Dear Investor,

Q1 was a challenging environment across equities, fixed income, and certain alternative asset classes – notably crypto and private credit. Markets were shaped by uncertainty around AI-driven disruption, escalating conflict in the Middle East and the resulting energy price volatility, ongoing supply chain disruptions, and weakening consumer confidence. The Altrinsic Global Equity portfolio declined 2.3% (-2.5% net), as measured in US dollars, outperforming the MSCI World Index’s 3.6% decline.i

Our emphasis on valuation, business quality, and durable growth positions the portfolio well given the wide range of potential outcomes stemming from geopolitical tensions and AI-related disruption. We continue to favor “shorter duration” equities – those with visible and durable earnings power – as opposed to companies dependent upon long-term narratives and highly aspirational “expectations” that earnings come through to justify very high valuations.

Amidst the uncertainty, we are seeing a growing opportunity set emerge. This includes companies with exposure to regions navigating near-term geopolitical pressures, particularly in parts of Asia and India, as well as high-quality businesses that have been indiscriminately sold amid heightened concerns around AI disruption. In many cases, we believe these risks are overstated, creating attractive entry points.

Wartime Considerations

There are known knowns. These are things we know that we know. There are known unknowns. That is to say, there are things that we know we don’t know. But there are also unknown unknowns. There are things we don’t know we don’t know.

– Donald Rumsfeld, former US Secretary of Defense

The “known unknowns” and “unknown unknowns” outnumber the “known knowns” when it comes to forecasting how the Middle East conflict plays out. Our view is that the “blue sky,” or Goldilocks, scenario – involving regime change, full abandonment of nuclear capabilities, and uninterrupted flows through the Strait of Hormuz – is highly unlikely. The Islamic Revolutionary Guard Corps controls Iran, has all the guns, and is willing to withstand economic hardship longer than President Trump is willing to endure political pressures or the global economy is able to endure economic pressures.

Outside the “blue sky” scenario, the most likely outcome is some combination of slower growth and higher inflation relative to pre-conflict conditions. Never has so much hinged on a “tweet” or a “Truth.” The extent to which global economic growth suffers depends on many factors, some of which include where oil prices settle, policy responses, the pace of deglobalization driven by supply chain restructuring, and tech-related productivity gains.

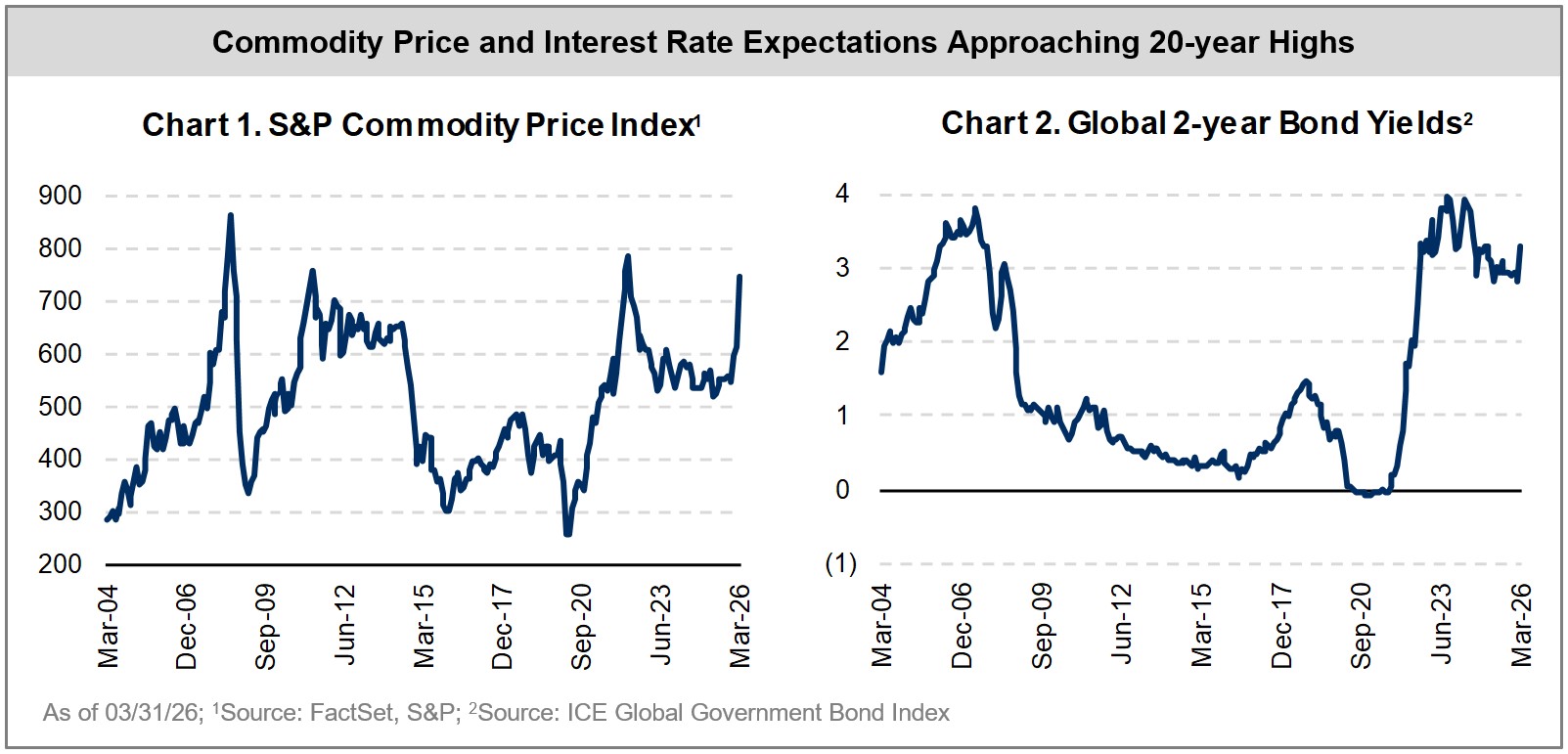

Inflation, interest rates, and risk premiums will largely be determined by the same factors, exacerbated by global capital flows. As shown in Charts 1 and 2, commodity prices and bond yields have, at a minimum, increased, and in some cases more than doubled. Considering the ballooning debt and deficit levels globally, economic strains could be more pronounced if these forces persist.

With history as a guide, we know that stock markets typically bottom long before the fog of war lifts and conflicts end. This does not imply that we should blindly follow the same playbook as past conflicts, given the material changes across economies (innovation/AI/demographics/sovereign conditions), markets (composition, concentrations), companies, and underlying valuations. Rather, it means embracing near-term uncertainty in pursuit of long-term, bottom-up opportunities among oversold investments.

India is a prime example. Our Indian investments and those with direct exposure to India suffered losses during the quarter, weighing on relative performance. India is a major importer of oil from the Middle East, so the war and energy disruption had an immediate impact on Indian stock prices, the value of the rupee, and external balances. India, however, has among the most compelling investment profiles in the world, with a young population, low credit penetration, improving foreign direct investment, and positioning as an attractive alternative to China.

We own HDFC Bank, a leading private bank in India, which is trading near all-time low valuations. Revenues and EPS are expected to grow at double-digit rates due to strong loan demand, operating leverage after years of investment, and continued market share gains from slow-moving state bank rivals. Another of our holdings, Japanese auto company Suzuki, fell to an all-time low valuation, as its largest profit source is India. Suzuki is the leading automotive manufacturer in the country, benefiting from rising car penetration and a continued shift to higher margin vehicles. We increased our investment in these companies over the last several months, as we see significant upside over the long term.

AI Disruption

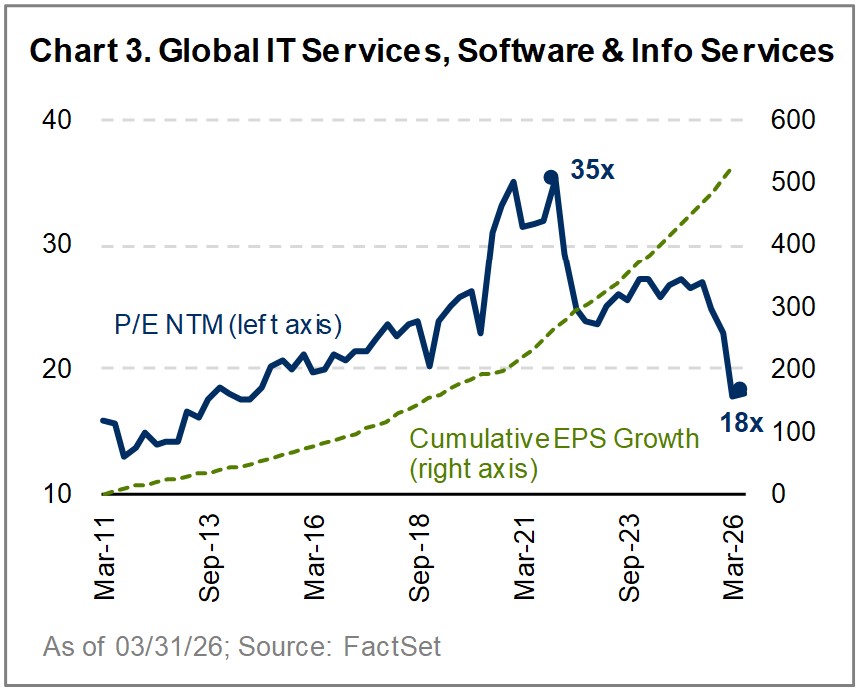

Outside of the Middle East, AI disruption remains a significant source of market controversy. Profound changes are underway across industries, and the stock performance and valuations of companies perceived as AI winners versus AI losers have been widening at an accelerating rate. In many cases, this is justified, but in others, it reflects narratives being detached from underlying fundamentals. Chart 3 illustrates the extent of this valuation compression.

Change on this scale creates opportunity as well as risk. As with most technological innovations in history, we believe the greatest long-term beneficiaries of AI will be the consumers and businesses that embrace it, rather than the early innovators. Considering the pace of AI innovation and our ownership mindset, distinguishing AI beneficiaries from AI casualties requires thoughtful analysis and deep engagement within relevant industry ecosystems. Important considerations include whether companies have dynamic management teams that are proactively integrating AI into operations and strategy, the extent to which proprietary or unique data, customer entrenchment, and/or high switching costs are creating durable competitive advantages, and whether the companies have the financial wherewithal to invest and fund AI adoption from a position of strength rather than desperation.

Several of our investments are already benefiting from AI infrastructure build-out. Samsung Electronics, Murata Manufacturing, and SMC Corporation – exposed to memory chips, capacitors, and pneumatic components, respectively – are seeing tangible demand lift from the accelerating pace of AI infrastructure investment. Similarly, Bureau Veritas and Intertek are well-positioned as AI becomes embedded in an expanding range of physical products, structurally increasing demand for the testing, inspection, and certification services they provide.

Elsewhere, outcomes have been more mixed. In many cases, markets have taken a “shoot-first” approach to AI risk, weighing on some of our investments, notably in IT, security, and business services, which have been repriced as though disruption were imminent. In cybersecurity, AI is expanding the attack surface while raising the frequency and sophistication of threats, reinforcing the long-term need for cybersecurity investment. We believe this should favor platform-based providers such as Check Point, whose integrated platform helps customers consolidate and simplify security in an increasingly complex environment. Despite continued growth and industry-leading profitability, Check Point trades at a low-teens forward earnings multiple, implying expectations for material business deterioration.

In IT services, Capgemini and Genpact face comparable situations. We believe enterprise AI adoption will require substantial upgrades to IT infrastructure and business processes, and AI providers will rely on trusted partners, positioning Capgemini and Genpact as critical last-mile delivery partners. This should expand – rather than shrink – their addressable markets. Both companies trade at high-single-digit multiples, priced for imminent disruption with little terminal value despite reaccelerating topline trends.

Along the same lines, Sony has built an enduring and increasingly recurring cash flow profile supported by strong intellectual property across music, gaming, and film. Shares declined due to rising memory input costs and concerns around AI-driven technological disruption. However, in a world of proliferating content, discovery and curation become increasingly valuable; Sony should benefit due to its leading content libraries and platform positions in music and gaming.

Performance Attribution and Investment Activity

In the first quarter, investments in financials (Chubb, Deutsche Boerse, Banorte, KB Financial), information technology (Samsung), and real estate (Daito Trust) were the greatest sources of positive attribution. Primary sources of negative attribution were our holdings in consumer discretionary (Suzuki Motor, Sony, Adidas) and industrials (Acuity, Intertek Group), and our underweight exposure to utilities.

Chubb’s outperformance highlighted its resilient profitability, and management signaled expectations of double-digit EPS growth in the coming years. Consistent execution at Deutsche Boerse and Banorte drove solid earnings growth amidst rising market volatility. KB Financial enjoys a combination of an improving competitive backdrop and much better regulation, helping the shares to rally sharply. Samsung outperformed on tightening memory supply and rising prices, and we continue to see a runway for further upside given improving execution and leverage to the memory upcycle. Daito Trust’s consistent operational performance further drove its defensive cash flow profile in a difficult apartment construction backdrop in Japan.

Suzuki trades at an all‑time low valuation that belies its dominant position in India, where structural growth and an improving product mix underpin a constructive long‑term outlook. Sony faces pressure from elevated input costs and AI disruption risk, but strategic business decisions and efforts to incorporate AI more broadly should counter these headwinds. Adidas is improving profitability under CEO Bjorn Gulden through both better business mix and more disciplined pricing, which should invigorate the company’s unique combination of brand heritage and category strength.

Acuity shares underperformed as volumes for their legacy lighting products remain subdued due to a weak US non-residential construction backdrop. However, the company is continuing to drive strong profit and cash flow growth through improving costs, product vitality, and the expansion of its intelligent spaces division. Intertek shares sold off following a disappointing fourth-quarter release, with both organic revenue growth and free cash flow falling short of our expectations; we view the headwinds as transitory. Subsequent to quarter-end, management reported improving underlying trends, announced a strategic review to evaluate a potential business separation, and received a preliminary takeover approach from a private equity firm – all of which underscore the intrinsic value of the company’s assets.

Much of our investment activity during the quarter involved adding to existing investments that our analysis indicates were oversold, primarily among technology and business services companies, as discussed above. A growing number of new investment ideas are being reviewed, but no new purchases were made during the quarter. We sold one investment, Pernod Ricard, in favor of adding to Diageo. Diageo has a more diversified product and geographic portfolio and is led by a newly appointed CEO, Dave Lewis, a proven value creator previously at Tesco, Unilever, and Haleon.

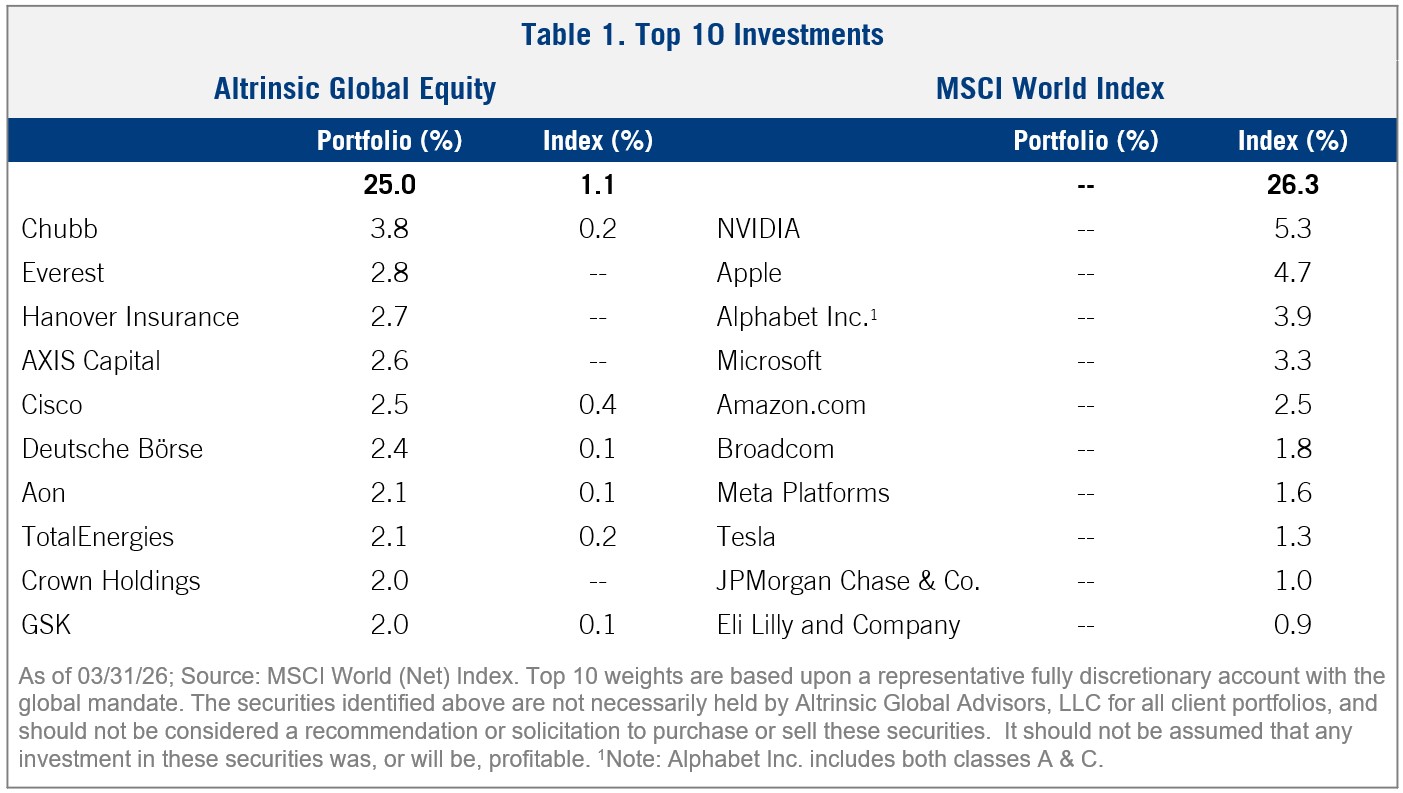

The portfolio is well diversified and meaningfully different from crowded indices, exhibits solid valuation and quality underpinnings, and is positioned to capitalize on volatility that surfaces among the continuing geopolitical, economic, and AI-related uncertainty. A summary of our largest investments is provided in Table 1.

Risk Considerations

At present, the greatest risks emanate from geopolitics and wartime dynamics, any disappointment in the extremely crowded AI narrative, and stagflationary pressures. These risks coexist with high government debt and deficits, which may constrain policymakers’ ability to respond to negative developments. As discussed in our Q3 2025 letter, global markets and economies exhibit an unusually high degree of concentration, circularity, and interconnectedness. These dynamics, together with the growing reliance on a narrow set of AI-driven leaders and the associated wealth effects, represent important risks.

We continue to observe complacency in many areas, as reflected in valuations and the embedded expectations across many segments of both public and private markets. With a flood of IPOs expected and an unprecedented backlog of private companies trying to go public, we see heightened risk of capital misallocation and valuation compression. History suggests that periods of heavy issuance often coincide with optimism near cyclical peaks rather than attractive entry points, increasing the importance of valuation discipline and selectivity.

Closing Thoughts

Well-managed companies with durable competitive strengths can innovate, adapt, and sensibly deploy capital in the face of uncertainty and volatility, typically coming out stronger on the other side. Strangely, many companies with these attributes are among the most attractively valued in equity markets today. We are capitalizing on opportunities arising from AI and geopolitical uncertainty by selectively adding to and initiating investments we believe are mispriced, while remaining disciplined in our assessment of risk and reward. We believe that long‑term investment success often requires being different from the benchmark and from prevailing consensus, particularly when it is hardest and least comfortable to do so.

Please contact us if you would like to discuss these or other matters in greater detail. Thank you for your interest in Altrinsic.

Sincerely,

John Hock

John DeVita

Rich McCormick