. Low debt. Longer maturities. Better financial productivity. In a world where interest rate risk refuses to retire, this is the resilience we want to own.

Performance Review and Investment Activity

The greatest sources of positive attribution this quarter were health care (Richter Gedeon), energy (Petronet), and real estate (Vinhomes). Negative attribution came primarily from our relative underweight exposure to, and positions in, information technology (Samsung, Tata Consulting Services, HCL Technologies), consumer staples (Raia Drogasil, China Resources Beer, Sumber Alfaria), and industrials (Grupo GPS, Corporacion America Airports SA, Motiva).

From a geographic perspective, gains in China (Lenovo, Tencent, Airtac) and the Philippines (International Container Terminal Services), as well as our underweight positioning in Saudi Arabia were sources of positive attribution. These were offset by our underweight and specific exposure to South Korean companies (Samsung, Silicon2, Krafton) as well as not owning SK Hynix; some of our Indonesian stocks that remained under pressure due to a regulatory hurdle from MSCI ratings as well as government policies and a weaker currency (Telkom Indonesia, Bank Mandiri, Sumber Alfaria); and our exposure to Brazil (Raia Drogasil, Grupo GPS, B3 SA – Brasil, Bolsa, Balcao).

Portfolio activity was low, as we exited two positions. In Brazil, we sold Banco Itaú as valuations surpassed our most optimistic medium-term return scenarios. In China, we sold China Resources Gas in favor of better risk-reward opportunities elsewhere in the portfolio. We trimmed several information technology holdings which reached our bull-case scenarios as AI enthusiasm surpassed historic levels, and we reinvested in Brazilian holdings that reported solid results but lagged on macro concerns including slower rate cuts and rising political volatility.

Concluding Remarks

“Quality without results is pointless. Results without quality is boring.” – Johan Cruyff

Johan Cruyff, the Dutch football player-turned-manager who won eleven major championships as a manager, scouted talent wherever it lived, championing stars from Bulgaria and Brazil when rivals looked only to Europe’s traditional powerhouse countries. We invest much the same way, pursuing quality companies wherever they are found – our version of ‘total football’9 on the EM pitch. Further, our discipline forces us to discover what sits beneath any result (whether earnings are at cycle peaks, pricing power can last, or returns on capital rest on leverage), as we look for quality, rather than lucky outcomes. We seek to own businesses that earn through the cycle, not just at its crest, built on what we believe are the sturdiest EM balance sheets in years.

Sincerely,

Alice Popescu